By Frank J. Diekmann

There was a phrase I heard over and over while in Washington a week back that I’m pretty sure most who said it hadn’t really thought through, and yet paradoxically, those same people may actually end up nailing it. Let’s hope not.

The words were “Drinking the Kool-Aid.” You’ve certainly heard them, probably used them, and just as likely didn’t give much thought to why the phrase is an ironic part of the lexicon now. Maybe you’ve never known, or have forgotten. In credit union circles, “Drinking the Kool-Aid” is something of an insider wink-wink, a reference to being a part of the cult of credit unions and being all-in on the cooperative business model.

Again and again at America’s Credit Unions GAC and at Mitchell Stankovic’s Underground meeting and at other events in DC, I heard the reference made so often I kept waiting for the Kool-Aid man himself to come bustin’ through the wall. He didn’t, but if CU leaders don’t grab their pitchforks and torches in response to a new NCUA proposal, he just may.

As I’m sure you know, the origins of “Drinking the Kool-Aid” are anything but a funny story about a bunch of hyper kids high on a sugar-infused beverage. If you don’t know the story, you can read more here. Or maybe you just need a one-word reminder: Jonestown.

A Significant Threat

My attention was caught by all the Kool-Aid references after I had already started writing this column about a significant threat to the future of many credit unions that, much like the phrase above, a lot of people in the CU community are naively oblivious to and that, I suspect, some others are quietly lobbying for behind the scenes, and not because it’s good for credit unions—it’s good for them.

As the CU Daily reported here, as part of its “Deregulation Project,” NCUA has proposed rolling back several long-standing procedural and disclosure requirements governing how federally insured credit unions convert into mutual savings banks. If history is any guide, it raises some thorny questions for credit unions, their members and the U.S. CU community overall. And it demands you speak up. Now.

The Deregulation Project has garnered some well-deserved plaudits from credit unions for dust-binning numerous outdated, onerous and repetitive rules and regs at the agency, some of which were originally banged out on typewriters. But regardless of how they were written, the rules related to credit union conversions to mutual savings bank charters were enacted by a prior NCUA board for good reasons and, if anything, they should be enhanced, not dialed back.

Making Merger Deals Look Like Insiders

If you think what’s taken place in some CU mergers, where insiders have lined their pockets with net worth that doesn’t belong to them (I will ask again: how has a lawsuit not yet been filed yet by members of these CUs?), get ready for some inside jobs that make the merger payout deals look like, well, kids at a Kool-Aid stand. (I’m not a conspiracy theorist, but you could easily fill a podcast with the suspicion some CU mergers are about creating a bigger institution that can eventually become a bank with an even bigger IPO.)

If you weren’t around at the time, about two-dozen credit unions took advantage of the then rules to convert to a mutual savings bank or other non-credit union charter between the mid-90s and mid-2007 or so, with activity peaking in the early 2000s. I wrote about many of them then and can tell you that nothing has changed from the pre-iPhone era when it comes to the motivation behind these conversions.

The controversy surrounding charter conversions was even the subject of a paper published by the University of North Carolina School of Law in 2006 that stated, in part, “Concerns and opposition over credit union conversions have recently centered on the potential for diminished voting rights following a conversion, a lack of sufficient member participation in conversion votes (i.e., too small a percentage of the total credit union membership making these critical decisions), and the potential economic windfall in the event of a subsequent conversion to a stock form of ownership.”

That’s academic speak. In plainer language, the members wuz robbed.

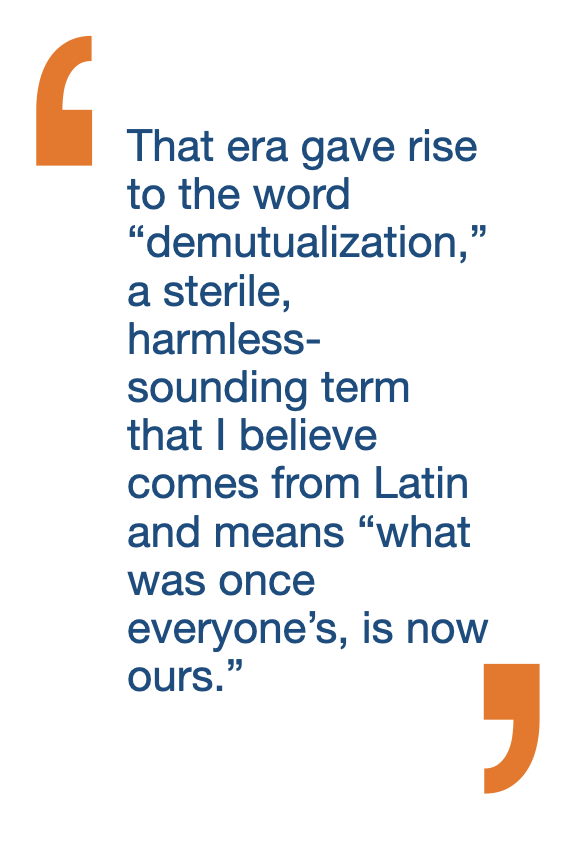

Sounds Harmless, But…

That era gave rise to the word “demutualization,” a sterile, harmless-sounding term that I believe comes from Latin and means “what was once everyone’s, is now ours.” The always-eloquent Ed Speed may call me on that definition, but you get the gist.

NCUA’s new proposed rule would amend subpart A of 12 CFR Part 708a, which outlines the steps credit unions must follow when converting their charter, and includes changes in communication practices, particularly the shift away from print media toward digital channels.

Under the proposal, NCUA said it is seeking to eliminate prescriptive formatting rules that define what constitutes “clear and conspicuous” disclosure. Current rules require specific font sizes and bold text for conversion notices. The agency said those requirements are overly rigid and may limit a credit union’s ability to communicate effectively across different platforms.

The Biggest Worry

The proposal would also revise notice requirements ahead of a board vote on a conversion, and that’s where several sources told the CU Daily their biggest worries lie.

If you want to read all the details of the proposal, go here, but the short version is to clear the runway for charter conversions. If you’re unfamiliar with how this process works, a credit union must Step 1) convert to a mutual savings bank charter in order to Step 2) convert to a commercial bank charter, in order to 3) Step On the former member-owners. With mutual savings banks, the emphasis is on the bank, not the mutual.

If you’re saying Frank, there is still a vote, and it’s all about the will of the members. Is it, though? Slick PR firms get hired to spin these proposals. Disclosures get buried in places where they’re not meant to be found. Apathy gets leveraged. Try to convert a credit union directly to a bank charter, and a lot of those couch-dwelling members are suddenly getting up and are motivated and involved. That’s why the mutual savings bank step is the grease in the middle. “Hey, Member, keep your seat, nothing to see here. You’ll still be an owner, just like in your credit union.” Sure, we’ll stealthily be changing from one member, one vote to one dollar, one vote, but hey, democracy’s democracy, right? Trust us!

What Would be Retained

The proposal would retain some rules, including:

- The requirement that members receive advance notice of a proposed conversion.

- The requirement that members vote on a conversion.

- Rules requiring credit unions to provide mechanisms for members to share views on a proposed conversion, including online posting options.

- Obligations to conduct conversion votes in compliance with applicable federal and state law.

That all sounds on the up and up. But all of that comes only after management has had complete control over what members see, hear and read ahead of casting their ballots.

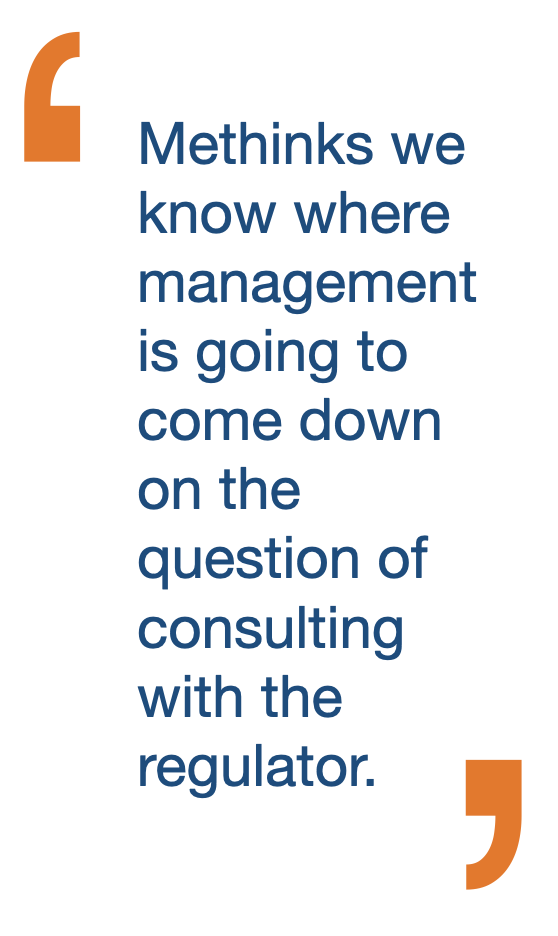

NCUA is also proposing to eliminate requirements that direct credit unions to submit certain member-generated materials to regional directors when disputes arise over whether the materials are appropriate. The agency said management should be able to determine when regulatory consultation is necessary. Would that be the same management (and board) that stands to profit big-time from the eventual conversion to a bank charter? Methinks we know where management is going to come down on the question of consulting with the regulator.

From the School of Spin, 101

I haven’t read one of these conversion press releases in a long while, but I could write one right now. They will all go something like this:

TOMBSTONE, Ariz.–Local Equity Credit Union is thrilled to announce it is seeking to convert to mutual savings bank charter in order to deliver members greater value, more products and services and even better technology options. Importantly, as a mutual bank, members will continue to have an ownership stake.

‘We were founded in the 1900s, and we will always be proud of our history as a credit union,” said President and CEO William T. Kidd. “But times have changed, and the 21st century demands a new charter to provide members with the modern offerings they want and need…”

Blah, blah, blah, yada, yada, yada.

What Won’t be Mentioned

What will be conveniently absent in those releases is what happens when a credit union does convert to a mutual savings bank charter: Hot money from Wall Street firms and investors pours in to take advantage of the “mutual” model of one-dollar, one vote, to approve conversions to commercial bank charters. It happened before, and it will happen again, only this time even more quickly given how easy it has become in the last two decades to move funds.

The bank will go public, insiders on the board and management will ultimately, cash in, as will the hot money investors who will then move onto to the next deal, maybe even another former credit union. And as for all those former CU members? Hey, they voted for it, didn’t they? Democracy!

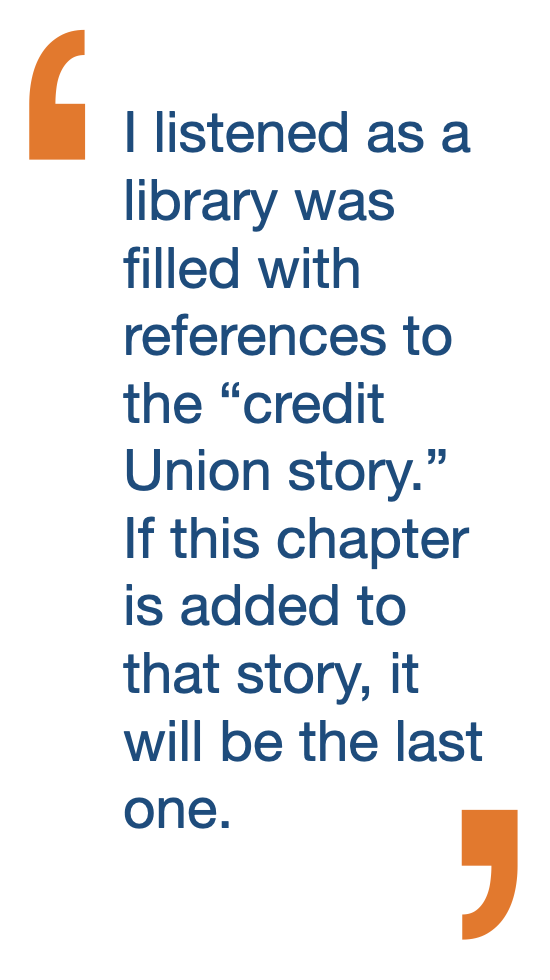

During GAC week, when I wasn’t hearing Kool-Aid references, I heard all about the “credit union family.” Family members don’t treat each other this way; they stick up for each other. I listened as a library was filled with references to the “credit Union story.” If this chapter is added to that story, it will be the last one. And I heard trade association speaker after trade association speaker exult from the main stage the glories of member-ownership, member control, and democratically run credit unions. If you believe it, DEFEND it. Or is that just Capitol Hill cover?

A Challenge for Two Groups in Particular

All credit union leaders have a stake in this charter conversion issue, but I’ll issue a challenge to two groups in particular: Development Educators and Crashers.

The National Credit Union Foundation recently announced a new class of 47 freshly minted DEs, explaining that participants explored “the cooperative principles, credit union purpose, and unique ideas that set credit unions apart from other financial institutions…” It’s a terrific program and I’m proud to have taken part in it (Class of ’99), but it’s time to talk less about “Best Class Ever” and more about why you took the class in the first place—you know, that principles and purpose thing. Or is all of that just talk?

As for the Crashers, your enthusiasm is exciting, but if you’re planning a future in credit unions, there must be credit unions in the future. Crashers have made a lot of noise in recent years, boisterously making themselves known at credit union meetings and events. Here’s your chance to make some more noise. If not, you’re going to be crashing into a new reality, because when a CU-turned bank talks about creating new “efficiencies,” here’s a hint: you and your job are the efficiency.

Will it be Your Last Drink?

NCUA’s proposal references “disclosures” in numerous places. Credit union leaders should demand those disclosures disclose everything and do so conspicuously and repeatedly in plain language, making clear what members stand to lose.

The deadline to comment on the NCUA proposal is April 13. Or you can choose not to comment and practice none of the preaching. But if you don’t you’re not just “Drinking the Kool-Aid,” you’re helping mix up the whole batch. And you know how that ends.

Frank J. Diekmann is Cooperator in Chief with the CU Daily and can be reached at [email protected].

One Response

There is real risk to member ownership if credit unions convert to mutuals. But I don’t think it’s just a regulatory issue or a case of bad actors. Disclosures only go so far if members aren’t paying attention, don’t understand what’s happening, or don’t feel like owners in the first place.

If we acted less like smaller, nicer banks and more like cooperatives, owned and operated by and for our members, then our members may actually see themselves as owner again. When people feel like owners, they show up. They ask questions. They vote.

It seems like we spend a lot of time fighting for member ownership at the policy level, instead of building it in practice. We ask members to defend something they don’t regularly feel. If we want different outcomes in times like this, the foundation has to be built long before the vote.