WASHINGTON — Could a one-time controversy in credit unions make a comeback? As part of its “Deregulation Project,” NCUA has proposed rolling back several long-standing procedural and disclosure requirements governing how federally insured credit unions convert into mutual savings banks, and if history is any guide, it raises some thorny questions for credit unions, their members and the U.S. CU community overall.

NCUA said the changes related to such conversions (see the agency’s other new deregulations proposals here) are meant to reduce regulatory burden and give credit union boards more flexibility in managing the process. But several people, asking for anonymity until additional information is available and they have been able to fully read through the proposal, told the CU Daily they have serious concerns some credit unions will look to convert to mutual savings bank charters–as wqs the case in the past–and then “demutualize” and become stock-issuing commercial banks in order to reap big windfalls for senior management and board members.

As one person said, “If you think the money insiders are taking in some of these mergers is egregious, wait until you see what happens when credit unions convert to banks.”

The agency has stated its proposal would not eliminate the requirement that members vote on a conversion or receive disclosures, but it is also propsing to remove what it described as overly prescriptive requirements that dictate how those disclosures must be formatted and delivered.

A Huge Concern & a Look to History

One huge concern being expressed is over changes NCUA is making to what members would be told about proposals to convert to a mutual savings bank charter, with the agency giving more control to the very board members who could potentially profit.

Conversions by credit unions to mutual savings bank charters and then to for-profit banks were the subject of significant controversy in the early part of this century, eventually catching the attention of Congress, where some members were so concerned there was discussion of legislation that would require greater disclosure to members. Critics of what was taking place argued members didn’t fully realize what such conversions to mutual savings bank charters would ultimately mean if the MSB went on to become a bank, including that they were converting from a democratically based institution where it was was one-dollar, one-vote to one where voting rights were weighted according to the depositor’s balance.

Other critics of the process of the charter conversions argued that members really never had any inkling of what the ultimate goal and motivation of the board and management were, as the only message members received was that they would remain “owners” in the MSB and that the conversion was necessary to “compete in today’s modern, competitive financial services marketplace.”

NCUA Challenges One Conversion

In 2005, NCUA challenged a conversion to a mutual savings bank charter by what was then Community Credit Union in Plano, Texas. The agency alleged the disclosures provided by the credit union failed to meet the requirements of its regulations aimed at preventing the disclosure of inaccurate or misleading information to members considering a conversion proposal.

But the United District Court for the Eastern District of Texas issued a Report and Recommendation in which the magistrate judge agreed with Community Credit Union that NCUA had acted “arbitrarily and capriciously” in failing to certify the member vote, finding that, “once the vote is conducted in a fair and legal manner, the [NCUA] has no authority or discretion to disapprove of the methods or procedures used in the vote.”

In 2006, Community CU converted to become ViewPoint Bank and ultimately merged into LegacyTexas Bank in 2015 after a 2013 acquisition deal.

Paper Examines Conversions

The controversy surrounding charter conversions was the subject of a paper published by the University of North Carolina School of Law in 2006. That paper stated, in part, “Concerns and opposition over credit union conversions have recently centered on the potential for diminished voting rights following a conversion, a lack of sufficient member participation in conversion votes (i.e., too small a percentage of the total credit union membership making these critical decisions), and the potential economic windfall in the event of a subsequent conversion to a stock form of ownership.”

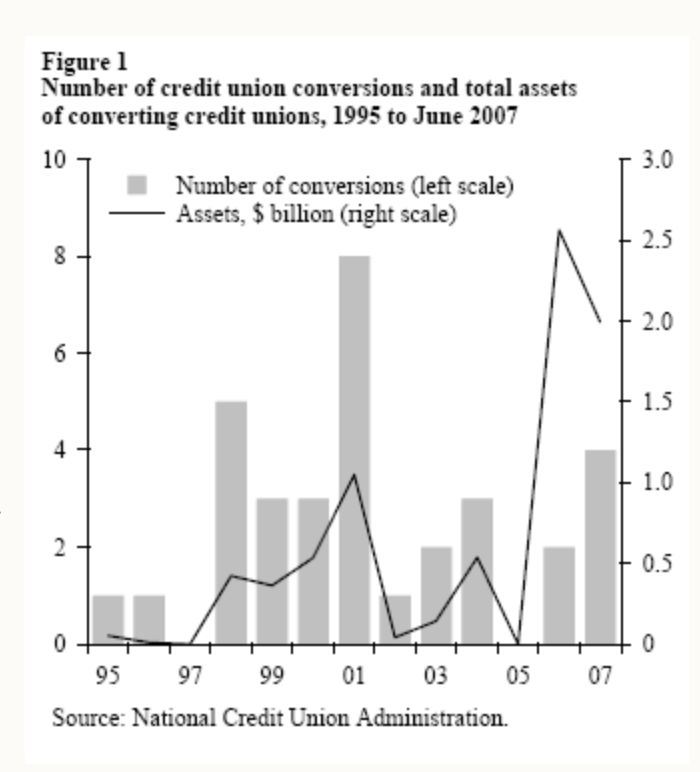

Approximately 21 to 33 credit unions converted to a mutual savings bank or other non-credit union charter between 1995 and mid-2007, with activity peaking in the early 2000s, according to a Federal Reserve Bank of San Francisco report.

What NCUA is Proposing

NCUA’s new proposed rule would amend subpart A of 12 CFR Part 708a, which outlines the steps credit unions must follow when converting their charter, and includes changes in communication practices, particularly the shift away from print media toward digital channels.

Under the proposal, NCUA said it is seeking to eliminate prescriptive formatting rules that define what constitutes “clear and conspicuous” disclosure. Current rules require specific font sizes and bold text for conversion notices. The agency said those requirements are overly rigid and may limit a credit union’s ability to communicate effectively across different platforms.

The proposal would also revise notice requirements ahead of a board vote on a conversion, and that’s where several sources told the CU Daily there biggest worries lie. While credit unions would still be required to post notices in branch lobbies and online, the NCUA is proposing to remove the mandate that notices be published in newspapers, and several detailed disclosure and communication provisions would also be pared back.

Boards Get More Discretion

The agency is proposing to remove typographical requirements for post-vote disclosures and to simplify the definition of “plain language,” leaving boards greater discretion over how information is presented to members.

In addition, the NCUA would eliminate requirements that direct credit unions to submit certain member-generated materials to regional directors when disputes arise over whether the materials are appropriate. The agency said management should be able to determine when regulatory consultation is necessary.

The proposal also calls for removing a section of non-binding “voting guidelines” from the regulation altogether. The NCUA said advisory guidance does not belong in the Code of Federal Regulations and can create confusion about what is mandatory versus optional, even though credit unions would still be required to conduct conversion votes in accordance with applicable law.

The Changes

What Would be Eliminated

The proposal would eliminate:

- A regulatory definition of “clear and conspicuous” that mandates specific formatting, including bold text and minimum font sizes.

- The requirement that proposed conversions be announced in newspapers.

- Detailed typographical rules governing post-vote disclosures to members.

- Requirements directing credit unions to submit disputed member communications to NCUA regional directors within fixed timeframes.

- A non-binding “voting guidelines” section that provides advisory suggestions on voter eligibility, state law considerations and meeting procedures.

What Would be Revised

The proposal would revise:

- Pre-vote notice requirements to focus on posting notices in branch lobbies, on credit union websites and on online banking landing pages, rather than print publications.

- Disclosure rules to rely on a broader “plain language” standard, without detailed examples embedded in regulation.

- Member-to-member communication provisions to give boards more discretion in determining how and when regulatory staff should be consulted.

What Would Remain

The proposal would retain:

- The requirement that members receive advance notice of a proposed conversion.

- The requirement that members vote on a conversion.

- Rules requiring credit unions to provide mechanisms for members to share views on a proposed conversion, including online posting options.

- Obligations to conduct conversion votes in compliance with applicable federal and state law.

Public comments on the proposed rule are due within 60 days of its publication in the Federal Register

America’s Credit Unions: Support for ‘Sensible Updates’

In response to a query from The CU Daily about the NCUA proposal, America’s Credit Unions President and CEO Scott Simpson said in a statement, “America’s Credit Unions supports sensible updates that remove unnecessary regulatory burden and modernize overly prescriptive requirements. This proposal touches on both by eliminating redundant regulatory requirements. Unnecessary regulatory complexity can limit credit unions’ ability to serve members effectively, even when they are operating fully within regulatory guidelines. We appreciate the NCUA’s continued efforts to streamline outdated requirements while maintaining strong and effective supervision. We will continue advocating for a regulatory framework that is clear, balanced, and focused on empowering credit unions to meet the needs of their members.”

One Response

Every small credit union should support the conversion of any large CU to a MSB.