FAIRBANKS, Alaska–Succession planning isn’t just about checking off a regulatory requirement—although that’s important—it’s foundational to a credit union’s talent retention, culture and future, credit unions gathered here were told.

Danielle Scodellaro, registered representative of LPL Financial, told attendees at the Alaska Credit Union Leaguemeeting said that in modern succession planning the most successful credit unions are not thinking about the leaders that have today, they are thinking about the organization they want to have tomorrow and how they are going to fill the seats they need to fill in order to get there.

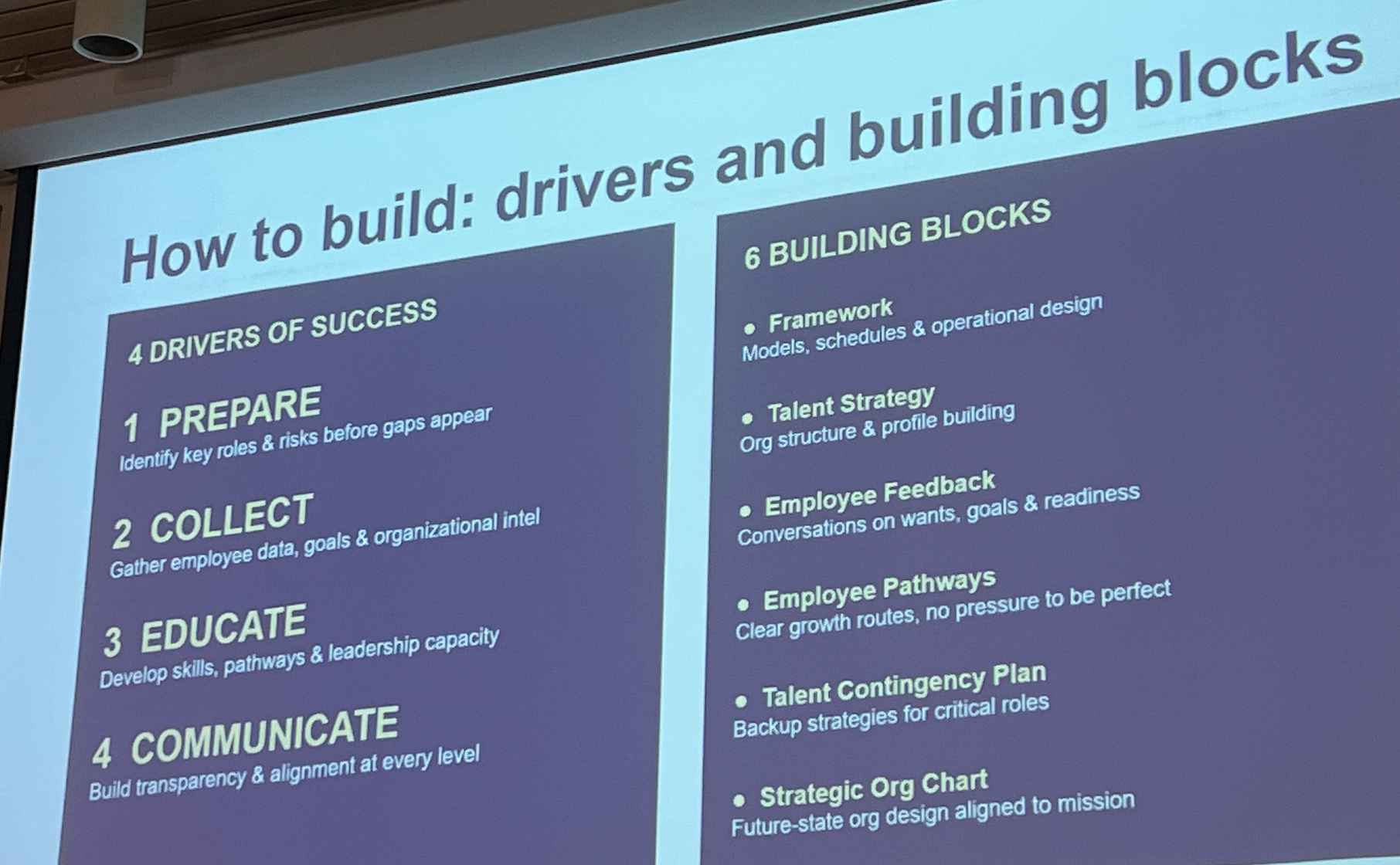

Scodellaro touched on are four drivers of success in succession planning, as well as six building blocks, which are outlined in the slide below.

The Leadership Challenge

“There are not enough leaders today to replace the number of leaders who are going to leave your organization,” Scodellaro said. “This is why NCUA has said you must establish a succession plan.”

She noted the agency requires credit unions to have a written plan that is reviewed at least once every two years, and it should involve more than just the CEO, but senior management and the board.

Building Your Succession Plan

According to Scodellaro, the plans:

- Should be focused on the continuous improvement of the organization

- Should be proactive and ensure no gaps

- Should expand from the C suite

- Need to be adaptive with the credit union

- Need to be forward-looking.

“They have to take into consideration what you want your organization to look like in the future, and how it will compete in the future,” she explained.

She said credit unions must understand their budget for developing such plans before they begin, and also need to have a time frame, need to identify outcomes and require a legal checklist. The credit union must also define who will be involved: Accountants, lawyers, insurance providers, succession planning consultants?

In the four drivers of success, Scodellaro said there is one credit unions frequently get wrong.

“The number-one thing credit unions fail at is step four, the communication piece,” Scodellaro told the meeting. “At the end of the day, people change their lives. They’re making decisions based on the information they have to date, not on information that you’re holding close to your chest. So, you might have some really great candidates, great rising stars, that you want for that next level to bring from the manager to VP or from the VP to the SVP. But if you’re not working with those individuals, communicating with those individuals on how to get there, you are probably still going to lose those individuals and not successfully implement your succession plan.”

The Foundation

In designing the foundation of the succession plan, Scodellaro said the plan must:

- Identify the framework

- Have mission/vision clarity

- Have proactive operational change

- Have flexibility

Models

When it comes to models, Scodellaro said the model must consider:

- Open recruitment. “This is where the NCUA wants all of you to get, which is there is a career path for wherever anyone starts in the organization.”

- Select recruitment

- Outside recruitment

Schedule

When it comes to the schedule for the succession plan, Scodellaro said the two factors to consider are:

- Event-Driven Succession Planning: “I’m sure the majority of executives have a schedule in mind for when they want to retire. The other piece is mergers: mergers are a form of event-driven succession planning. Many are forced to use that form when they don’t have any other options.”

- Unexpected.

Implementing the Plan

“We have to fill the gap, we have to build culture, and we have to develop talent,” Scodellaro said.

Scodellaro explained that filling the gap involves the recruiting, hiring and onboarding of the right people, many of whom may not want to have a long-term career with the organization.

She further noted:

- Building the culture means creating ownership, creating feedback loops and incentives aligned to long-term success

- Developing the talent is about aligning skills to future roles through training, pathways and continuous development.

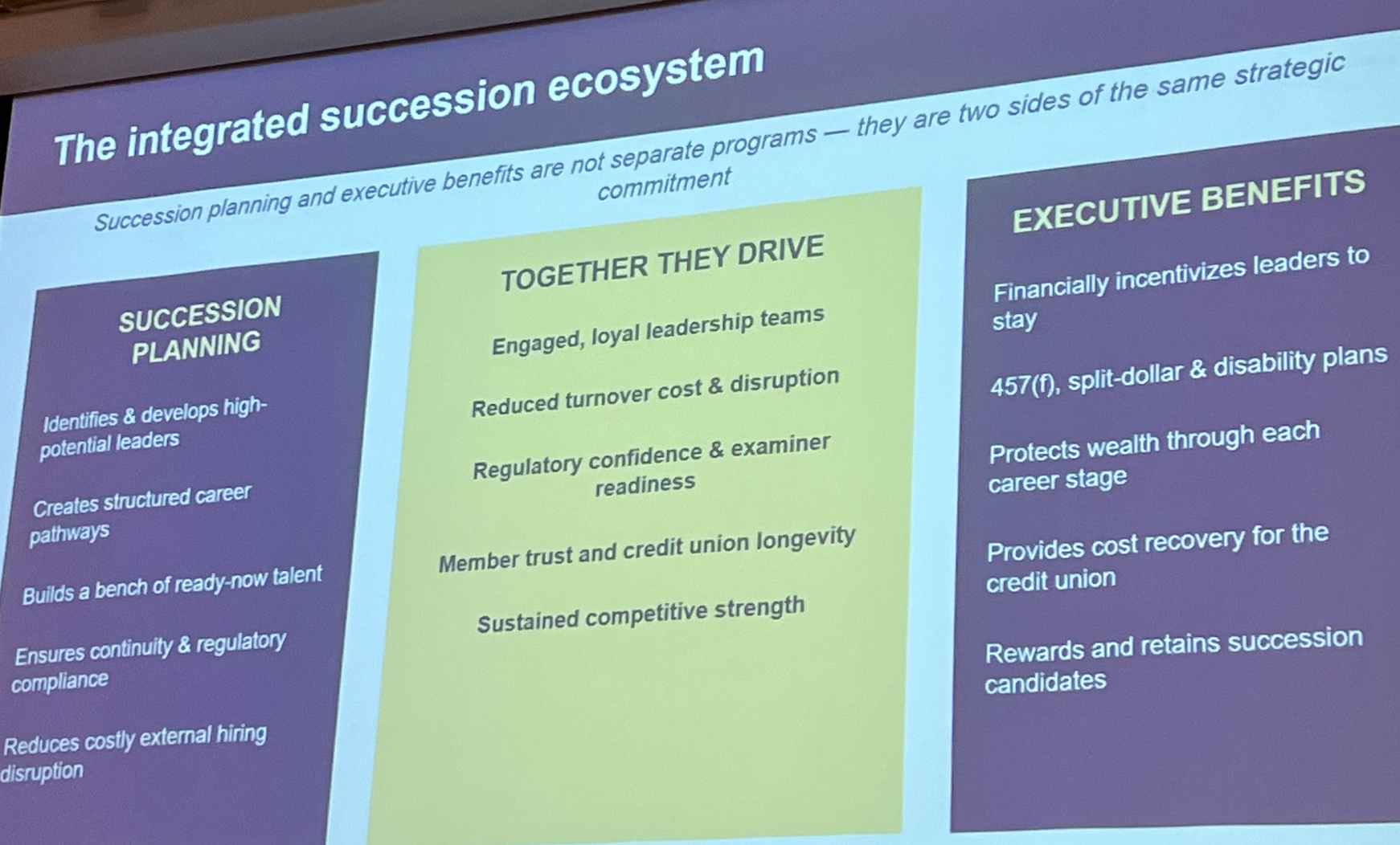

Executive Benefits Plans

Scodellaro described executive benefits are “the retention engine that keeps your best leaders committed.”

If a credit union has a key leader it wants to keep, Scodellaro observed that it’s likely other organizations also want to recruit this person. “And that’s where executive benefits play a role.”

She noted that 82% of people want better benefits, even though as credit unions know well, medical is one of the biggest line items in the budget.

Scodellaro said targeted benefits plans are built around the 5 Rs: Recruit, Reward, Retain, Retire, Risk Management.

“Retirement includes enticing the CEO to move on, even though many organizations are reluctant to address,” said Scodellaro. “Managing risk is around VPs and rising stars. Cash isn’t what they always need.”

Scodellaro said many rising executives may have to choose between helping an aging parent or taking on more responsibility, which is where discussion is really important.