By Jim Drake

One of the most common questions I hear from leaders of large credit unions is this: “What can we do to support smaller credit unions?”

It’s a fair question—and an important one.

But if we’re being honest, the answers often don’t go very far. And from the small credit union side, we haven’t always done a great job of articulating clear, actionable expectations either. We’re good at identifying the issues. Less effective at defining clear solutions.

So, let’s change that.

The Reality

I run a small credit union in a market with multiple billion-dollar institutions. Strong organizations. Well-run. Highly competitive.

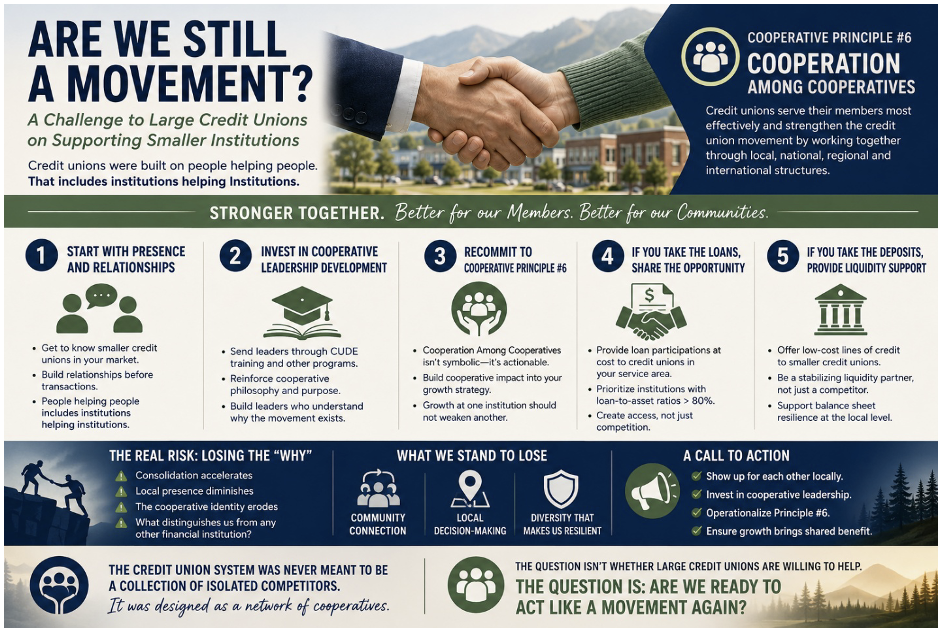

But here’s the reality: Not one of those organizations has walked through our doors to introduce themselves since entering the market or during leadership transitions.

That’s not a complaint—it’s an observation. And it leads to a larger question: Are we still operating as a cooperative movement—or just competing financial institutions that happen to share a charter type?

Moving From Frustration to Action

After sharing these thoughts with peers today, one point was clear: The conversation becomes productive when we move from frustration to specific, implementable ideas.

Here are a few that reflect both my perspective and real feedback from other credit union leaders.

What Real Support Could Look Like

1. Start With Presence and Relationships

Get to know the smaller credit unions in your market.

- Meet with leadership

- Understand their balance sheet pressures and opportunities

- Build the relationship before competition defines it

This is simple—but it’s not happening consistently.

2. Invest in Cooperative Leadership Development

If we want cooperative outcomes, we need cooperative-minded leaders.

- Send executives to CUDE (Credit Union Development Educator) training

- Reinforce cooperative philosophy alongside financial strategy

- Build leaders who understand why we exist—not just how to grow

Because if we only train for scale, we shouldn’t be surprised when we act like scaled competitors.

3. Recommit to Cooperative Principle #6: Cooperation Among Cooperatives

This principle should show up in business decisions—not just conference presentations.

If your growth strategy impacts smaller credit unions, there should be a deliberate cooperative offset.

4. Rethink How We Compete on Loans

This is where today’s feedback added important nuance. Yes—large credit unions have structural advantages in pricing, access, and distribution.

But several peers made a valid point:

- Small credit unions can often compete on rate

- The challenge is less about pricing—and more about scale, channels, and access

So, what are constructive options?

Option A: Expand Loan Participations

- Offer participations to smaller CUs at low or reduced premiums (or at cost where feasible)

- Create consistent access to earning assets

- Help smooth loan-to-asset imbalances

This isn’t theoretical—there are already examples of large credit unions beginning to do this more intentionally.

Option B: Adjust Competitive Practices

A simple but powerful idea raised today: Adopt a policy of not actively refinancing loans away from smaller credit unions in your market

That is one of the most direct ways to operationalize “cooperation among cooperatives”—without requiring subsidy or structural change.

Because let’s be candid—when we aggressively refinance each other’s loans, we’re not functioning as a movement.

5. If You Take the Deposits, Support Liquidity

Deposit competition is real—and smaller institutions feel it faster.

A cooperative response could include:

- Offering low-cost lines of credit

- Acting as a local liquidity partner

- Supporting stability—not just growth

This isn’t charity. It’s about maintaining a healthy ecosystem.

Encouraging Signs

One of the most important takeaways from today’s conversation: This is starting to happen.

There are large credit unions beginning to:

- Share participations more intentionally

- Recognize the imbalance created by scale

- Look for ways to collaborate rather than just compete

That shift matters.

But today, it’s still the exception—not the norm.

When Did Strategy Become Only About Profitability?

At some point, our industry shifted from Mission + Sustainability to Growth + Profitability as the primary outcome

Profitability matters. Scale matters. But if that is the only lens, we lose something fundamental.

Because credit unions were not created to optimize earnings.

They were created to serve people—especially in communities that others overlook.

The Real Risk: Losing the “Why”

If we continue down a purely competitive path:

- Smaller credit unions disappear

- Local communities lose access and voice

- Consolidation accelerates

- The cooperative identity erodes

And eventually, we are forced to ask: What makes us different anymore?

A Call to Action

This is not about blame. It’s about leadership.

If we believe in the credit union movement:

- Show up locally—get to know smaller institutions

- Invest in cooperative leadership (not just operational scale)

- Turn Principle #6 into real business practices

- Compete responsibly—without undermining the system that supports us all

Final Thought

The credit union system was never meant to be a collection of isolated competitors. It was built as a network of cooperatives.

The question isn’t whether large credit unions can help. The question is: Are we willing to operate like a movement again?

I’d genuinely like to hear from other CEOs—large and small:

What does real cooperation look like in your market today?

Jim Drake, CUDE, is president/CEO Blue Mountain Credit Union in College Place, Wash. Mr. Drake can be reached at [email protected].