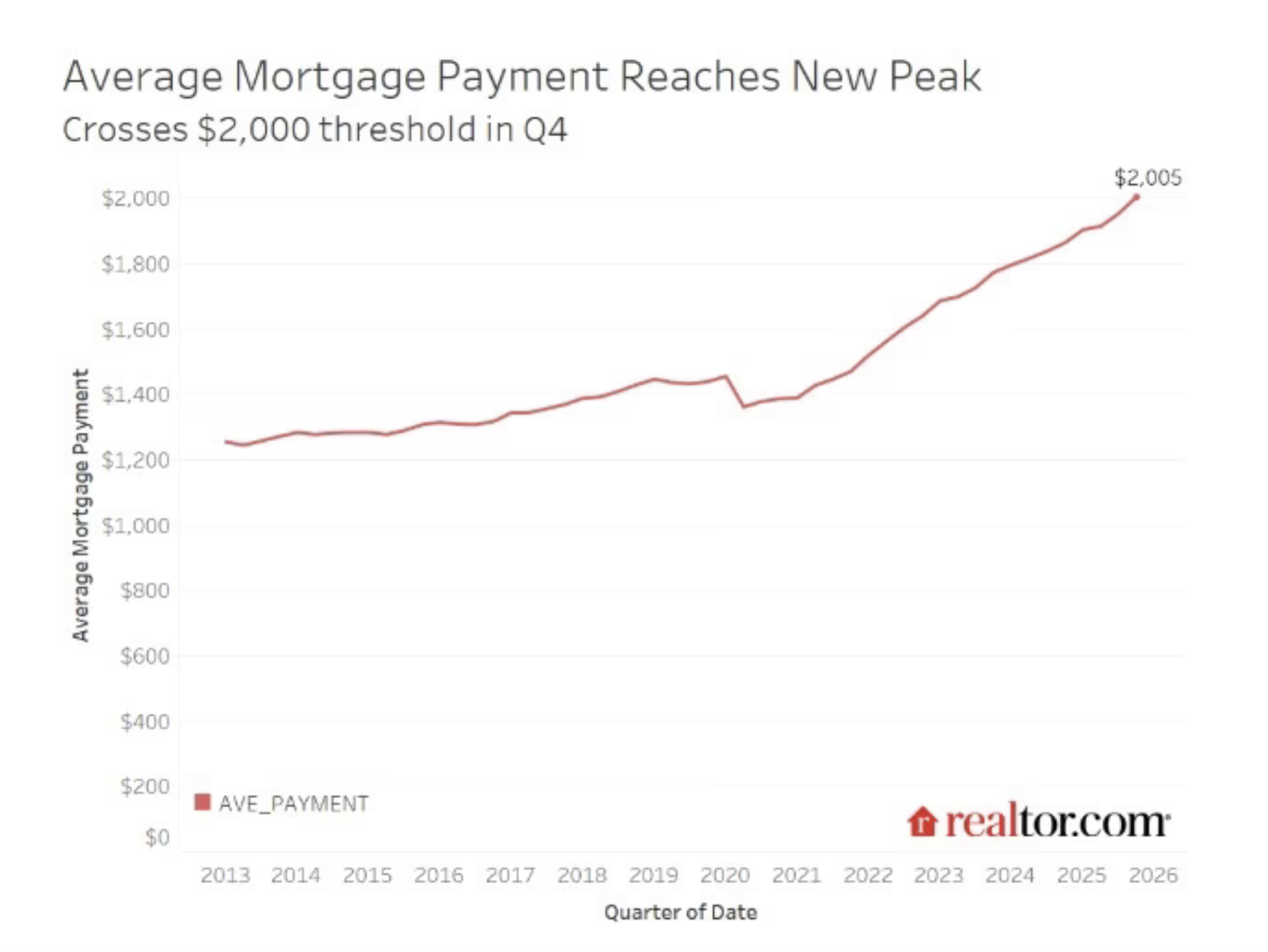

NEW YORK — The average monthly mortgage payment for U.S. homeowners surpassed $2,000 for the first time at the end of 2025, underscoring the continued strain from high home prices and elevated interest rates, according to a report by Realtor.com.

The company’s economic research team said the average payment for existing mortgage holders reached $2,005 in the fourth quarter, a 44% increase from 2021. That amounts to a jump of more than $600 in typical monthly costs over three years, based on Realtor.com’s quarterly outstanding mortgage report.

Hannah Jones, a senior economic research analyst at Realtor.com, said the milestone reflects how higher borrowing costs have filtered through the housing market. She noted that new mortgages had already crossed the $2,000 threshold in September 2022, meaning more recent buyers are bearing the full impact of higher rates and home prices.

‘Much More Difficult’

Realtor.com also cited comments from Sarah DeFlorio, vice president of mortgage banking at William Raveis Mortgage, who said first-time buyers are facing increasing challenges qualifying for homes.

“This means it is much more difficult for first-time homebuyers who are already stretched thin in terms of qualifying for a property that would suit their needs,” DeFlorio said, according to Realtor.com. She added that some buyers are relying on family members for co-borrowing or financial assistance, while others remain stuck renting.

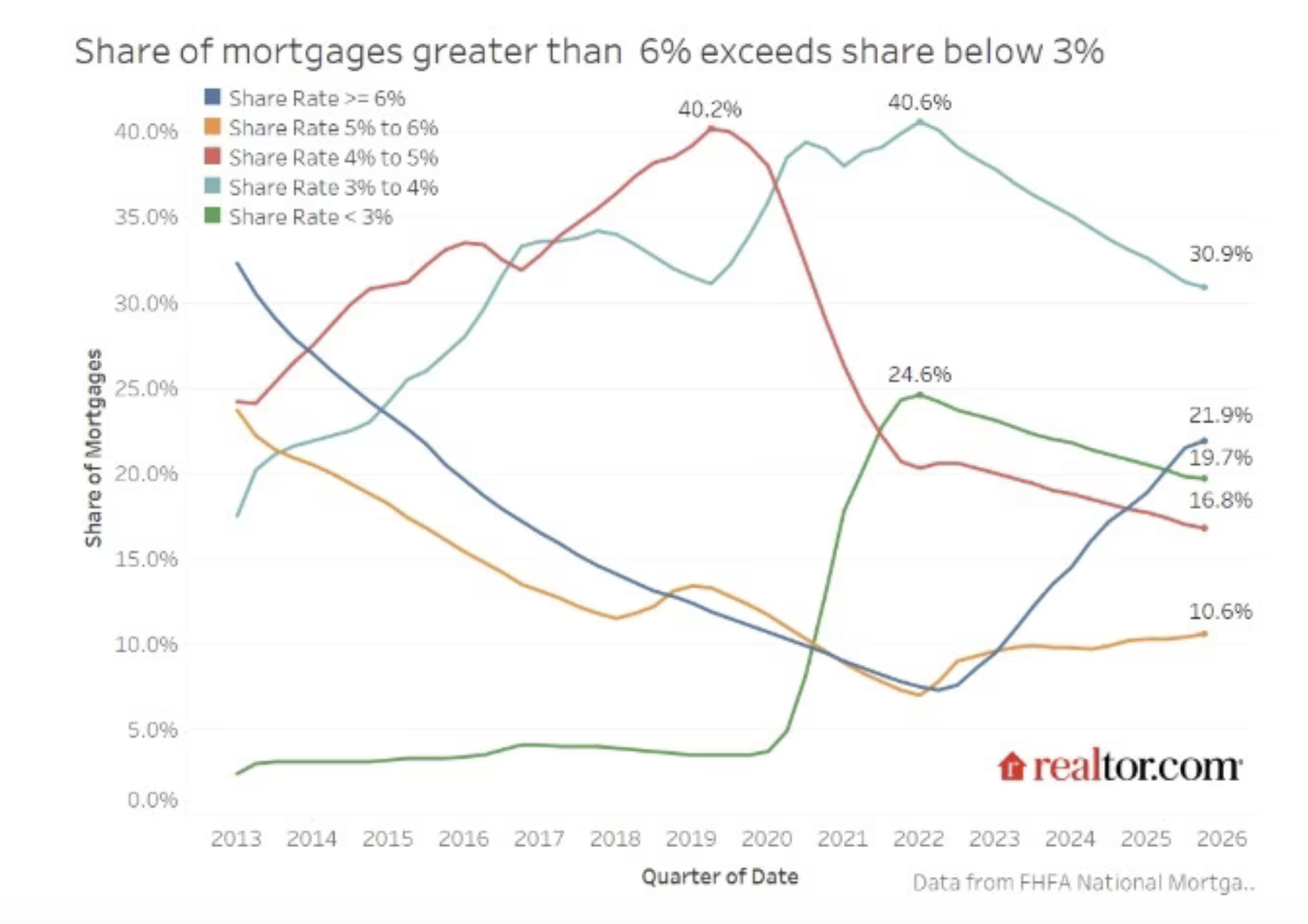

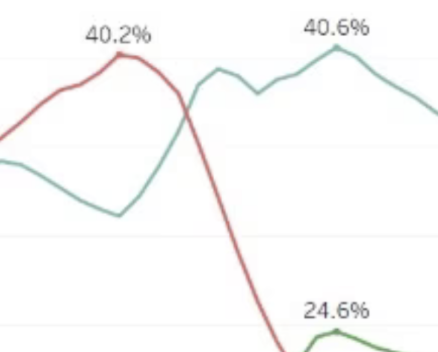

The report also pointed to gradual changes in mortgage-rate distribution that could signal a slow easing of the so-called “lock-in effect,” which has discouraged homeowners from selling to avoid giving up low-rate loans.

Fewer Mortgages Below 3%

According to Realtor.com, the share of mortgages with rates below 3% fell to 19.7% in the fourth quarter from 20% in the prior quarter, while loans in the 3% to 4% range declined to 30.9% from 31.5%. At the same time, higher-rate mortgages continued to rise, with the 5% to 6% category reaching 10.6% and those above 6% climbing to 21.9%.

Jones said the share of borrowers with rates of 6% or higher increased nearly 4 percentage points from a year earlier, indicating that homebuying activity has continued despite affordability pressures.

“Even in today’s high-price, high-rate market, homebuying activity around major life events, such as having kids, a job change, or a divorce, keeps the market in motion,” Jones said, according to Realtor.com.

Slow Shift

The report said the shift away from ultra-low-rate mortgages remains slow, reflecting both homeowners holding onto favorable loans and others paying off mortgages entirely. It also noted that incentives such as rate buydowns offered by homebuilders may be helping sustain activity in the mid-range mortgage categories.

Jones added that easing inflation and lower mortgage rates would be key to boosting seller activity and relieving price pressures in what remains a supply-constrained housing market, according to Realtor.com.