WASHINGTON—Criticism of credit unions by the banking industry has expanded into a new area: low-income designations.

An opinion essay published in the ABA Banking Journal argues that policymakers should review how credit unions’ low-income designation (LID) interacts with proposals to expand federal deposit insurance coverage, contending that changes to business transaction account insurance could disproportionately benefit certain large credit unions and reshape competition across the financial system.

According to the essay, the issue centers on whether proposals to raise deposit insurance coverage for business transaction accounts beyond the current $250,000 threshold should be evaluated alongside existing statutory authorities granted to low-income designated credit unions.

The article was authored by Robert Flock, senior vice president for strategic engagement at the ABA.

Evolved Too ‘Broadly’

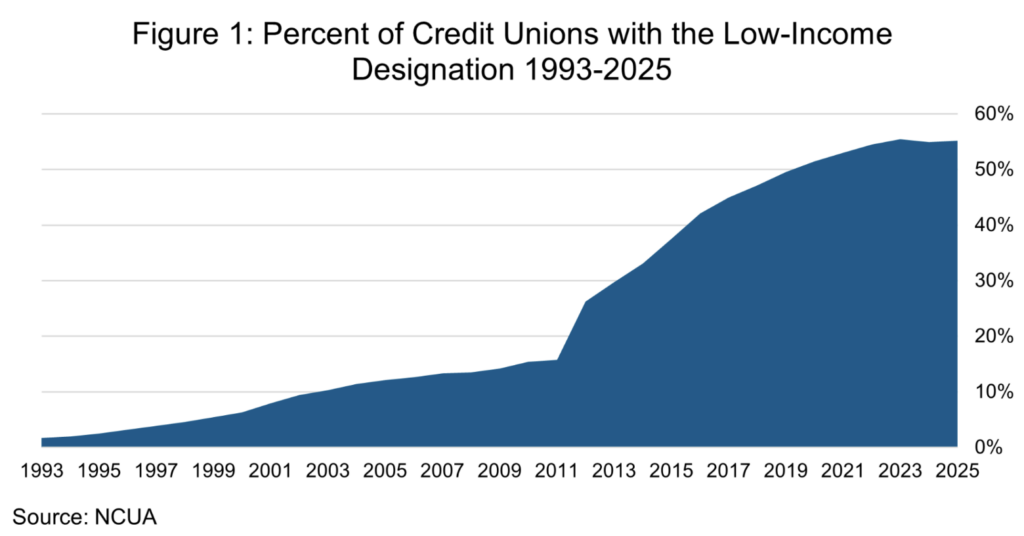

The opinion piece states that the LID was originally established in the mid-1990s as a targeted tool intended to support access to financial services in underserved communities and was initially held by 260 institutions in 1995. By the end of 2025, the ABA Banking Journal reported that 2,390 credit unions—representing approximately 56% of federally insured credit unions—held the designation.

Flock argues that LID status has evolved into a broader strategic tool because it provides exemptions from certain statutory restrictions, including the cap on member business lending and limitations on accepting non-member deposits. According to the essay, many of the nation’s largest credit unions now hold the designation, including 10 of the 20 largest institutions in the sector, with average assets exceeding $16.6 billion.

Points Raised

Among the points raised by Flock:

- LID credit unions can accept deposits from non-member sources, including businesses, municipalities and institutional entities, authorities that generally do not apply to non-LID credit unions.

- Expanded deposit insurance coverage for business operating accounts could encourage concentration of large balances at institutions positioned to accept and deploy those funds.

- LID credit unions’ exemption from the member business lending cap could amplify their ability to grow commercial lending activities relative to other credit unions and banks, according to ABA analysis cited in the article.

The opinion piece further contends that any expansion in business transaction account insurance should be accompanied by a broader review of related policies, including tax treatment, supervisory frameworks and charter authorities.

Call for a Review by Treasury

The ABA Banking Journal essay recommends a Treasury-led review conducted in coordination with banking and credit union regulators to examine how LID status, tax exemptions, deposit authorities and lending authorities interact across the financial system and whether existing policy structures remain aligned with their original objectives.