MADISON, Wis.–New research from TruStage has found three-quarters of middle-market consumers in the U.S., defined as those with a household income between $55,000-$160,000, rate their financial situation as good, and 73% still believe the “American Dream” is within reach.

“Yet beneath this individual confidence lies a more sobering reality; perceptions of economic strength are masking the strain inflation is placing on household spending, future savings and long-term consumer confidence,” TruStage said in releasing the findings from its 2025 Middle-Market Survey.

“While the 2025 data paints a hopeful personal finance picture of many middle-market Americans, there are concerning trends underneath the surface that cannot be ignored,” CEO Terrance Williams said in a statement. “An alarming number of individuals, especially younger consumers, women and Black Americans say financial stress negatively impacts their physical or mental health. This tells us our industry can do more and to reverse these trends.”

Uneven Optimism

TruStage noted the survey found financial confidence among consumers isn’t evenly distributed.

Optimism among women and Gen X is notably lower, with only 64% and 67% believing their financial situation is “good.” “

This is far below the general average of 76%, showing a clear need for more support for these groups as they navigate the complexities of today’s economic environment,” TruStage said.

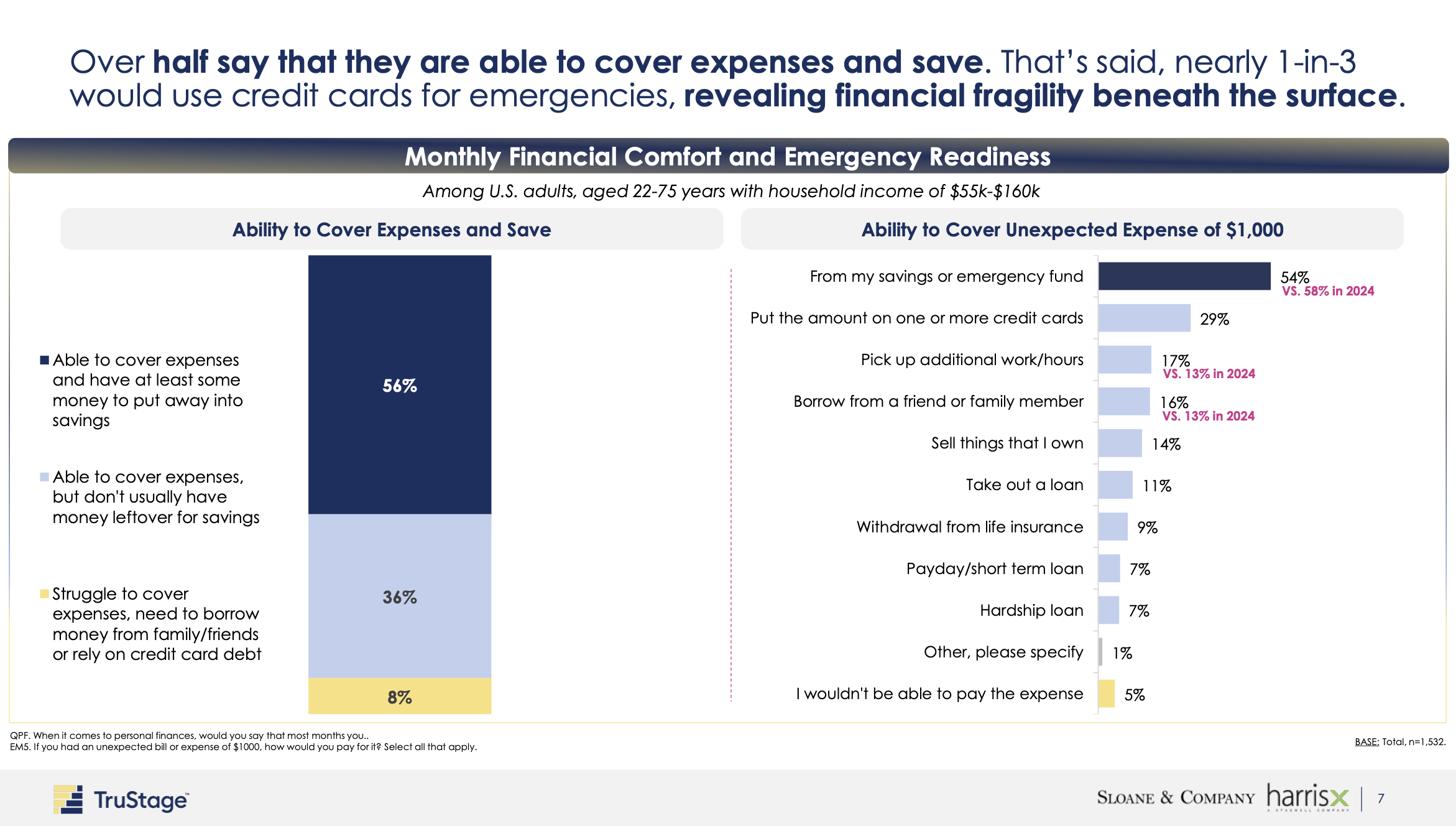

More than half of middle-market consumers (56%) say that financial stress has negatively impacted their mental wellbeing – “further fueled by anxiety around the economy.” The survey found that for 87%, inflation ranks as the top financial concern, and among those feeling the pinch from rising prices, 60% report spending more and saving less, stoking concerns around retirement and emergency funds.

Key Findings

According to TruStage, other key findings include:

Gender Gap

Women express significantly less optimism than men when it comes to their personal finances, highlighting a persistent gender gap in financial confidence, according to TruStage.

- 67% of women report spending more, saving less due to inflation, compared to 53% of men.

- 33% of women say their financial situation is bad, compared to 15% of men.

- 25% of women report their finances are getting worse, compared to 18% of men.

- Only 50% of women see the job market as being good, compared to 67% of men.

- Highlighting further gaps between how men and women perceive their finances, women (58%) are more likely than men (39%) to cut back on social activities due to financial stress, the company reported.

Impact on Wellbeing

“Financial stress is taking a measurable toll on individuals’ overall well-being, impacting both mental and physical health,” TruStage found.

- 56% say financial stress negatively impacts their physical or mental health, with inflation, higher taxes and a possible recession leading as the top concerns.

- The negative impact of financial stress is significantly higher among younger generations with 72% of Gen Z (those between 22 and 28 years old) feeling the effects.

- Similarly, Black consumers are feeling negative impacts on a more pronounced level (66%).

Use of Digital Tools

The TruStage survey found consumers are gradually embracing technology for financial advice, blending innovation with long-standing traditional habits and relationships with financial institutions.

- Search engines (91%), family/friends (93%), and digital news (90%) are the most trusted financial sources

- Despite only 19% of respondents using social media for financial guidance, trust in these platforms has grown, jumping from 67% to 83% since last year.

- Budgeting, saving, and tracking expenses remain core strategies for which the middle-market is using technology, while interest is also growing in other AI-driven tech tools.

The Innovation Imperative

“Despite macroeconomic volatility, this year’s findings report that more consumers have begun saving for retirement (78% in 2025 compared to 73% in 2024),” TruStage reported. “That said, balances are small, with nearly half (48%) reporting having less than $100,000 saved, and less than one in three consumers (29%) express being very confident in making retirement decisions.”

The company added that even with more middle-market consumers contributing to their long-term reserves, “Financial institutions have a responsibility to address the confidence and preparedness gap.”

“Meeting our customers where they are is essential to advancing the TruStage mission of making brighter financial futures accessible to all, which includes empowering people to save for retirement,” Williams added in a statement. “As consumers increasingly embrace technology for financial advice, exactly how we do this will evolve. Ultimately, the future of retirement readiness will be defined by how well we blend innovation with the trusted traditions and human touch people value.”

What It All Comes Down To

According to TruStage, “Bridging this readiness gap increasingly comes down to access, making timely, digestible guidance, where people already manage their money, essential. The use of digital tools is on the rise and can meaningfully extend the reach of human advice, turning intent into action one step at a time.”

Abut the Survey

TruStage said the survey, conducted by HarrisX, sampled 1,532 American adults with a household income between $55,000-$160,000, focused on the middle-market, their perceptions of the U.S. economy and financial habits and future plans. Results were weighted for age, gender, race/ethnicity, region, and income where necessary to align with actual proportions within the population.

For more info: Middle-Market Survey