LOST PINES, Texas—Some credit unions are “completely blind” to what is happening in payments, while others clearly recognize how member expectations have evolved in a market in which consumers will move their business over even short delays in making a payment or, more importantly, being paid, according to a panel of experts.

As one panelist observed, “People want to get their money when they want it, and are much more likely to keep their funds in the credit union if they can.”

Another person shared a story of a company that makes wage and salary payments available to employees immediately on payday, and it shares a list of financial institutions that offer the same-day availability. If a credit union isn’t on the list, the employees choose another provider.

The Panelists

The discussion took place during Catalyst Corporate’s Strategic Summit meeting. Participating as panelists were:

• Glenn Wheeler, VP, payments products and innovation, Catalyst (moderator)

• Don Gonzalez, VP, customer relations, Federal Reserve Financial Services

• Stephanie Prebish, managing director, association services, Nacha

• Keith Gray, VP, strategic partnerships, The Clearing House

• Kris Varma, director, Visa Direct Global Sales and Partnerships

How Panelists Responded

Here is a look at how each of the panelists responded when asked by Wheeler about what is happening in payments, why it is relevant to credit unions, as well as what else they are seeing.

Gray: We run a check imaging network, a wire network and an ACH network, and we launched real-time payments (RTP) nine years ago.

If you think about yourselves and your members or consumers and the way you transact your business, expectations have changed. I think of it like the Amazon effect. I have a son who got his first real job and he asked why it takes two or three days to get paid, yet Amazon can deliver a package the same day.

RTP is a good example. We focus on the real-time nature of both FedNow and RTP. Right now, almost half of the payments that move over RTP do so when your branches and everything are closed—outside of business hours. It’s not just that I expect things to happen faster; I expect to have access anytime.

Other speakers were talking about meeting your customers and members where they are. Where they are is they want to do business, and it’s not just about speed; they want it to be embedded. They don’t even want to have to deal with the payment—like Uber.

We launched RTP, and when FedNow launched, it was to put in place the infrastructure to allow companies like Catalyst to provide products and services that ride on top of that infrastructure to make that possible.

Prebish: We’re seeing tremendous growth in the network. Just in the third quarter alone we had $470 billion in transactions, so we love that ACH has the ubiquity. We’re already there, the infrastructure is there and we have seen use cases now for faster returns with ACH. It’s there for those who need it. It’s great for an emergency use.

We like to say that ACH is just fast enough, and we’re meeting all of those use cases.

Exposed to Experiences

Gonzalez: Your members are getting exposed to this innovation today. They are seeing it, they are feeling it and the question is, is your credit union ready to support them in that innovation?

If you’re not, it’s really a choice you’re going to have to make. Am I going to do what I’m doing as a credit union, or am I going to move forward to make sure I’m meeting the needs of my members as they evolve with these payment capabilities?

The one thing I will leave you with is your members are not going to walk into the credit union or call you up specifically and say, “I want ACH,” or “I want instant payments,” or “I want FedNow or RTP.” They want the experience. They’re getting exposed to these experiences and, ultimately, it’s about meeting them where their finances are being provided to them. You’ll see that as it evolves.

I think it’s an interesting time for credit unions. I was a credit union officer helping to provide all the new services for our members, and I know how important it is for us to provide the best service. That’s why these payment changes and innovations are going to be so critical for credit unions to stay current.

Poor Payment UX Leads to People Moving

Varma: As the network, we see a lot of what’s happening in cards and we get to see this service gateway—whether you have a Mastercard or a debit PIN network like Star, Pulse or NYCE—we get to see those transactions. The interesting thing with community banks that we’re seeing is the amount of cross-border traffic that’s happening. But it’s completely blind, so if somebody goes in and uses their Visa card or jumps out and goes into another fintech, or anywhere else to do a cross-border payment, it’s happening right now.

Clients are jumping out of the UX and going somewhere else. They want that Amazon experience right now and they don’t want to wait.

What we get to see as the network are patterns that are happening, and we get to sit down and talk with banks and credit unions: the data speaks for itself. You might be blind to it because somebody’s funding their account outside through a credit union, but the data doesn’t lie and we know what’s happening. It’s about lifetime value for the customer, and it can be a UX loss. I’m going to do my mortgage and my vehicle loan here, but I’m going to do my banking somewhere else because they don’t offer faster payments.

It’s the difference between walking in and filling out forms for a payment, or saying I’m just going to move my money over there and send it in minutes or seconds. I think that trend is happening as we speak.

We want to make sure members are happy and they feel content and they can do that within the ecosystem. It’s less about the rail they choose; it’s more about getting that faster payment experience right.

It’s an interesting place to sit because we as a network get to see all of the transactions happening, and we see more and more card transactions happening. Now we’re even seeing cross-border card transactions happening, which was never the trend.

The Clear ROI

(Varma said Visa research shows the average consumer who makes cross-border payments has twice as much money in their account as the average customer/member; their tenure with the FI is three times as long as the average customer, and they are four times more likely to buy another product.

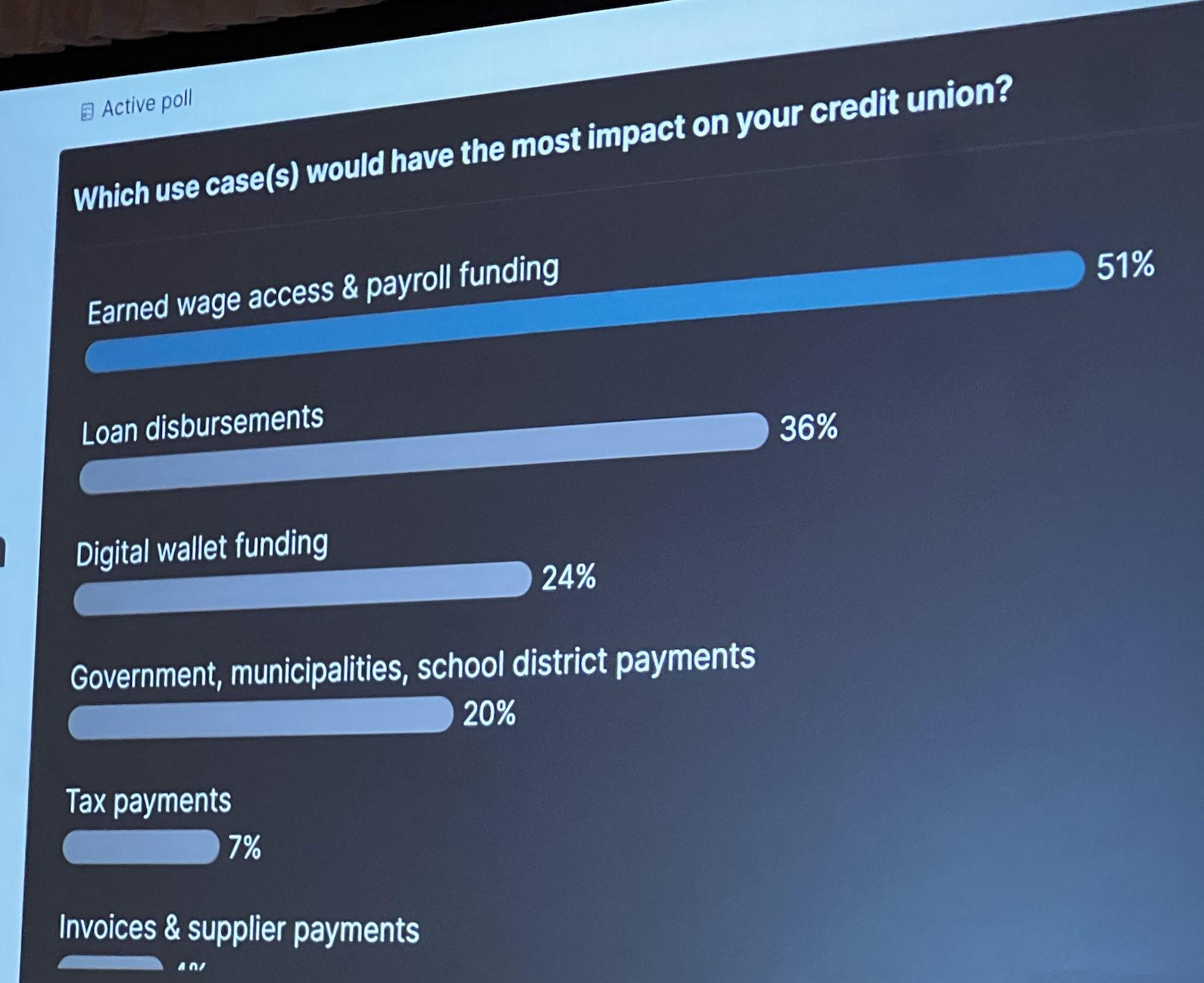

During meeting, attendees were asked to cast votes, as shown below, for payments issued that would most affected them;

One Response

Thanks for your coverage on our Strategic Summit! Hope to see you next year!