MADISON, Wis.—A new analysis is forecasting that the supply and demand for credit will decrease and increase this year, there are “headwinds” for deposit growth, and the pace at which CUs add new members has also slowed, due to fewer loans being made, and more.

Those findings and others are included in the newest Trends Report released by TruStage. The report, authored by the company’s chief economist, Steve Rick, is based on data through December 2024.

Here’s a look at how credit unions performed by category through December, according to the new Trends Report:

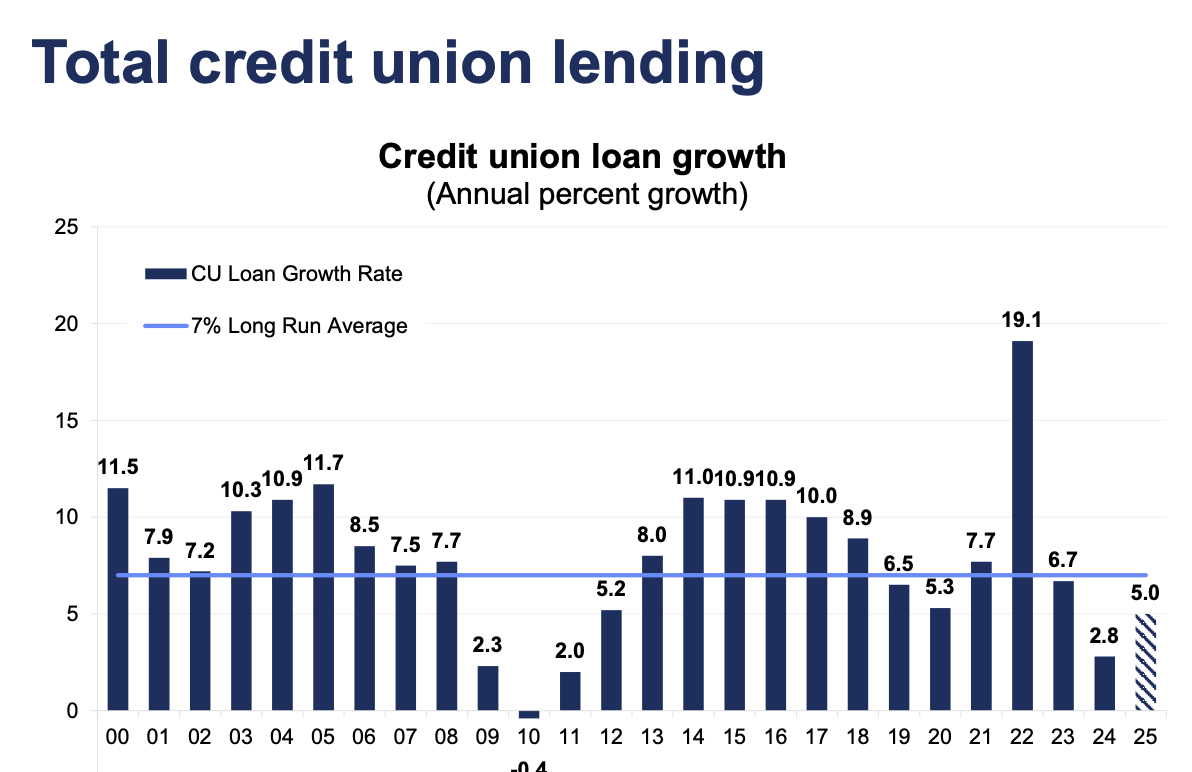

Total Credit Union Lending

Credit union loan balances rose 0.60% in December, more than twice the 0.25% pace reported in December 2023, according to the report.

Driving overall loan growth was strong growth in adjustable-rate mortgages (2.9%), credit card loans (2.7%), and second mortgages (2.4%). December credit card seasonal factors – such as holiday shopping –typically add 3.1 percentage points to the underlying credit card trend loan growth, the report states, further noting that credit union loan balances rose 2.8% in 2024, down from the 6.5% reported in 2023 and below the 7% long run average for two reasons.

“First, the Federal Reserve kept short-term interest rates high form most of 2024, which increased consumer and mortgage loan interest rates, and therefore reduced members’ demand for loans,” Rick wrote in the analysis. “Second tight liquidity, especially among larger credit unions, has reduced their ability to keep making loans. Credit unions now hold 14.2% of the consumer loan market, down from 15.0% which was the highest percentage on record. Expect credit union loan growth to rise to 5% in 2024 as deposit growth increases and liquidity improves. Credit unions with ample lending capacity will see faster loan growth as other lenders face liquidity challenges and even greater concerns around capital and loan performance.”

Consumer Installment Credit

According to the Trends Report, the great deleveraging of the U.S. consumer balance sheet that began in 2008, then reversed course in 2022, has resumed in 2023 as household debt grew slower than disposable personal income.

“Household debt burdens, as measured by residential mortgages and consumer credit as a percentage of disposable personal income, fell to 94% in the third quarter of 2024, down from 95.9% in the third quarter of 2023, according to the Federal Reserve’s Flow of Funds report,” the Trends Report states. “A strong labor market, fast rising wages and slower consumer lending were the primary factors bringing down the debt-to-income ratio.”

The Trends Report analysis found debt-to-income ratios are back to the levels seen in the third quarter of 1999, before the housing and debt boom of 2002-2007. “Falling debt burdens during the last 16 years have improved household balance sheets,” the report states. “Household net worth has also surged since 2009 due to rapidly rising stock and home prices. Expect household debt-to-income ratios to fall slowly for the next few years as income growth barely exceeds debt growth. We expect the supply and demand for credit to decrease and increase this year as lending institutions tighten their lending standards thereby reducing the supply of credit and lower market interest rates increase the demand for credit. Tighter lending standards will reduce credit card and other forms of short-term debt the most.”

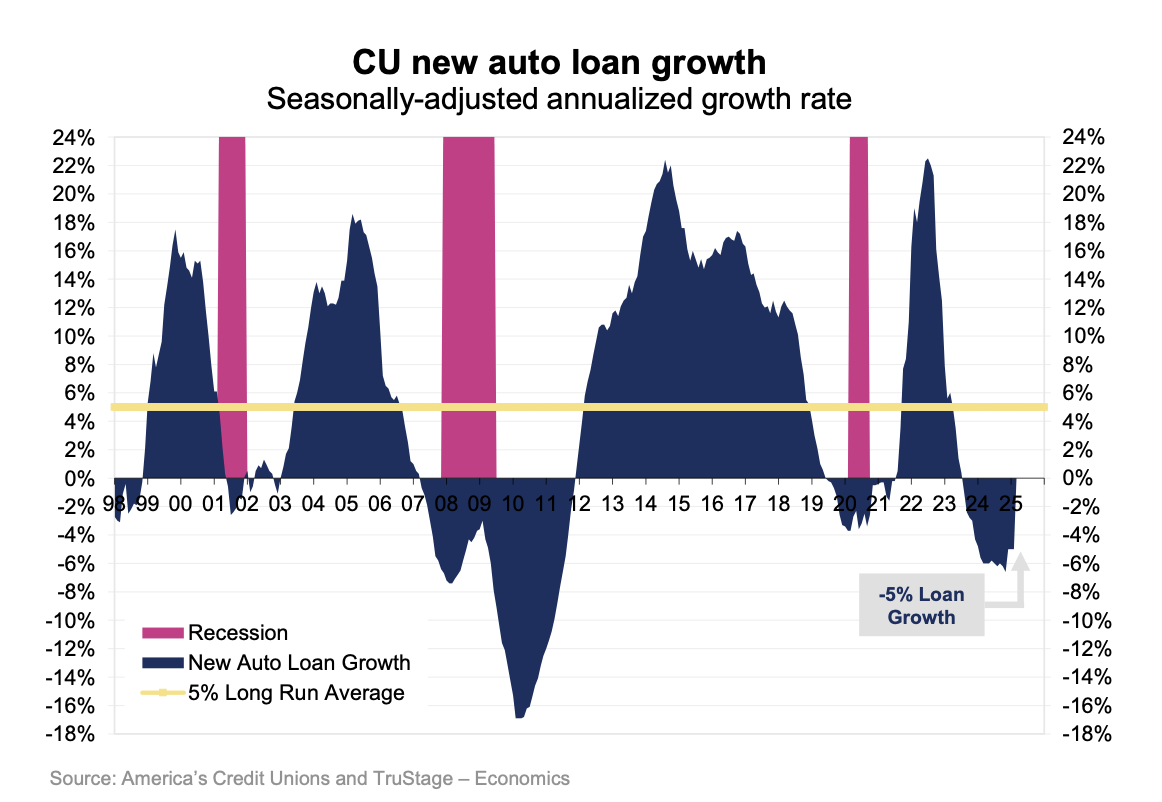

Vehicle Loans

Credit union new auto loan balances fell 0.1% in December, like the 0.2% drop set in December 2023, and rose 5.8% for the full year, which is the slowest pace since 2012, the Trends Report states.

“On a seasonally-adjusted annualized basis, new auto loan balances fell 5% in December due to high lending interest rates, tight liquidity pressures causing some credit unions to pull back from lending, increased vehicle incentives by manufactures, and tighter lending standards reducing the availability of credit,” Rick wrote in his analysis.

The report further notes:

- New vehicle sales rose 0.6% in December from November to a 16.5 million seasonally-adjusted annualized sales rate and were up 5.5% from the pace set one year earlier. “Sales improved due to greater vehicle inventories making it easier to buy a new vehicle, a resilient U.S. economy boosting consumer confidence, and a tight labor market creating two million new jobs and a 4.1% increase in average wages.”

- Despite the improved new auto market in 2024, sales are still below the assumed market equilibrium of 17 million car sales due primarily to persistently high new car transaction prices. “Moreover, declining used-vehicle values are leaving consumers with less equity from their trade-ins making the purchase of a new vehicle out of reach for many consumers.”

Sales to Rise

“For 2025, we expect auto sales to rise from 15.8 million in 2024 to 16.3 million. This 3.2% increase is due to improvement in new-vehicle affordability, steady growth in inventory levels, a relatively healthy labor market and the prospect of declining interest rates reducing the lending costs of a new vehicles,” the report forecasts.

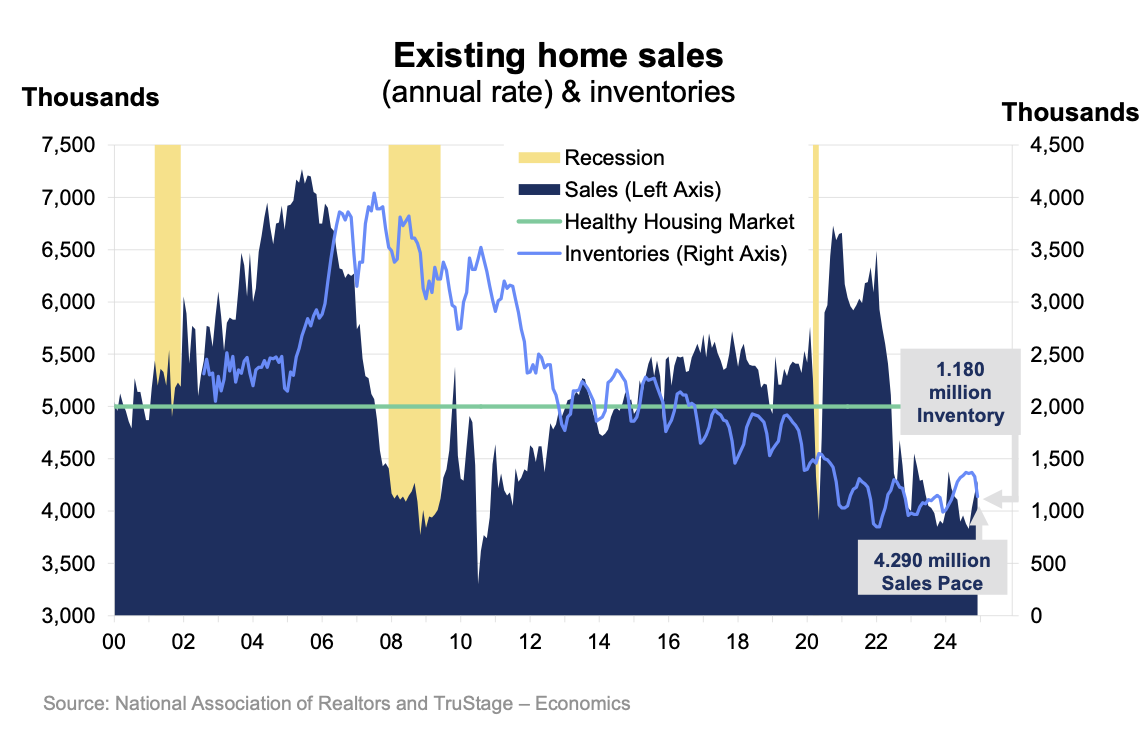

Other Real Estate Information

The Trends Report found the housing market closed 2024 on a stronger note as existing home sales rose 2.9% to a 4.29 million seasonally-adjusted annual rate in December from November, and rose 10.5% from December 2023.

“High mortgage interest rates and high home prices, however, continue to weigh on sales along with limited homes available for sale,” the report states. “Currently the month’s supply of homes on the market has plummeted to 3.5 months, below the six months considered a balanced housing market.

“Meanwhile home prices are still rising due to the tight housing market,” the report continues. “Median single-family home prices felln0.2% in December due to seasonal factors but rose 6% during the last year according to the National Association of Realtors, which is above the 4% long run average. Housing demand is expected to remain below its long-term trend of five million annual home sales during the next year due to unaffordability issues related to high home prices and high interest rates.”

Savings & Assets

The personal savings rate (personal savings divided by disposable personal income) averaged 4.6% in 2024, below the 6% long run average, which has created a “headwind for credit union deposit growth,” according to the new report.

“During December 2024, consumers saved only 3.8% of their disposable income, down from the 4.5% reported in December 2023,” the report observes. “Today’s low savings rate comes on the heels of the high savings rates reported during the COVID-19 pandemic in 2020-2021 when consumers spent less on leisure and hospitality and received three rounds of government stimulus checks. Consumers typically used 80% of their stimulus payments to either pay down debt or to build up their precautionary savings balances. Expect the personal savings rate to rise to 6% later in 2025, due to members’ having exhausted their excess savings built up during the pandemic and rising volatility in the equity markets.”

Rick states that the drop in the personal savings rate is one factor pushing up long-term interest rates recently. The figure shown in the chart, he said, shows how the jump in the savings rate in 2020-2021 helped lower the 10-year Treasury note interest rate.

“Financial institutions used the surge in savings deposits to purchase additional government debt. This increased the price of bonds and reduced the interest rates on those bonds,” the report states. “The recent drop in the savings rate slowed the growth in credit union and bank deposits and therefore the funds available to purchase additional government debt which raises interest rates.”

Equity and Other Key Measures

The credit union movement’s equity-to-asset ratio ended 2024 at 9.7%, up from the 9.1% reported at year-end 2023, as net income grew, and credit unions experienced less losses on the market value of available-for-sale investments, according to the Trends Report.

“Credit union equity (Other Reserves + Undivided Earnings + Unrealized Gains/Losses on Available for Sale Securities) rose $20.8 billion in 2024 due to less losses on securities ($4.5 billion) and higher net income ($16.3 billion),” Rick explained. “The numerator of this ratio (equity) rose 10% in 2024,nwhile the denominator (assets) rose only 3.3%. The net effect was a 6.6% rise in the ratio from 9.1% to 9.7%.”

The analysis goes on to state credit union earnings as measured by return-on-asset ratios came in at 0.70% in 2024, up from 0.68% in 2023, but below the 1% long run average. The gain was due primarily to higher net interest margins offsetting higher provision for loan losses and operating expenses, according to the report.

“Credit unions reported a return-on-equity (a.k.a. equity growth rate) number of 10% in 2024, above the 7.4% 30-year average,” the Trends Report states. “The return on equity ratio is an important measure of credit union financial performance because it is considered the speed limit for asset growth in the long run.

“Credit union equity growth could improve in 2024 if the Federal Reserve continues to lower interest rates later in the year and therefore boosts the market value of available-for-sale investments and reduces the competitive pressure on deposit pricing,” the Trends Report analysis continues. “Therefore, we are forecast return-on-asset ratios rising to 0.75% this year due to rising net interest margins, higher fee income and lower loan loss expense.”

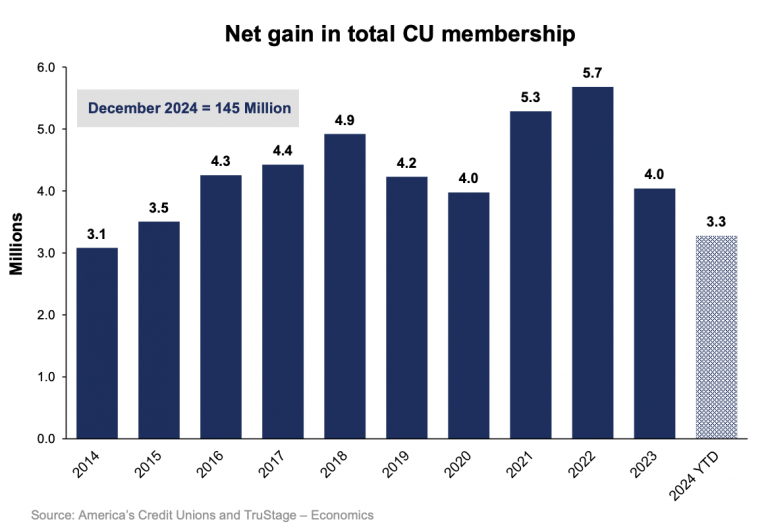

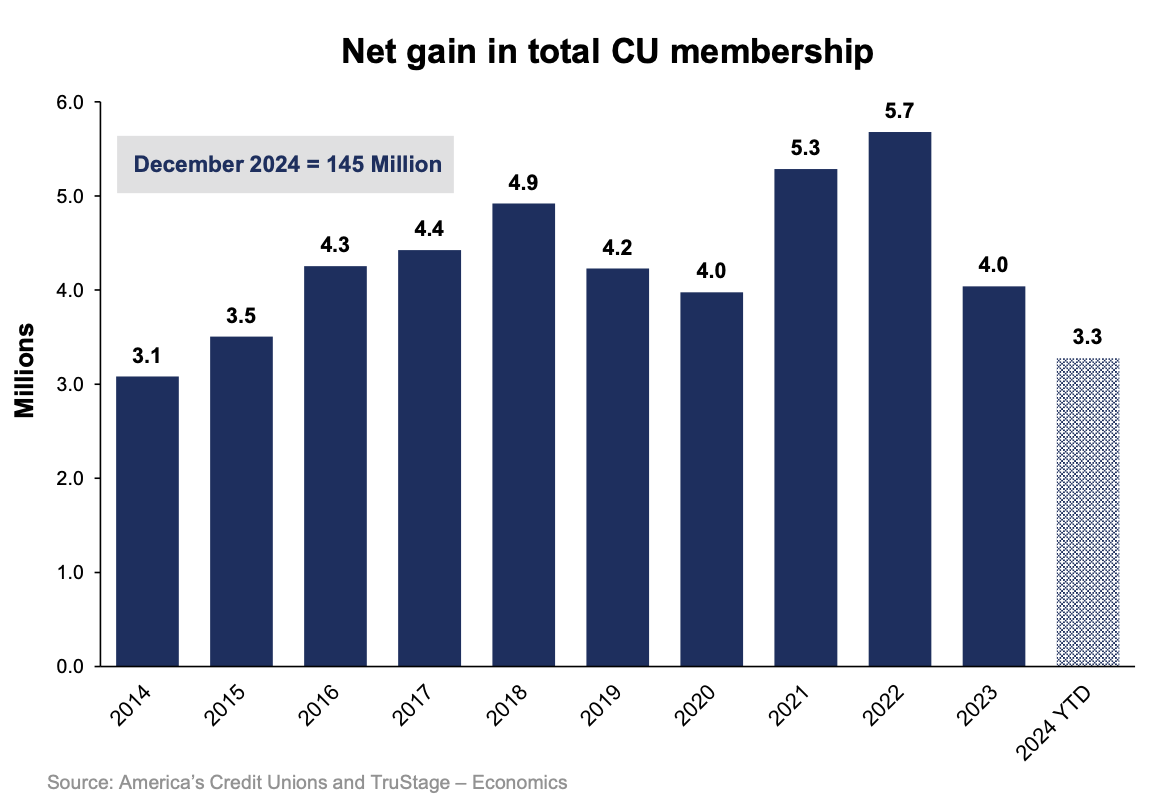

Credit Unions & Members

Credit unions added 303,000 memberships in December, more than the 116,000 reported during December 2023, according to the new data. Credit unions added 3.3 million memberships for all of 2024, the slowest pace since 2014.

“This membership slowdown is due, in large part, to the slowdown in credit union lending,” the report explained. “Membership growth is also driven by job growth. In 2024, the economy gained 2 million jobs, according to the Bureau of Labor Statistics, down from 2.6 million in 2023, and 10% less than the 2.2 million jobs the economy typically added annually during 2010-2019. For 2025, expect a weaker labor market with an expected 1.5 million additional jobs being added to the workplace due to slower immigration.”

Rick noted in the report that credit union membership growth is expected to be 3.0% in 2025 and 2026, below the recent 5-year average of 3.4%, due to a decrease in the demand for credit by the American consumer and slower job growth.