KENNEWICK, Wash.—The leader of an organization representing small credit unions has sent a comment letter to the CFPB in which it “implores” the Bureau to provide relief from HMDA reporting for small CUs, arguing the requirements are unnecessarily burdensome and are having the opposite of their intended effect.

The letter follows a similar letter recently sent to the bureau by America’s Credit Unions.

Doug Wadsworth, president of the $73 million Tri-CU Credit Union and founder of Endangered Small Credit Union Defense (ESCUD), sent the letter calling for the HMDA reporting threshold for loan volume to be returned to the levels that existed prior to 2021. He said only institutions that originate more than 500 closed-end mortgage loans in each of the two preceding calendar years should be required to report.

‘Onerous Reporting’

“The Home Mortgage Disclosure Act (HMDA) reporting threshold requirements have been significantly reduced in the past few years, and is now so low that even tiny credit unions are required to comply with this onerous reporting burden, even if they only finance a couple dozen tiny home equity loans per year (rarely even an actual first mortgage),” Wadsworth wrote. “Not only is the gathering and reporting of this data excessively burdensome and costly to small credit unions, but the tiny amount of data being gathered is likely to be completely insignificant and immaterial to the collecting agencies.

“Burdensome and costly reporting requirements like this are destroying the long-term viability of small credit unions, and limiting the options of homeowners, often those who are overlooked or denied by large institutions,” the letter continued.

Hurting Consumers

Wadsworth said that while ESCUD recognizes collecting housing data is valuable for detecting economic trends and illegal discrimination, the thresholds are now so low that they discourage small credit unions from participating in mortgage lending at all, “which hurts consumers.”

“Prior to 2021, the loan-volume threshold for these ‘mortgages’ was 500, then a couple years later it dropped to 200, then down to 100, and finally in 2023 it dropped to only 25 loans!” the letter states. “If a tiny credit union does 25 tiny home equity loans and a single home loan purchase per year, they are now subject to HMDA reporting! Such small numbers of tiny loans, by tiny institutions… this data cannot provide any significant or material value to the agencies collecting it, while suffocating small credit unions.”

The letter urges the CFPB to recognize HMDA requirements are “the most burdensome and costly reporting burden confronting our entire credit union, likely even higher than the Bank Secrecy Act itself.”

Complicated & Expensive

The letter goes on to outline the code that must be purchased, a complicated login for reporting, another complicated registration process described as “horribly non-intuitive, redundant and slow,” and reporting that requires many hours of data testing and formatting “with their special LAR File tool, which we must download, and then follow a complicated process which I have to ‘re-learn’ every year (since we only use it once per year).”

Wadsworth estimated his credit union, which has a mortgage department of one person, must spend 100 hours per year on HMDA compliance, even if it originates just one mortgage and a couple dozen small HVAC home equity loans annually.

Wadsworth further told the CFPB that smaller institutions are more likely to make loans to borrowers of color who already face greater obstacles to obtaining credit, and that the compliance burden only exacerbates the issue.

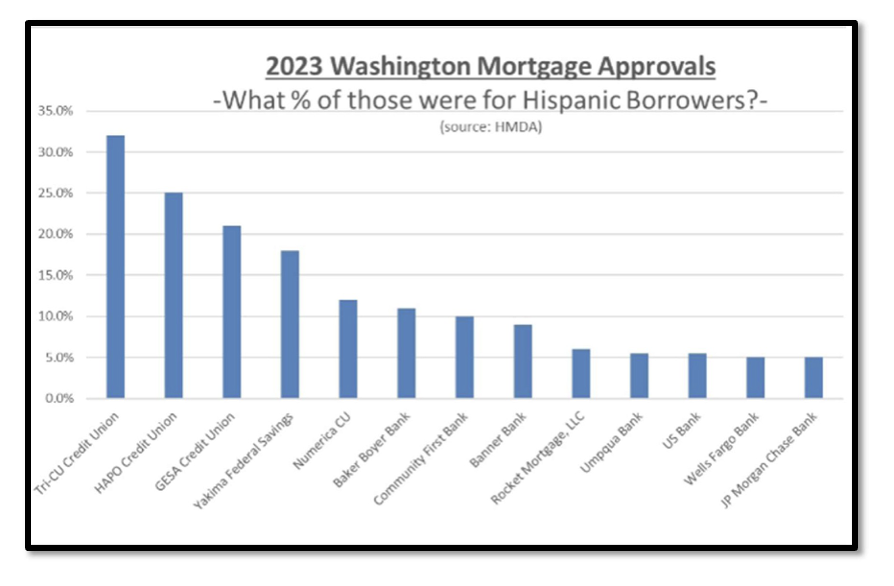

Example Shared

He shared a graphic illustrating that “my tiny credit union (the only small one left in our community) approves a significantly higher ratio of mortgages for minorities than big banks or even big credit unions in my community.”

Wadsworth added, “It might be argued that since our loan-volume threshold is still under 500, we are at least eligible for the ‘partial exemption’ of data reporting, which slightly reduces the number of data points requiring collection. However… the data points still required represent the bulk of the reporting anyway, so we are only ‘exempt’ from 10% of the burden.”

In closing, Wadsworth “implored” the CFPB to increase the loan-volume threshold for small credit unions back to 500 (where it was prior to 2021) and/or increase the asset-size threshold to above $250 million, “so that small credit unions like mine can continue to provide valuable and flexible home loan options to our members, those who need it most.”

Members of ESCUD

The credit unions belonging to ESCUD include:

• Granco Federal Credit Union (Ephrata, Wash.)

• Mint Valley Federal Credit Union (Longview, Wash.)

• Nordstrom Federal Credit Union (Everett, Wash.)

• Tri-CU Federal Credit Union (Kennewick, Wash.)

• Connection Credit Union (Silverdale, Wash.)

• Spokane Media Federal Credit Union (Spokane, Wash.)

• Spokane City Credit Union (Spokane, Wash.)

• Evergreendirect Credit Union (Tumwater, Wash.)

• Prime Source Credit Union (Spokane, Wash.)

• IBEW 76 Federal Credit Union (Tacoma, Wash.)

• Community Healthcare FCU (Everett, Wash.)

• Waterfront Credit Union (Seattle)

• United Trades Federal Credit Union (Tualatin, Ore.)

• POLAM Federal Credit Union (Los Angeles)

• SEG Federal Credit Union (Laurel, Mont.)

• Milestones Federal Credit Union #5144 (Lewiston, Maine)

• Good Neighbors Federal Credit Union (Depew, N.Y.)

• IBEW 26 Federal Credit Union (Lanham, Md.)

One Response

As a clarification: Increasing the threshold (of 25) for HMDA reporting, will likely require an ACT of CONGRESS (ugh), which could take some time (and we need legislators who will fight for our survival). However, these articles (and these pleas to the CFPB) are still useful, because it helps build momentum and shifts public perception in our favor!

Doug Wadsworth

President of ESCUD