WASHINGTON–The executive orders coming out of the White House have complicated an already complicated litigation landscape, according to three attorneys.

Speaking to a session titled “Litigation Trends Impacting Credit Unions” during America’s Credit Unions’ GAC were Brandy Bruyere of Honigman, LLP, and Christina Miller, SW&M, LLP. The session was moderated by Ann Petros of America’s Credit Unions

The session is one of the most popular annually at GAC—either because of or in spite of the threats discussed.

Wire Transfers & EFT

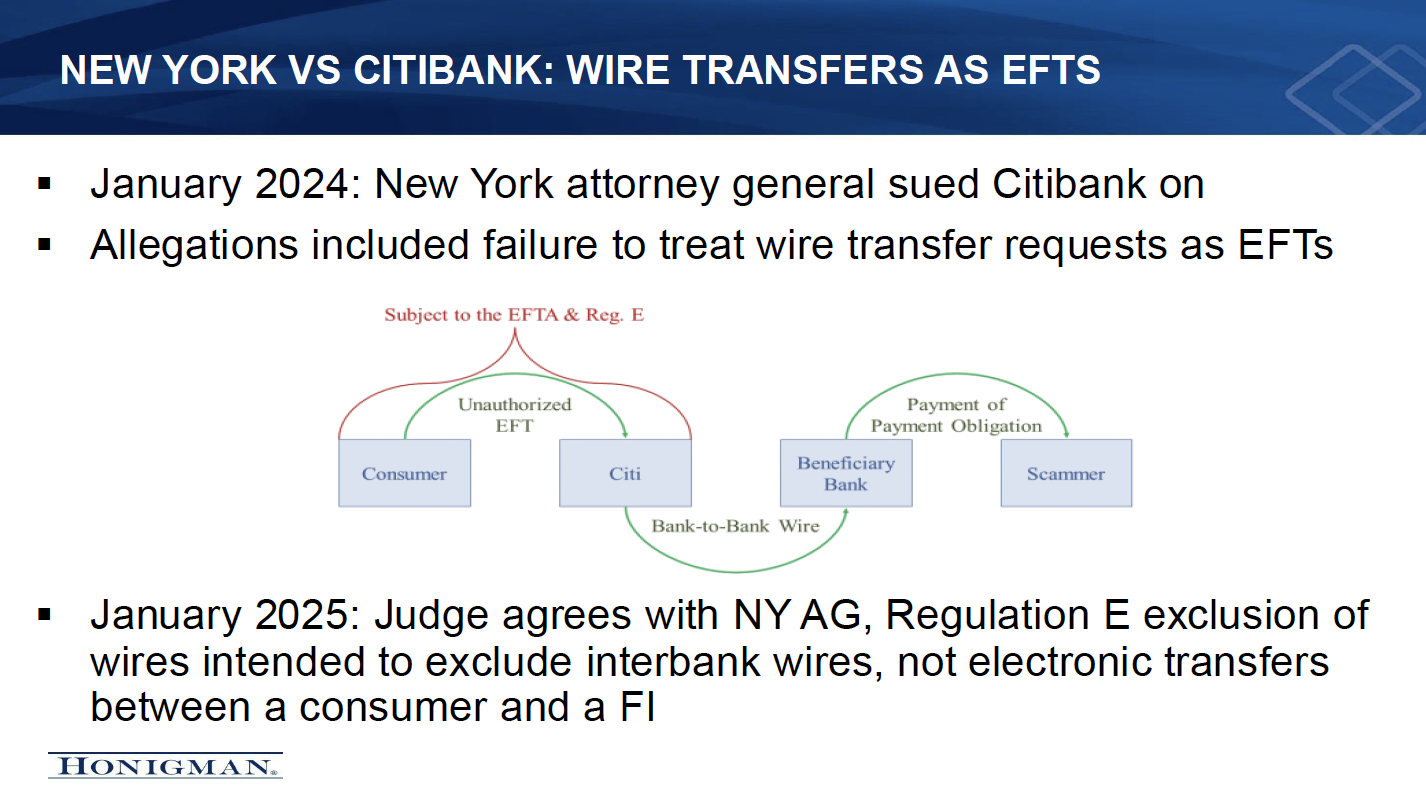

Bruyere began with a case involving Citibank and wire transfers. A lawsuit was filed by the New York Attorney General against Citibank alleging that wire transfers should actually comply with the Electronic Funds Transfer Act (EFT) laws, and that Citi had been out of compliance.

“The argument they’re making here is that when your member logs into their online account and initiates the wire transfer, they’re not really initiating the transfer, they’re initiating from their account over to your general ledger account and then you are sending the letter where you actually facilitate the transaction,” Bruyere explained.

A court has agreed with the New York AG’s position; the case is being appealed.

“It does make sense to go back and figure out what your members need to do to initiate a wire transfer and what do you need to do for security/fraud,” said Bruyere, noting some credit unions have turned to live video authentications.

“Members want to move money as fast as possible without friction, but the easier you make, the easier you make it to commit fraud,” said Bruyere.

America’s Credit Unions and other financial institutions have filed amicus briefs in support of Citi, but the case raises numerous other questions, according to Bruyere, with the briefs arguing the EFTA isn’t meant to cover wire transfers and instead such transfers should fall under UCC.

Junk Fees & Lawsuits

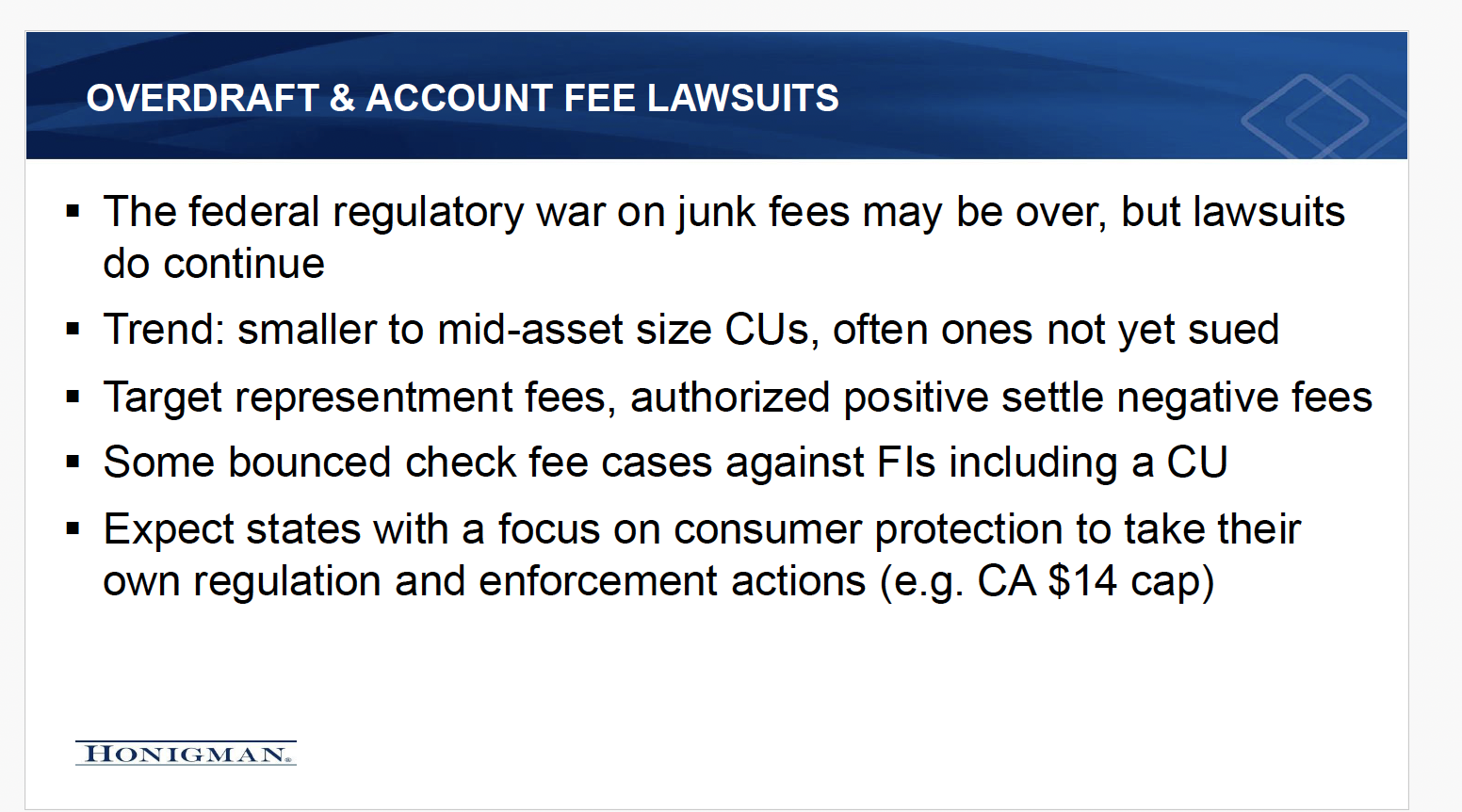

Bruyere said there has been a slowdown in litigation targeting credit unions related to junk fees, and the CFPB has been largely muted under the Trump administration.

“But that’s not going to change the plaintiff’s attorneys from making the same kinds of arguments. They will argue breach of contract, or unfair trade practices, or state level UDAAP,” Bruyere said. “I do still see these lawsuits. The trend was the biggest credit unions all got hit first. Now, there are maybe one or two that are class actions, if you have not updated your membership and account agreements.”

California Remains a Challenge

While NCUA announced during GAC it would no longer publicly disclose the NSF/OD data it collects, Miller said California remains a challenge, including legislation that, effective Jan. 1, 2026, would cap overdraft fees at $14. But not for all FIs.

While the Trump administration has largely shuttered the CFPB, Miller said California has been “aggressive”

“It’s created turmoil in California,” said Miller, explaining that the law only applies to state-chartered credit unions, not state-chartered banks.

“I think (California was) trying to follow the CFPB; they want to have a mini CFPB,” said Miller. “…While we may see pauses with the change on the federal side, what we would say is be very careful…on the state level you.”

DACA Suits at the State Levels

Petros: In class action trends, another trend we’ve seen are suits over DACA status. What do we know about these?

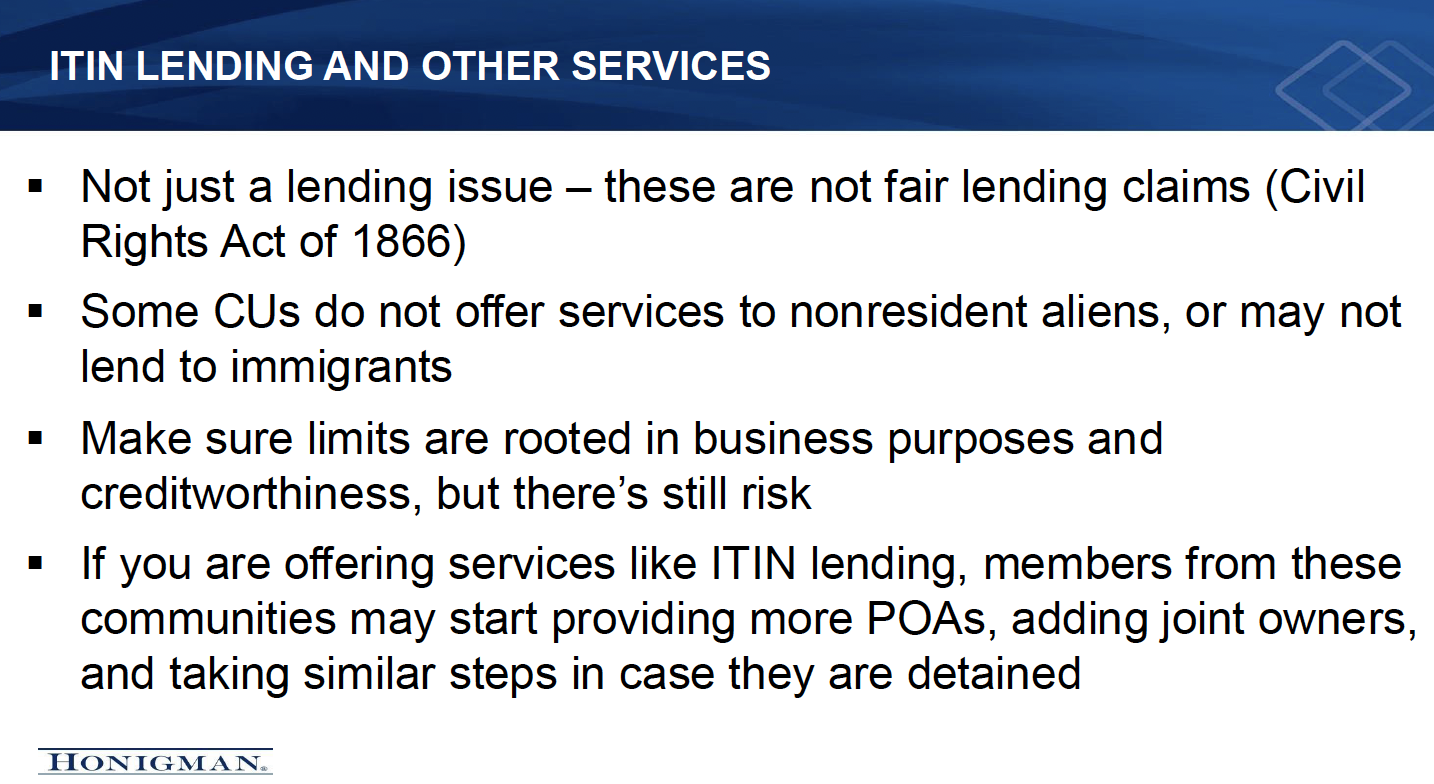

“The Mexican American Legal Defense Education Fund (MALDEF) is an advocacy group that focuses on filing lawsuits to advocate for social change in the communities they represent,” said Miller. “They are targeting us and have now filed 21 lawsuits. The suits are about blanket policies that say we’re not going to lend to immigrants or anyone who’s not a green card holder, and most of these people have DACA status. They are very sympathetic plaintiffs.”

Miller said the suits have resulted in settlements in the $75,000-$100,000 range plus attorneys fees in some states. “Most credit unions have been settling these,” said Miller. “They don’t seem to be going away. They want to see credit unions serving these communities. They are citing a civil rights law enacted after the civil war.”

ITIN Lending

Petros asked about ITIN lending, with Bruyere saying the status of such lending really depends on the credit union involved. Some won’t make the loans, others consider them part of their mission. The risk lies in automatic denials of someone due to immigration status, Bruyere reminded.

Now, with the Trump administration promising to deport many immigrants, some credit unions (and even borrowers) have sought out co-signers in the event the borrower is deported outside the country, she added.

“Whether we are going to be deputized around this is very hypothetical right now,” said Bruyere. “What you are going to see is people being coached by advocacy groups to bring in power of attorney documents. Take some protective measures should they be detained.”

Just from a “practical perspective,” Miller noted that in 2024 there was a suit that came from the contact center level where someone said, ‘Oh, no we can’t loan to you.’ Make sure that top-down, everybody’s trained and everybody else is getting all this information you.”

The Fate of DEI

Petros: Credit unions are nervous over Trump administration orders around DEI and pulling those back and what that means. It’s not just about policies, but also access to special programs focused on underserved communities, the Greenhouse Gas Reeducation Fund, etc.

Miller said many people are overlooking what is included in many executive orders. For instance, one executive order around “unleashing American energy” could affect the $6 billion in funds that are part of the Greenhouse Reduction Fund and reserved for low-income communities to become more energy efficient. OMB had also issued an order to stop disbursing related funds, only to later reverse that.

As Miller pointed out, some credit unions are already receiving funds through Inclusiv, which has more than a billion-dollars to disburse, even though there is a risk the administration may come back and scrutinize such expenditures.

“Make sure you are doing really good recordkeeping about where you are using the money and to whom you are sending it,” said Miller. “Check your financial agreements. You need to look at termination and penalties.”

Attention to CDFIs

Petros: What about CDFIs? They are based on equity and helping certain populations and communities?

The attorneys said they had not seen any action in that area, but they expect CDFI applications will slow even though court orders have stopped some of the executive orders.

Affirmative Action

One interesting point made during the presentation surrounded an interpretation of the affirmative action laws signed in 1965 by President Lyndon Johnson.

“There has been some discussion over whether share insurance makes you a federal contractor,” it was observed.

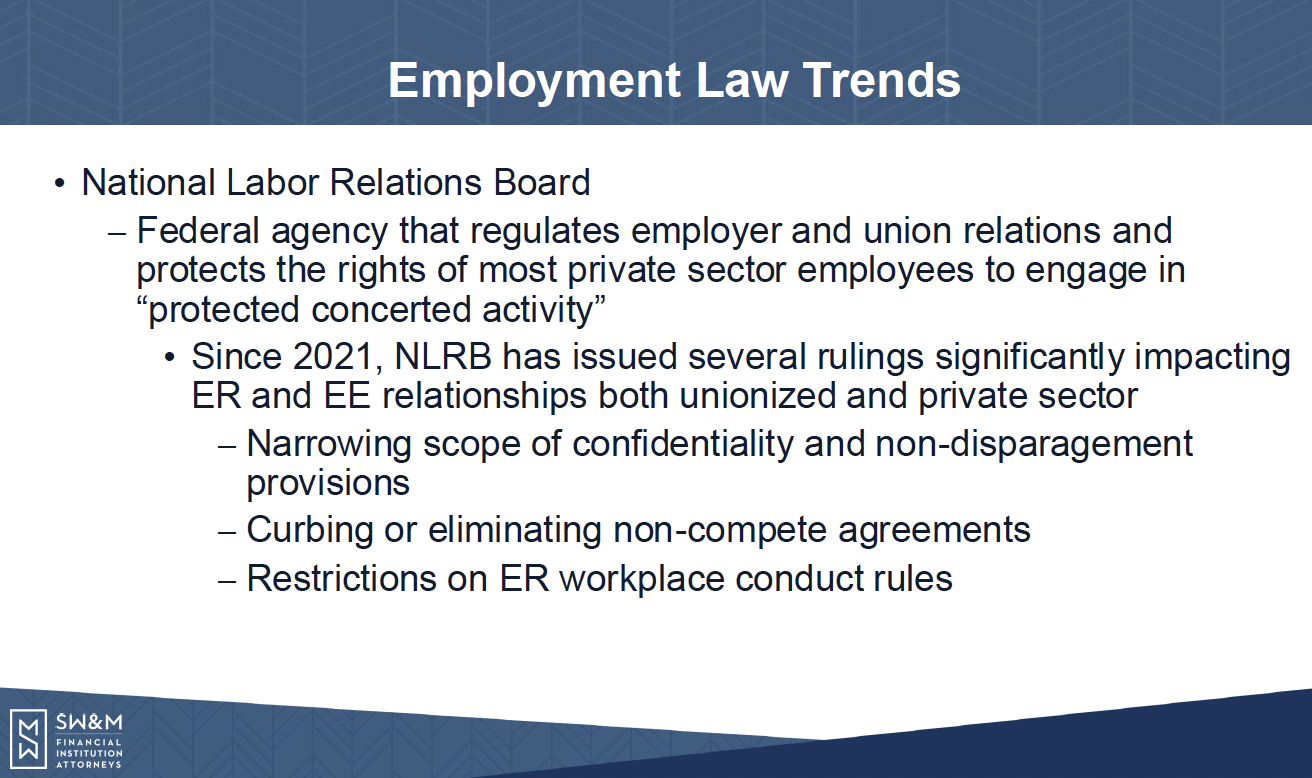

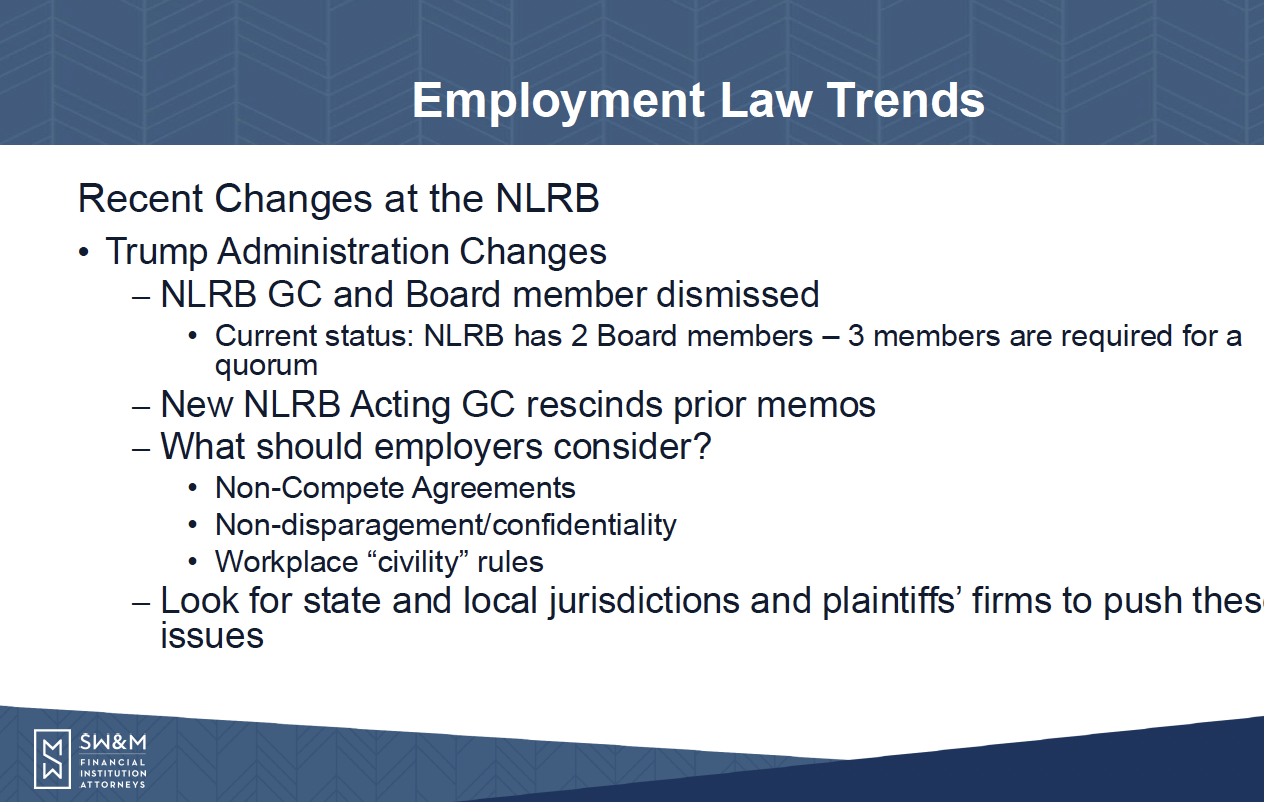

Employment Law

“I will say that employment litigation, I think, is easily even more disruptive because it’s internal and you have employees…so, we always want to keep an eye on the potential for employment litigation,” she said.

The panelists noted the uncertainty surrounding the National Labor Relations Board only compounds the related litigation challenges in a market in which there is a “competition for talent.”

“How do you protect your assets, your training secrets? Will we do that through non-competes? Those are almost prohibited.”

It was noted there remain issues related to non-disparagement and confidentiality provisions

Transparency agreements are also “hot” in employment law, with Miller pointing to several states as being much riskier to do business than others when it comes to employment.

Privacy, Pixels and Google Analytics

As Bruyere explained, a pixel is a mini piece of software that captures data. In 2024, there was some discussion at GAC that such tracking violates wiretapping laws and lawyers may attempt to apply those laws to new technologies such as AI when its used to provide a script to call center agent.

“Are marketing and BD people under a lot of pressure to maximize budgets and get ads in front of people that they are being sold things they don’t really understand? If you ask your marketing people, ‘Do we have pixels on our website sending things to Meta?, they don’t know. To stay ahead of this we want to know what we are using, do we understand it and do we have something to show that we did let our members know.”