By Fred Cadena

Americans are dealing with an affordability crisis. From the rising cost of food and everyday necessities to home prices reaching record highs, consumers are stressed. An April 2025 survey from Pew Research uncovered that 28% of respondents expected their financial situation to be even worse a year later. With April 2026 around the corner, those sentiments are still present.

According to data from a Vericast survey conducted in December 2025, 82% of consumers agree the amount of money in their bank account directly impacts their mental health. On top of that, consumers are more focused on financial stability rather than financial expansion in 2026. As a result, traditional milestones, like buying a house, are taking a back seat to basic financial wellbeing, such as getting out of debt.

Consumers are looking to build confidence and gain financial control this year, creating an opportunity for credit unions to help. First, it’s important to understand sentiments around finances across age demographics, so credit unions can then provide personalized offers that support real consumer needs and goals.

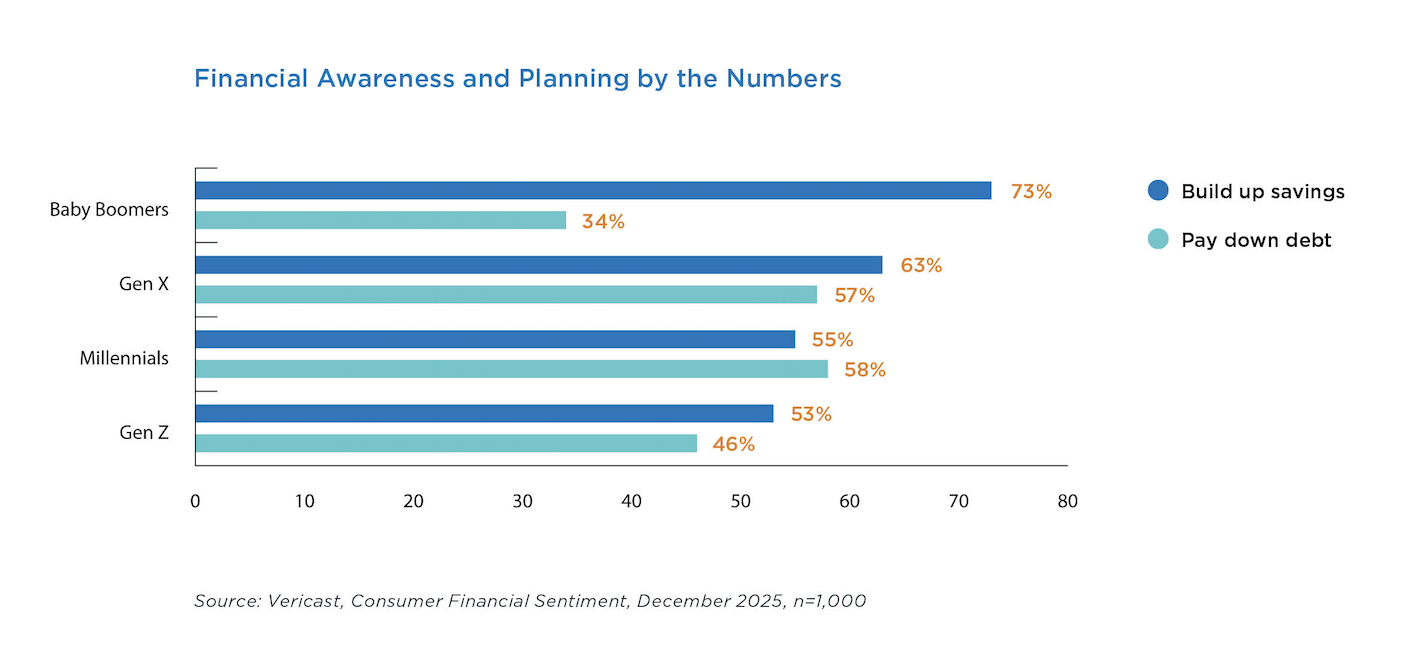

Financial Awareness and Planning by the Numbers

In a May 2025 study done by Vericast, respondents were asked if the current market uncertainty made them more aware of their finances – 85% said yes. Economic uncertainty is changing consumer behavior with 64% of total respondents saying they now monitor their bank accounts more closely. Nearly 3 out of 4 Millennials (70%) and Gen Z (74%) agree with this. Only 19% of respondents confirmed feeling “very positive” about their financial wellbeing.

Now, consumers across age demographics still feel like they’re going uphill a bit to reach better financial health. Our December 2025 study shows the top financial goals for consumers in 2026 are building up savings (60%) and paying down debt (50%).

Baby Boomers are mostly in retirement, so making sure savings are robust remains a top priority. Gen X is approaching retirement, meaning they are likely focused on entering that stage of life with little to no debt and a nice nest egg in savings. Millennials are more settled in their careers and family lives, so it’s not surprising they want to keep debt minimal while increasing savings to handle big life events or unexpected emergencies. Gen Z is aging up, with the older end of the demographic in their late 20s, a point where financial stability often becomes a bigger focus as they plan their futures.

Where to Start in Helping Consumers

Despite the rise of social platforms and AI tools, local financial institutions are seen as a trusted source by consumers – 74% of respondents say they either somewhat or highly trust local banks and credit unions. In fact, more than a third of respondents across Gen X (35%), Millennials (40%), and Gen Z (39%) say they’ve actually taken the financial advice of a local bank or credit union.

But is this trust translating across consumer financial goals? Less than half of our survey respondents say they feel “somewhat confident” that their current financial institution (FI) can help them make progress towards their financial goals. While there isn’t an outright lack of trust, something still isn’t translating between consumers leaning on their FIs for financial advice and actually feeling like they can accomplish what they want financially.

As consumers navigate the affordability crisis, credit unions must do more to demonstrate value, progress, and relevance tied to the financial needs of each member or risk losing them in the fray. Personalized guidance and relevant offers can turn existing trust into measurable progress for members.

What Consumers are Looking for in Pursuing Financial Wellbeing

Restoring consumer financial confidence requires credit unions to cast a much wider net. Guidance and education are the starting points, but it doesn’t cover everything, and consumers are clear about what they want from FIs in order to trust them.

- Lower Fees and Better Interest rates (46%)

- More Personalized Recommendations (32%)

- Tools to Track Financial Progress (30%)

- Proactive Alerts and Nudges (22%)

- Educational Content (20%)

Credit unions should provide more transparency in their communications around rate changes and offer new tools and content that align with what’s important to each generation being served. From there, offerings can be personalized to match the needs and goals of each individual member in ways that authentically help them move the needle on their finances. Balancing the desire for personalization with respect for data privacy and industry compliance will play a crucial role.

How to be Consumers’ Ultimate Partner

Financial stress isn’t an abstract concept. Account balances have a direct emotional impact on consumers, and it can feel like they will never get financial stability without the right support.

To succeed in this environment and meet the moment, credit unions must move beyond transactions, taking a steady and proactive part in members’ financial lives. That means providing guidance, offers, and tools that reflect where members are, not where institutions think they should be.

Financial confidence isn’t built overnight, but credit unions that operationalize empathy and embed financial wellbeing into every interaction will earn consumer loyalty through every financial peak and valley.

Fred Cadena is SVP, Head of Client Strategy with Vericast.