WASHINGTON–The Independent Community Bankers of America (ICBA) has published what it said is an “exhaustive analysis” of publicly available data and which it said validates what it has “long warned” about: that the “recent explosion of taxpayer-subsidized acquisitions” of banks by credit unions is harming small businesses and local communities and that community banks outperform credit unions in high-poverty areas.

The credit union trade groups have responded by comparing the bankers to “Scrooge” and by referring to a number of the assertions made by the ICBA as “myths” and the “same old tired arguments,” as outlined below.

In a blog post, the ICBA noted that siince2010 credit unions have acquired 77 community bank charters with less than $50 billion in assets—with more than 60% of these charter acquisitions (49) occurring in the past five years, according to FDIC and Federal Financial Institutions Examination Council data.

“Even more revealing, our data show these deals involve the largest credit unions, which often cross state lines to acquire community banks well outside their field of membership,” the bank trade group stated. “Since 2010, more than 80% of charter acquisitions involved a credit union with more than $1 billion in assets, while more than 40% involved a credit union headquartered in a different state than the acquired bank.

‘Counter to Claims’

“And counter to credit union industry claims, credit union acquirers aren’t saving struggling community banks. Nearly two-thirds of acquired banks saw an increase in net operating income in the five years leading up to their acquisition, while more than three in four grew their total assets in that five-year period,” the blog post stated. “The data is clear: These tax-subsidized entities are using their members’ shares to purchase well-performing institutions (and eliminating local, tax-paying community banks in the process).”

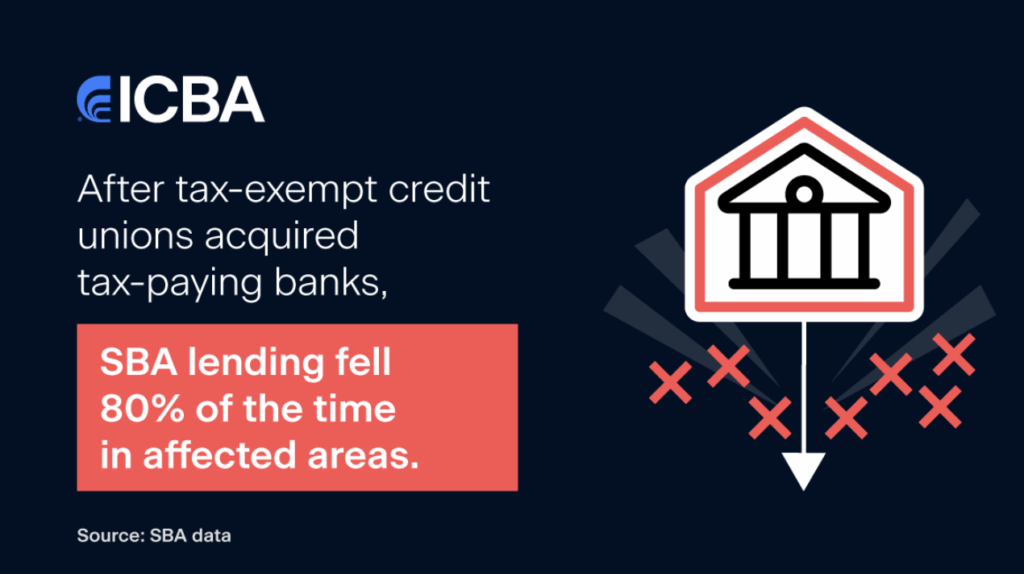

The ICBA said Small Business Administration data show the acquisitions are harming access to credit in local communities—particularly underserved areas—and “should give pause to anyone interested in preserving locally based economic growth.”

According to the SBA, the data show that since 2010:

- In areas where community banks participated in SBA programs, SBA lending fell after the acquisition nearly 80% of the time.

- Community banks have provided roughly 69.3% of SBA loans provided by banks and credit unions since 2010, compared to 2.8% from credit unions.

- In the highest-poverty counties, community banks accounted for 76.5% of SBA lending, compared with just 1.8% from credit unions—”showing community banks dramatically and disproportionately outperformed credit unions in meeting commercial lending needs in high-poverty areas.”

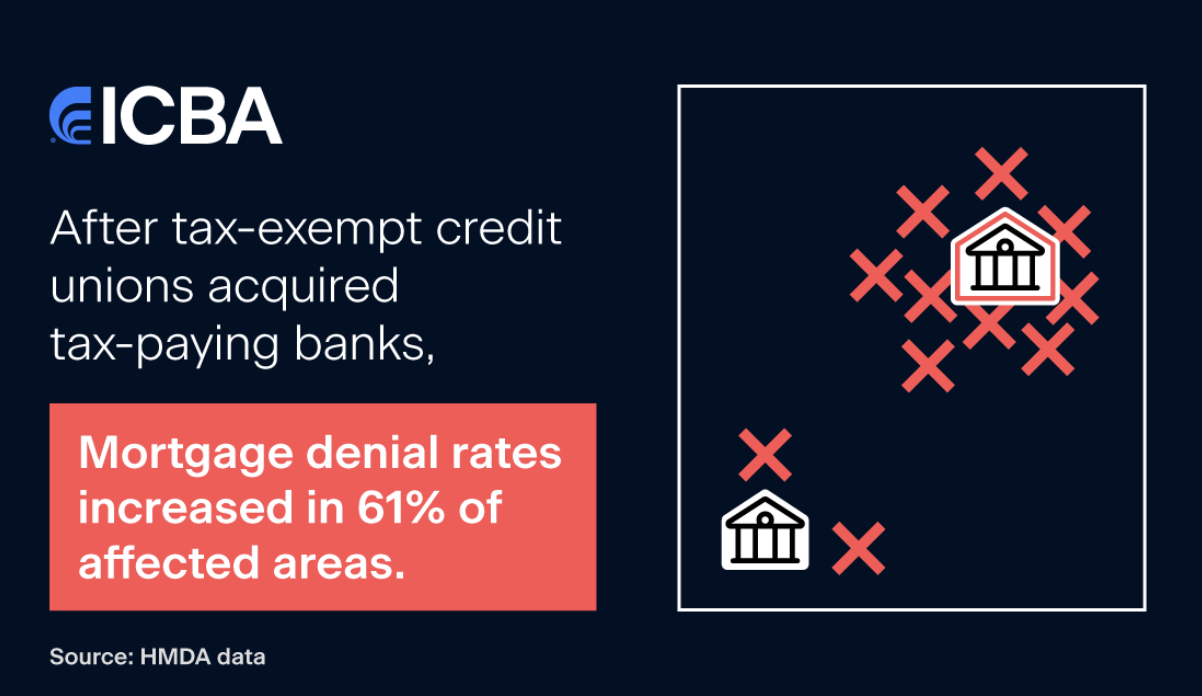

Mortgage Lending Allegedly Harmed

After repeating that “Community banks are outperforming credit unions in the lower-income communities that credit unions receive a federal tax exemption to serve,” the ICBA said its analysis of Home Mortgage Disclosure Act lending data shows total mortgage applications decreased in 57% of affected service areas following an acquisition.

It further said it found:

- The amount loaned per approved mortgage application decreased in 61% of acquisitions, while the median mortgage loan amount across all areas decreased $20,000 per loan.

- Mortgage denial rates increased in 61% of acquisitions, with a median increase of 2.1 percentage points. In areas where denial rates rose, the median increase was nearly 10 percentage points, according to the ICBA.

“This relatively high share of areas with increased denial rates and lower application volumes suggests that credit unions are not replicating the mortgage lending practices or community relationships of the banks they acquire—despite the taxpayer-subsidized industry’s claims,” the blog post states.

‘Real Economic Consequences’

According to the ICBA, its analysis reveals that overall, the “decline in small-business and mortgage lending shown in our analysis has real economic consequences on the local communities affected by credit union acquisitions of community banks, particularly in lower-income areas.”

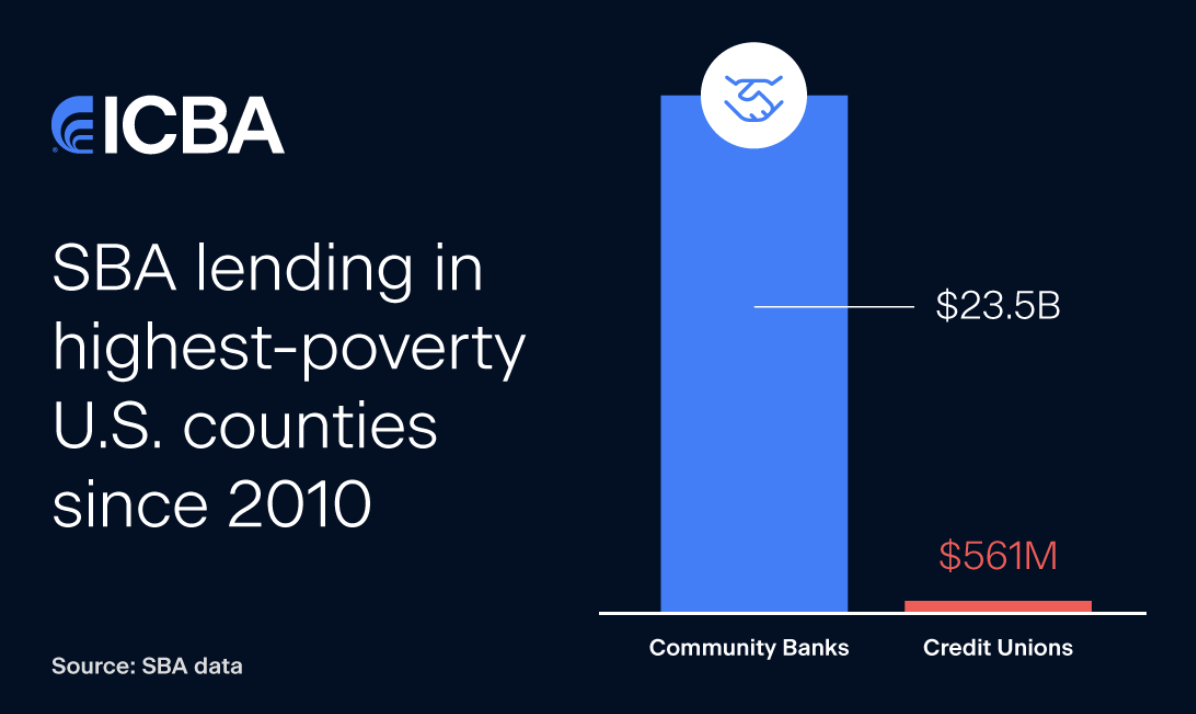

“Since 2010, community banks made $23.5 billion in SBA loans in the top 25% highest-poverty U.S. counties, compared to $561 million by credit unions,” the blog post states. “This community bank lending translated to supporting 433,227 jobs in these high-poverty areas, compared to just 16,415 jobs supported by credit unions. Overall, community banks issued a total of $305 billion in SBA 7(a) and 504 loans—nearly 25 times more than credit unions. Community bank SBA loans supported nearly 6 million jobs between 2010 and 2024, while SBA loans issued by credit unions supported 295,000.”

Moving Forward

The ICBA again called on Congress to act and to end the tax exemption for the largest CUs.

“The damage to communities highlights the inequities and perverse incentives built into federal policies that prop up this taxpayer-subsidized industry,” the ICBA stated. “Lawmakers granted credit unions a full federal tax exemption on the condition they serve defined fields of membership, but years of relaxed policies and mission creep have created conditions that are at odds with the public’s best interest.”

The trade added it will “continue to share this data as we press lawmakers to reexamine credit union policies and end the federal tax exemption for credit unions with $1 billion or more in assets—and we encourage the nation’s community bankers to spread the word as well with their members of Congress.”

DCUC: Bankers Acting Like ‘Scrooge’

Given the holidays timing of the release of the ICBA analysis, Jason Stverak, chief advocacy officer with the Defense Credit Union Council, said the bank trade group is “once again is acting like Scrooge. We hope they will be visited by the credit union ghosts of past, present and future, and understand that credit unions at the community level are very often partners with community banks and that the greater threat to the existence of community banking is not credit unions, it is the fact that many…for lack of a better term, are being gobbled up by regional and large mega-banks.

“We would hope that on the 99% of issues that credit unions and community banks agree on at the local level, that they see us as a partner and an ally to ensure that the underserved and unserved across this country in the small towns like the one I’m from have access to all the financial services,” Stverak added.

America’s Credit Unions: ‘Same Old Tired Arguments’

“The Independent Community Bankers of America (ICBA) is once again trotting out the same old tired arguments when publicly attacking credit unions,” Americas Credit Unions said in response. “When you look closely, the facts show that these attacks—as usual—miss the mark.”

America’s Credit Unions also released the following “myths vs. facts” statement, including:

“MYTH: “Across the country, credit unions are using their federal tax exemption to acquire local community banks…”

FACT: Across the country, credit unions are using their federal tax exemption to provide lower cost loans, higher savings rates, and financial counseling services for consumers trying to make ends meet. At a time when affordability is top of mind for working Americans across the country, the data clearly shows that with every type of loan—from auto to credit cards and mortgages—credit unions are making life more affordable for those who need it most.

MYTH: “In markets where community banks participated in SBA programs, those loans declined after a credit union acquisition nearly 80 percent of the time.”

FACT: The claim that credit unions lend less to small businesses relies on a selective and misleading use of Small Business Administration (SBA) data. A more honest reading of the same dataset—SBA 7(a) loan activity from 2010 to 2023—reveals that the banks choosing to sell to credit unions barely participated in SBA lending to begin with. After acquisition, those same branches increased their small business lending under credit union stewardship. The numbers are not ambiguous. The rhetoric is.

MYTH: “…lawmakers should treat credit unions over $1 billion in assets the way they operate — like tax-paying commercial banks.”

FACT: Credit unions’ tax status is due to their not-for-profit cooperative structure, where their members are the owners. Credit unions succeed when their members succeed. No matter the size, it’s their structure and focus on the member that is the determining factor to being a credit union. Whether they have $50 million or $10 billion in assets, that structure remains the same. The data has proven this for the better part of a century. Credit unions, large and small, offer better prices and services because they aren’t focused on making money off their members. The profits go back to members.

MYTH: “Consumers hear the jingles marketing ‘great rates for everyone’” is bad?

FACT: It’s not bad for consumers. Bankers hate the competition, and they would like Congress to eliminate credit unions so they can charge more. Independent research reinforces this reality. A study from American University shows that the mere presence of credit unions in a local market drives down costs and improves products for consumers across the board. Competition works. In fact, Americans benefit by roughly $23 billion each year due to the competitive pressure credit unions place on banks. If that is the ICBA’s definition of a market distortion, most consumers would welcome more of it.

‘Everyone Benefits’

“Consumers deserve to know if they are eligible to join a credit union and access affordable rates,” America’s Credit Unions said. “Everyone benefits from the presence of credit unions, even if they don’t use one.”