MADISON, Wis.–A new analysis—which includes a forecast for rates in 2025– shows loan balances have risen, but not at smaller CUs; delinquencies have been rising, but are expected to improve, and membership growth continues to outpace U.S. population growth overall.

Those findings and other forecasts are included in the January Trends Report published by TruStage, which is authored by the company’s chief economist, Steve Rick.

Here’s a look at how credit unions performed by category, according to the Trends Report:

Total Credit Union Lending

Credit union loan balances rose 0.4% in November, above the 0.3% pace reported in November 2023. Driving overall loan growth was strong growth in home equity lending (1.6%), unsecured personal loans (1.0%), adjustable-rate mortgages (0.8%) and credit card loans (0.7%),” the analysis states.

It notes November seasonal factors typically subtract 0.22 percentage points from the underlying trend loan growth as winter weather slows auto and home purchases.

Member Balances Grow

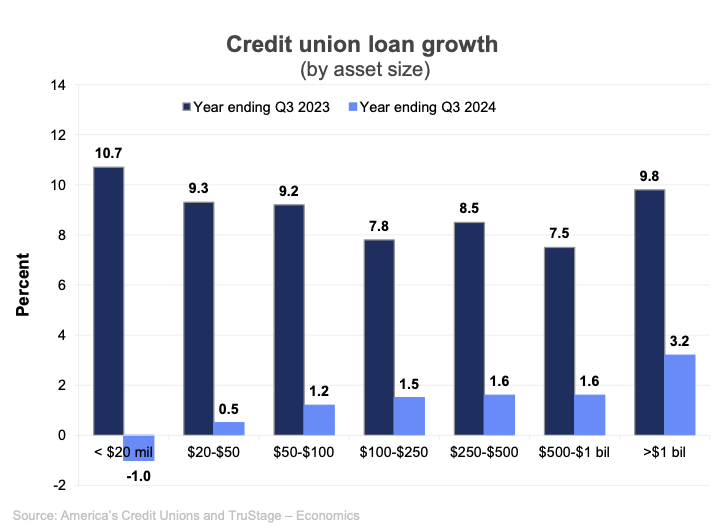

“Over the past 12 months, total credit union loan balances rose 2.4%, below the 7.2% long-run average,” Rick said in his analysis. “However, industry average growth rates mask big disparities between large and small credit unions. In the year ending in the third quarter of 2024, credit unions with assets greater than $1 billion reported a 3.2% increase in loan balances, which was down significantly from a similar period one year earlier.”

The report added that during the same period, credit unions with assets less than $20 million reported loan growth of -1.0%, which is significantly below the 10.7% pace set a year earlier (see figure above).

“We expect overall credit union loan growth to rise to 5% in 2025 due to lower interest rates, faster deposit growth lessening credit union liquidity pressures and rising consumer demand for durable goods,” Rick forecast.

Consumer Installment Credit

According to the new report, credit union consumer installment credit balances (auto, credit card and other unsecured loans) rose 0.1% in November, above the 0.2% decline set in November 2023, as consumer spending grew in the fourth quarter of 2024.

“Credit union consumer installment credit fell 1.4% over the last year, which is significantly below its 30-year average annual growth rate of 6.3%, and below the 7.1% rise in total real estate loans,” the report states. “The last time credit union consumer installment loan balances fell into negative territory was during the tail end of the Great Recession in 2011.”

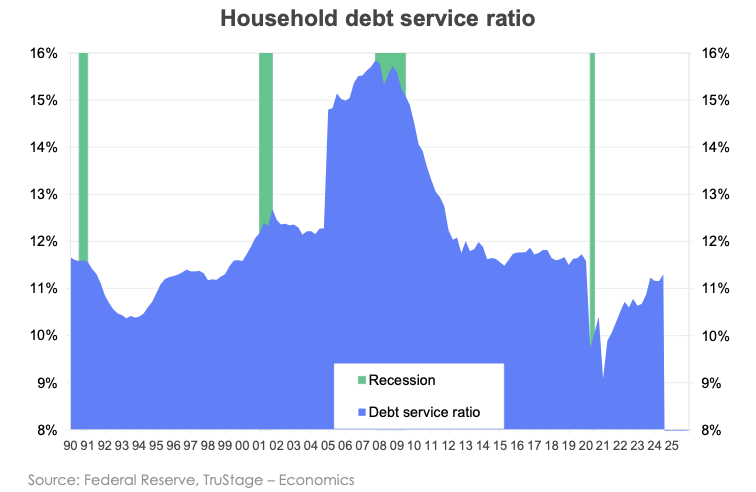

Household Debt Service

The Trends Report shows the household debt service ratio (mortgage and consumer debt payments required to remain current on that debt as a percent of disposable income) rose to 11.3% in the third quarter, from the 11.2% reported in the second quarter, and above the record low of 9.1% reported in the first quarter of 2021, according to the Federal Reserve.

The 2021 record-low debt service ratio was caused by record-low interest rates and government stimulus checks, which were used to pay off debt.

“The current 11.3% debt service ratio is below the 13% average reported during the 2000-2019 time period and significantly below the high-water mark of 15.8% set right before the onset of the 2008-2009 Great Recession,” the report states. “So, most consumers are not overly burdened with debt.”

Looking Forward

Looking into 2025, Rick is forecasting high interest rates and the repricing of adjustable-rate credit will mean higher spending on servicing debt, which will increase the debt service ratio.

“This will reduce household disposable income for spending on goods and services or will decrease the national savings rates,” the Trends Report predicts.

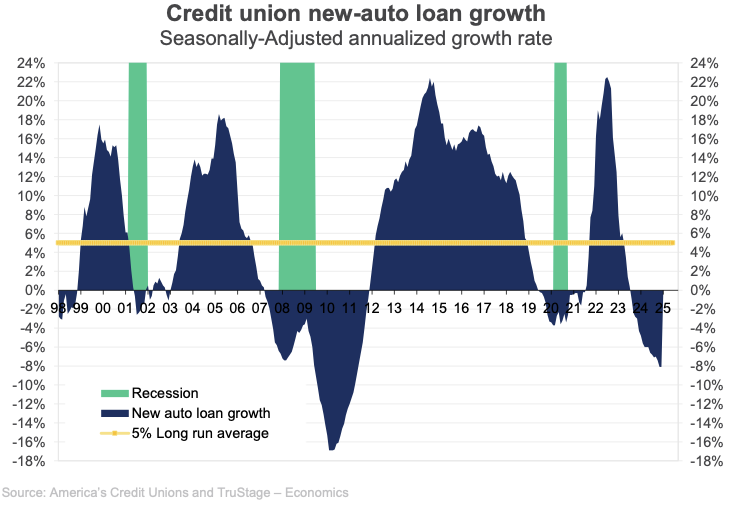

Vehicle Loans

Credit union new-auto loan balances fell at a -8.1% seasonally-adjusted annual rate in November, significantly below the -4.3% pace set in November 2023, “due to high lending interest rates, strong competition from finance companies, tight liquidity pressures causing some credit unions to pull back from lending, increased vehicle incentives by manufactures, and tighter lending standards reducing the availability of credit,” the report states.

November is typically one of the slower months of the year for credit union new-auto loan originations as seasonal factors subtract 0.35 percentage points from the underlying trend growth rate due to normally weak new auto sales, the Trends Report added.

About Auto Prices

It further notes new auto prices rose 0.6% in November from October but are down 0.6% during the last 12 months, according to the Bureau of Labor Statistics, increasing the size of the auto loan to finance the auto purchase. Used auto prices fell 3.3% during the last year leaving consumers with less equity from their trade-ins when purchasing a new vehicle.

“Expect auto sales to rise above the 17 million pace in 2025 due to continued job growth, lower interest rates and a steady growth in inventories,” the report observes. “If inflation pressures reassert themselves, however, this will keep interest rates higher for longer, eliminating one of the key factors driving new vehicle sales in 2025.”

Real Estate Information

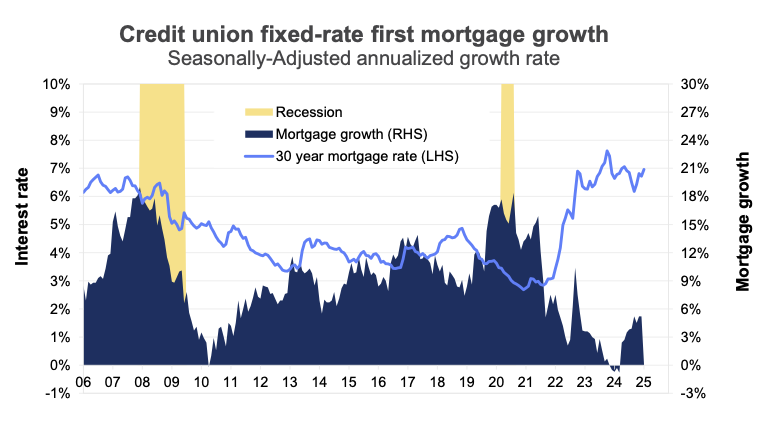

The new Trends Report shows credit union fixed-rate first mortgage loan balances rose 0.3% in November, above the 0.1% decline set in November 2023.

“Existing home sales rose 4.8% in November from October to a seasonally-adjusted annual rate of 4.15 million and are up 6.1% from the year earlier,” Rick stated. “But sales are still below the five-million annual sales rate considered to be a healthy housing market due to high interest rates and poor affordability. Fixed-rate mortgage loan balances are currently rising at a 5.4% seasonally-adjusted annualized growth rate (see figure below) due to lower mortgage rates.

“With the Federal Reserve expected to lower short-term interest rates 50 basis points in 2025, and the 10-year treasury interest rate expected to remain around 4.5%, expect the 30-year mortgage interest rate to remain in the 6.5% – 7.0% range for 2025,” the report added.

The analysis shows U.S. home prices climbed to a record high in November amid the lowest housing affordability in four decades.

Dream Homes or Just Dreams?

“Following two years of double-digit growth, the housing market remains overvalued so expect home prices to level off or only increase 2-3% during the next two years,” Rick said in his forecast. “The U.S. national homeownership rate came in at 65.6% in the third quarter of 2024, down from the 66% during the third quarter of 2023. Today’s homeownership rate is above the 62.9% nadir reported in the second quarter of 2016, but below the 69.2% apex reached in the fourth quarter of 2004.

“Expect mortgage originations to rise 10% in 2025 as the economy continues its expansion and mortgage interest rates fall approximately one-half of a percentage point throughout 2025,” the forecast added.

Savings & Assets

Credit union savings balances rose 1.0% in November, better than the 0.3% increase reported in November 2023, due to the month ending next to a payroll Friday and lower market interest rates removed some of the competitive pressure from money market mutual funds, according to the Trends Report.

The analysis added that November’s seasonal factors typically subtract 0.2% percentage points from the underlying savings trend growth.

Additional Data Points

Among the other data points in the report:

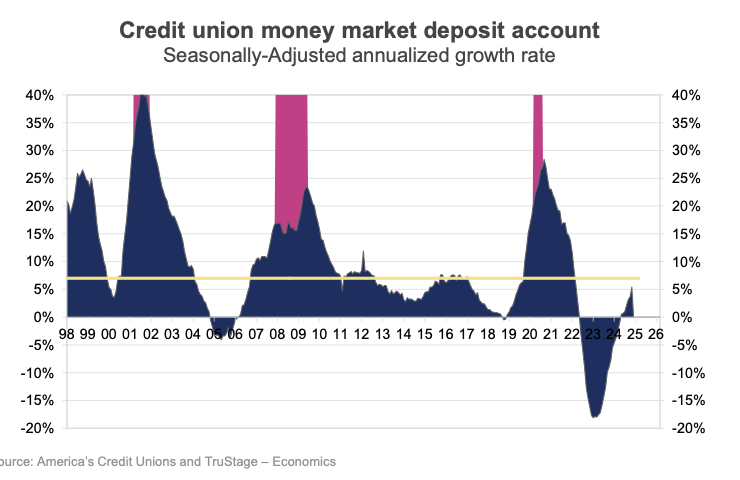

- Credit union money market deposit account balances are currently growing at a 5.4% seasonally-adjusted annualized growth rate, which is below the 7% long-run average, but better than the negative numbers reported during the last two years.

- With the Federal Reserve lowering short term interest rates during the last few months, this has lowered the yield on money market mutual funds and therefore the competitive pressure faced by credit unions for these type of deposits.

- The average credit union member was sitting on $13,808 in deposits in November 2024, up $411 from the $13,397 set back in November 2023. “This is a 3.1% increase in the dollar amount of deposits per member,” the report states. “So, If the Federal Reserve keeps lowering interest rates this year and the household savings rate increases to its 6% long run average, we could see the annual growth rate of the savings-per-member ratio eventually return to its long run 4.5% average over the next year.”

“What’s Expected”

Rick said he expects credit union savings balances to rise 6.5% in 2025, below the 7% long run average but better than the 5.5% reported in 2024 due to rising real incomes, a rise in the personal savings rate (personal savings as a percentage of disposable personal income), and more competitive credit union deposit interest rates.

“This additional liquidity will be welcomed by many credit unions facing tight liquidity conditions in 2024,” Rick added.

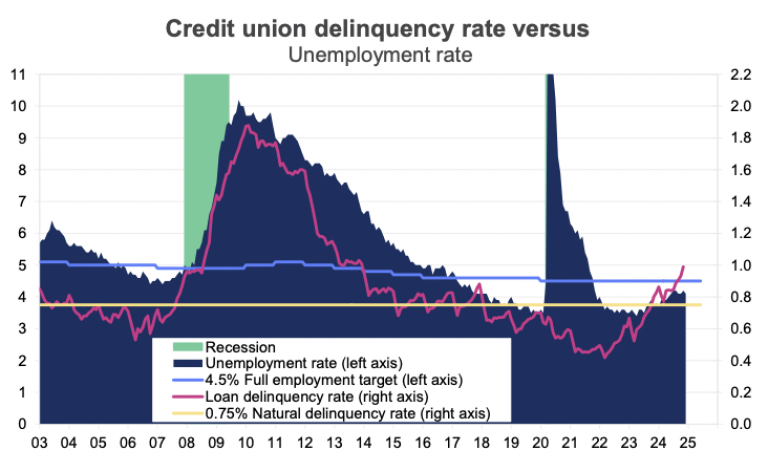

Capital & Other Key Measured

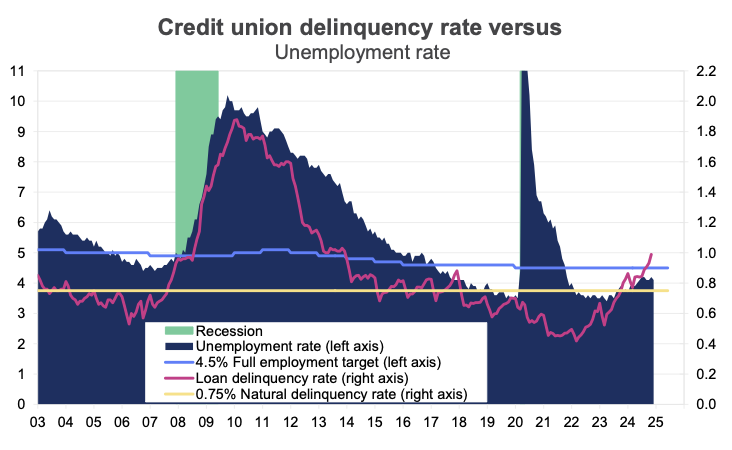

The credit union loan delinquency rate (loans two or more months delinquent as a percent of total loans outstanding) rose to 0.99% in November from 0.93% in October which is in line with the traditional seasonal pattern, according to the Trends Report.

“Delinquency rates typically reach their nadir in any year’s first quarter as members use tax refunds and bonus checks to catch up on any late loan payments,” the report states. “As the year progresses, delinquency rates slowly rise and reach their apex late in the fourth quarter.”

The report further notes credit union loan delinquency rates are now significantly above their 0.75% long-run natural delinquency rate, after six years of below trend numbers.

Six Factors

According to Rick, six factors explain the rising loan delinquency numbers during the last couple of years:

- Falling real wages

- High rent inflation

- Student loan payment resumption

- Rising interest rates on adjustable-rate loans

- Some members dropping car insurance due to high premiums

- A rather large denominator effect due to loan balances rising slower than the dollar amount increase of delinquent loans.

Loan Quality Measures to Improve

“Expect loan quality measures to improve slightly during 2025 due mainly to faster loan growth affecting the denominator of the ratio,” Rick wrote, before cautioning, “But keep an eye on possibly higher interest rates causing repricing of adjustable-rate loans into higher loan payments and therefore squeezing households’ budgets. Since the delinquency rate is a ratio its important to compare the growth rates of the numerator (dollar amount of delinquency loans) and the denominator (total loans). During the last year, the numerator increased 26.2% while the denominator rose only 2.4%.

“This increased the delinquency ratio 23.7%, from 0.80 in November 2023 to 0.99% today. The 23.7% growth rate can be approximated by subtracting the denominator growth rate from the numerator growth rate, (26.2% – 2.4% = 23.8%),” the report states.

Credit Unions & Members

Credit union memberships grew 177,000 in November, or 0.12%, which is like the 176,000 new members, or 0.12%, that were added in November 2023, the Trends Report analysis shows.

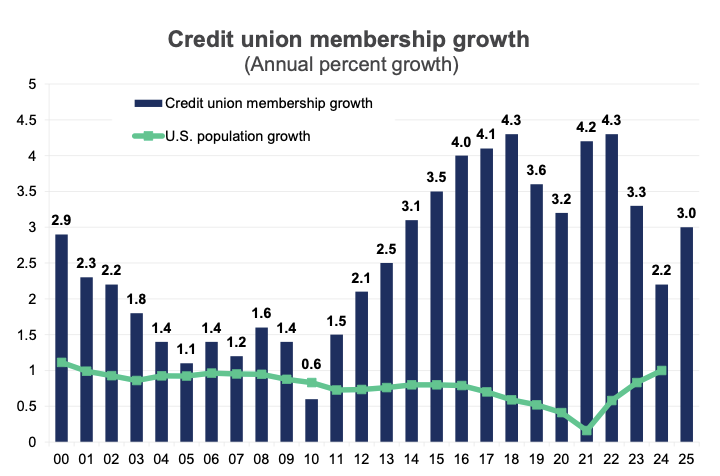

Year-to-date, credit unions added 2.973 million new members, slower than the 3.924 million members added during a similar period in 2023. During the last 12 months, credit union memberships rose 2.2%, the slowest pace since 2012.

“Credit union membership growth of 2.2%, however, is still outpacing the 1.0% growth rate of the U.S. population, indicating credit unions are increasing their market share of the financial services marketplace,” Rick wrote.

Total Membership

The Trends Report shows total credit union memberships reached 144.7 million in November, 3.0 million more than November 2023. Strong home equity lending and modest job hirings are two major factors driving the rise in memberships, the report states.

“Job growth is historically a major factor determining credit union membership growth,” The Trends Report analysis added. “The U.S. economy added 2.0 million jobs during 2024, according to the Bureau of Labor Statistics, down from the 2.6 million added in 2023. For 2025, expect only 1.5 million new jobs to be created as immigration slows, economic growth slows to its potential growth rate and the labor market reaches equilibrium.

The Forecast

“Slower job growth will weigh on membership growth while better loan growth numbers will both be major factors impacting membership growth,” the report added. “We expect the pace of credit union membership growth to rise to 3.0% in 2025 while the U.S. population growth rate falls to 0.75%.”