SANTA MONICA, Calif.—More than one-in-four new vehicle trade-ins are underwater, a new analysis has revealed.

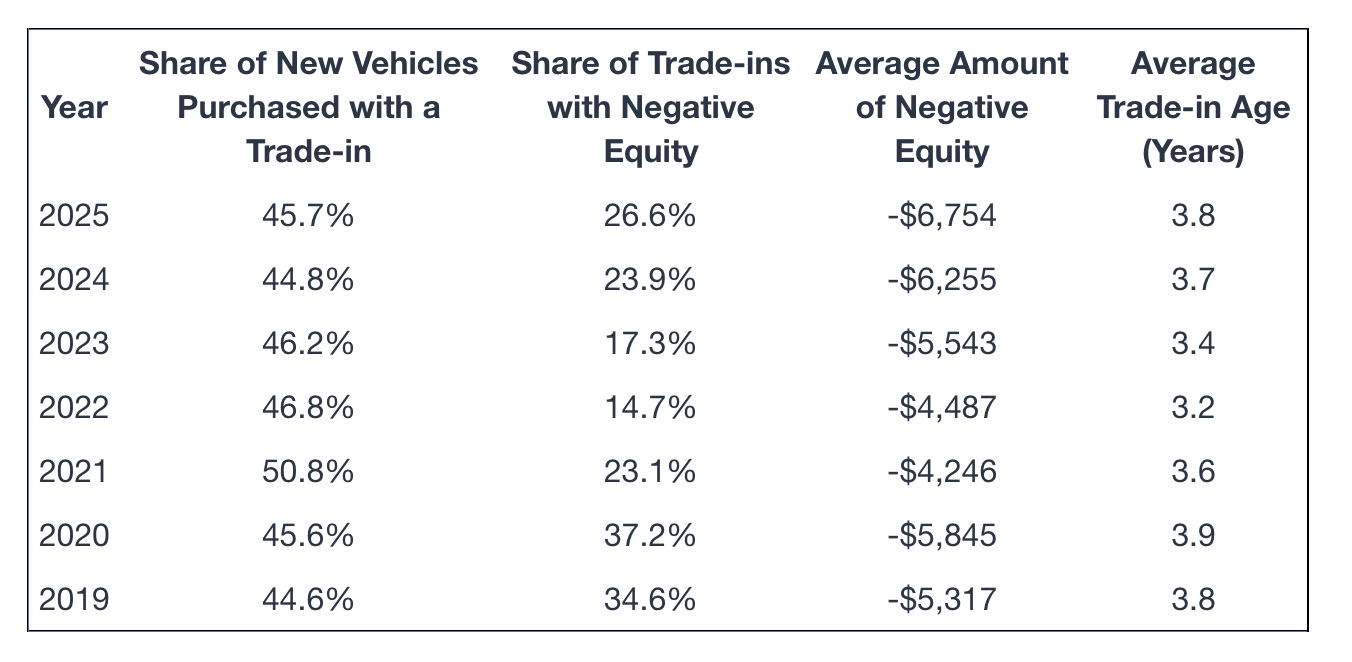

According to Edmunds, that marks a four-year high, with the company reporting that 26.6% of trade-ins toward new car purchases that had negative equity in Q2, up from 26.1% in Q1 this year and 23.9% in Q2 2024.

In 2021, 31.9% of new-car trade-ins were upside down, the Edmunds data show.

Edmunds further reported the average amount owed on upside-down loans in Q2 was $6,754, which was down from $6,880 in the first quarter of the year but still up from 2024’s $6,255.

‘Compounding the Negative Effects’

“Affordability pressures, from elevated vehicle prices to higher interest rates, are compounding the negative effects of decisions like trading in too early or rolling debt into a new loan, even if those choices may have felt manageable in years past,” Ivan Drury, Edmunds’ director of insights, said in a statement. “And as buyers take on new loans with much higher interest rates than those from just a few years ago, even potential tax deductions can’t meaningfully offset the thousands more they’ll pay in interest.

“With a growing share of upside-down owners thousands of dollars in the red, many are at risk of getting stuck in a cycle of debt that only grows harder to break over time,” Drury added.

Monthly Payments Climb

According to Edmunds, the average monthly payment for buyers who rolled negative equity into a new loan climbed to $915 in Q2, which the company said is the highest on record for this group and $159 more than the overall industry average of $756.

That group of buyers also financed $12,145 more than the typical new-vehicle buyer, Edmunds added.