NEW YORK — More than 3.5 million federal student loan borrowers fell into default after pandemic-era protections ended, with many of the borrowers older and already financially strained, according to a new analysis from the Federal Reserve Bank of New York.

The New York Fed said approximately one-million borrowers entered default during the fourth quarter of 2025, followed by another 2.6 million borrowers in the first quarter of 2026 after missed payments again began appearing on credit reports.

The report marks one of the clearest pictures yet of the financial fallout following the end of the federal student loan payment pause that began during the COVID-19 pandemic.

Getting Older

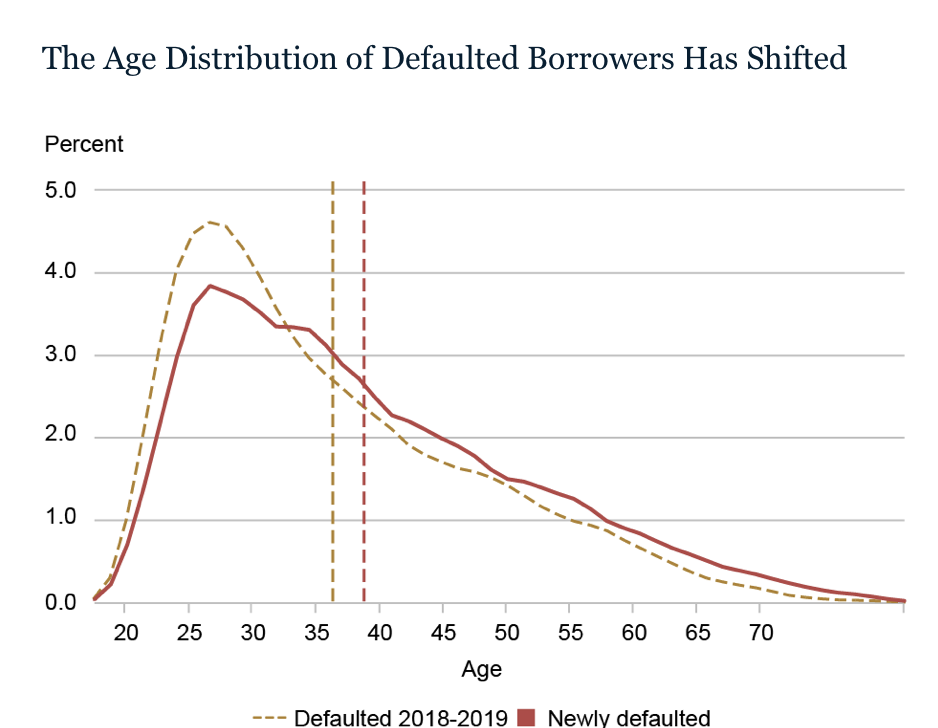

According to the New York Fed, borrowers in default are now older on average than before the pandemic, with the typical borrower nearing age 40. Borrowers age 50 and older also are increasingly represented among those falling behind on payments.

The Fed’s researchers said borrowers entering default were more likely to live in Southern states and often already carried other forms of debt distress. While many had remained current on their loans before the pandemic, the resumption of payments following years of paused obligations appears to have strained household finances.

The New York Fed reported that about 2.6 million borrowers were more than 120 days delinquent and had been referred to the U.S. Department of Education’s Default Resolution Group during the first quarter.

Additional Findings

The report also found:

- The student loan delinquency rate rose to 10.3% during the first quarter.

- The transition rate into serious delinquency fell to 10.9% from 16.2% in the prior quarter.

- Overall U.S. household debt rose modestly to $18.8 trillion, even as student loan stress increased.

Researchers warned additional defaults could occur as borrowers transition away from the Biden-era SAVE repayment program, which had temporarily reduced or suspended payments for millions of borrowers.As the CU Daily reported here, U.S. household debt climbed to a record $18.8 trillion during the first quarter of 2026, as mortgage, auto loan and home equity borrowing increased, according to new data from the Federal Reserve Bank of New York.