DENVER — Mortgage lenders closed out 2025 with a lower critical defect rate in the fourth quarter, although compliance-related problems and borrower eligibility issues continued to pressure loan quality, according to a new report from ACES Quality Management.

The company said its quarterly ACES Mortgage QC Industry Trends Report covering Q4 2025 and the full calendar year (CY) 2025. The report, released Wednesday, analyzed post-closing quality control data from its ACES Quality Management & Control software platform.

The Key Findings

According to the report:

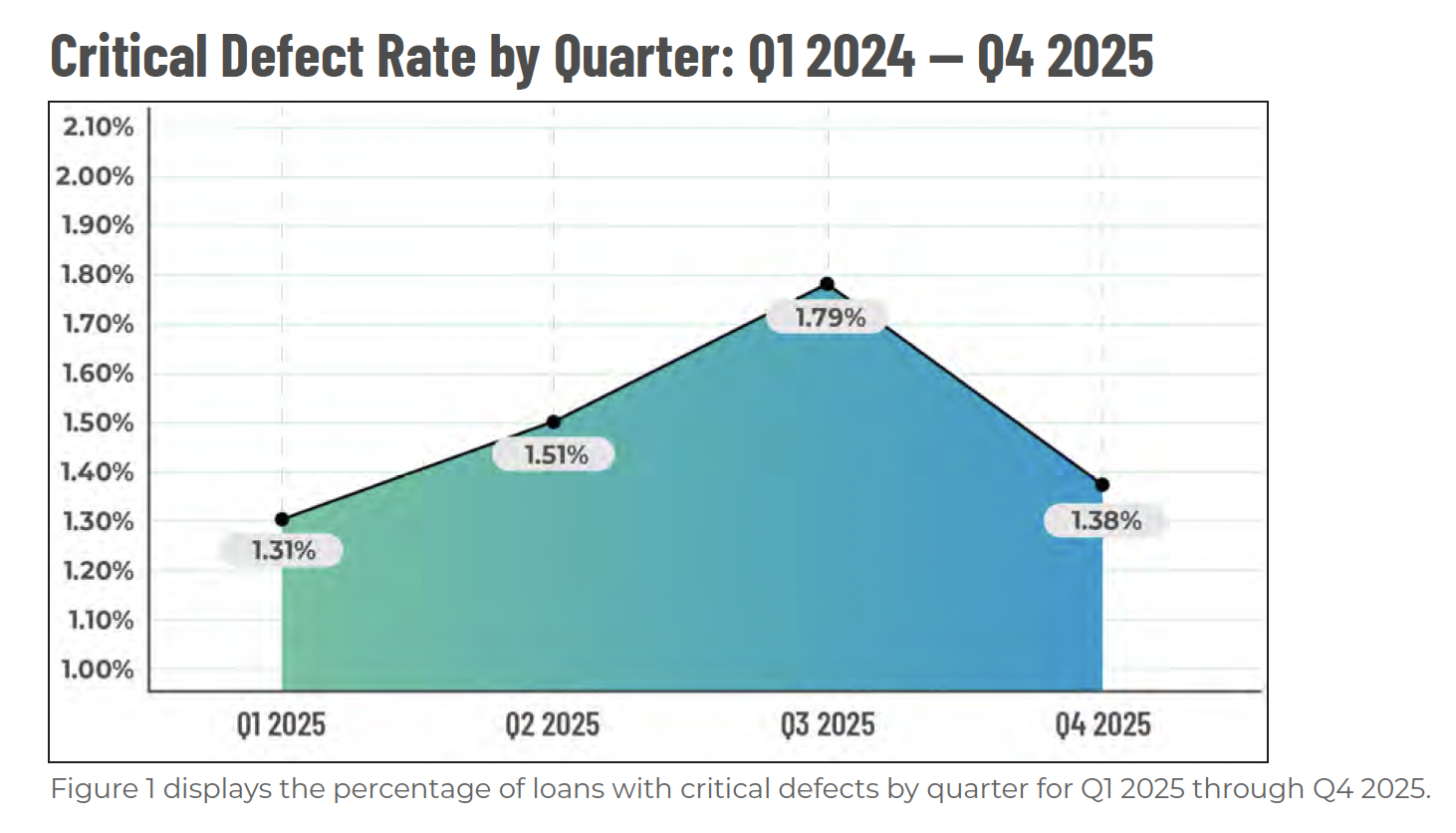

- The overall critical defect rate fell to 1.38% in Q4 2025, down 22.91% from 1.79% in Q3 2025. ACES said it marked the first quarterly decline after three consecutive quarters of increases.

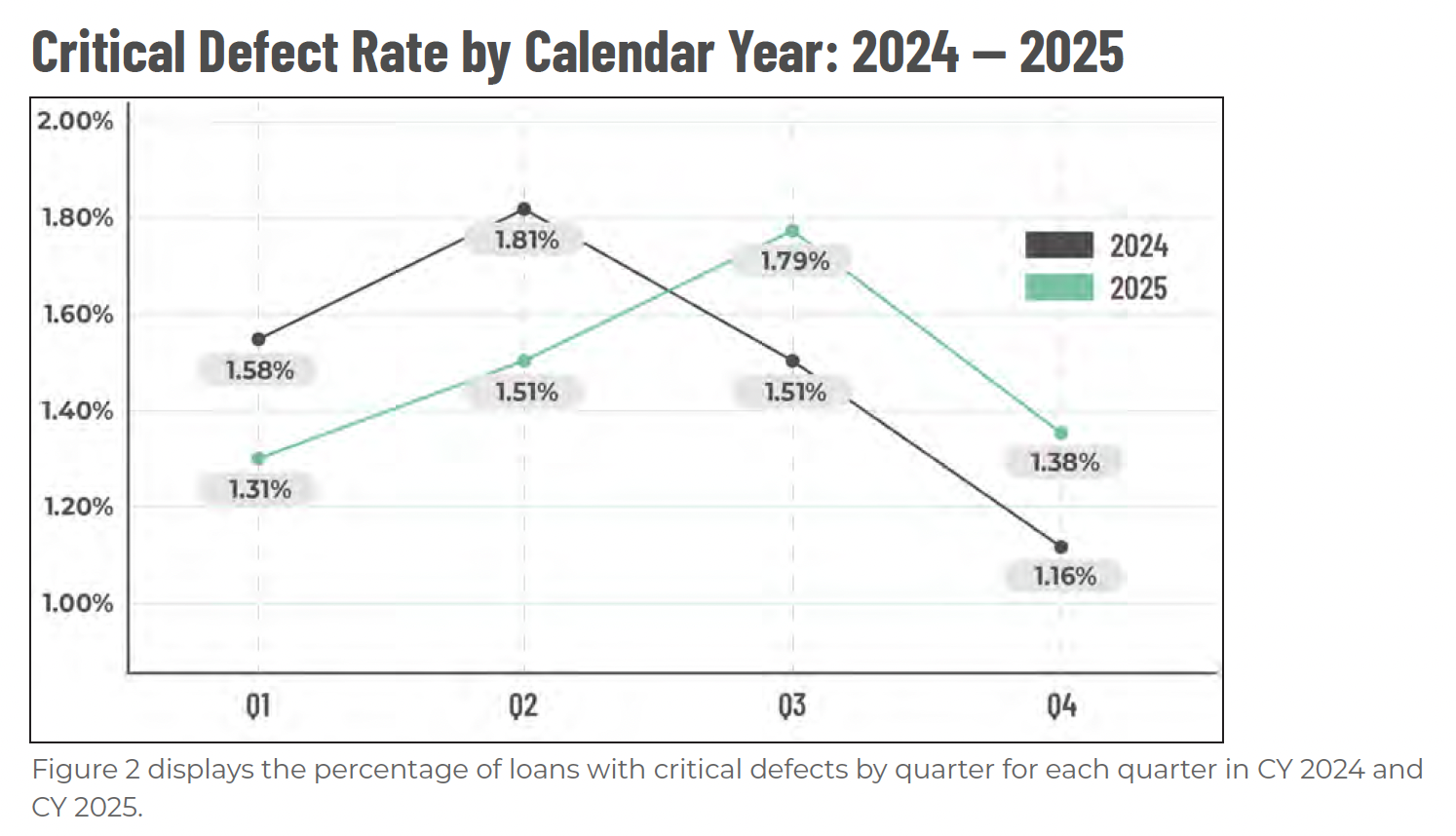

- The average critical defect rate for all of 2025 was 1.50%, essentially unchanged from 1.52% in 2024.

- Legal, regulatory and compliance defects became the leading category in Q4 2025, increasing 30% from 18.97% to 24.66%. ACES said it was the second time the category had ranked first since Q4 2024 and represented its third consecutive quarterly increase.

- Income and employment defects fell 21% to 21.52%, dropping out of the top spot for only the second time since Q4 2024.

- Borrower and mortgage eligibility defects increased 291.58% year over year in 2025, while credit-related defects rose 166.13%, which ACES said reflected a growing number of borrowers stretching to qualify amid affordability pressures.

- Refinance review share nearly doubled during 2025, rising from 11.14% to 21.04%, while refinance defect share more than doubled from 15.30% to 32.20%.

- Federal Housing Administration loan defect share remained elevated at 30.86% for the year relative to review share, while Veterans Affairs loan defect share rose for the second consecutive quarter in Q4.

‘Shift’ Taking Place

“Lenders ended 2025 on a strong note, with Q4 delivering a meaningful drop in the critical defect rate and the full-year average holding essentially flat versus 2024,” Nick Volpe said in a statement released with the report.

However, Volpe said the industry’s shift toward “eligibility-driven defects” as refinancing activity returned suggests lenders will need tighter documentation and more consistent eligibility reviews in 2026.

ACES said the report is based on loan audits selected by lenders for full-file reviews using its benchmarking system. The company said its clients include more than 70% of the nation’s top 20 independent mortgage lenders, seven of the top 15 U.S. credit unions and 14 of the top 30 banks.