LAS VEGAS–What happens to credit unions seeking loans that focus only on making loans? They don’t just miss loan opportunities, they miss opportunities for long-term growth, according to one person.

During a session at NACUSO’s Reimagine Conference here, Samantha Paxson, the CEO and founder of Power & Light Collaborative who is well-known to many throughout credit unions, offered research-based insights on why the best strategy for any credit union is to focus on member-centricity and human-centricity.

“Our strategy has to evolve to make sure that we are super-relevant and super-critical in our members’ lives,” said Paxson. “My challenge to all of you is to be the leader who transforms mediocre, undifferentiated experiences into something that is exceptionally bold and that makes you essential to consumers today.”

Where to Begin

And where should that journey begin? Paxson suggested heading straight to the typical credit union’s website, which is most likely dominated by product rates.

“That’s our model. We do loans. and loan interest income makes up the majority of our net income. And loans have been our value proposition for many years,” said Paxson. “But when you look at other providers, it’s different. When you look at Chime, it’s grown to double the size of Navy Federal in just 10 years. They have 24-million customers and they are just killing it. Look at what they are leading with–they are leading with daily transactional use-cases.”

Product Pushers

In contrast, Paxson said, when she looks at credit unions’ sites she usually encounters a singular focus on pushing products, with rates being the value prop.

“Now, we need deposits and we need a reason for consumers to come into our environment and do business with us,” Paxson stated, noting members have a broad range of needs and only get a new loan, on average, every five to seven years.

“When you think about the big value prop of credit unions, why do we exist? What I hear at this conference and many other conferences is that we’re looking for products, we’re looking for shiny objects that will get people to come into our environment and do business with us,” she said. “But we have to know what’s actually going to drive member utilization. Are we people centric, designing our credit unions around our members? Or, are we product centric? It’s kind of a provocative question. Yes, people are looking for low rates, but they’re also looking for convenience, they’re trying to get things done in their financial lives in their short-term world and in their long-term world.”

How to Get to 67% Growth

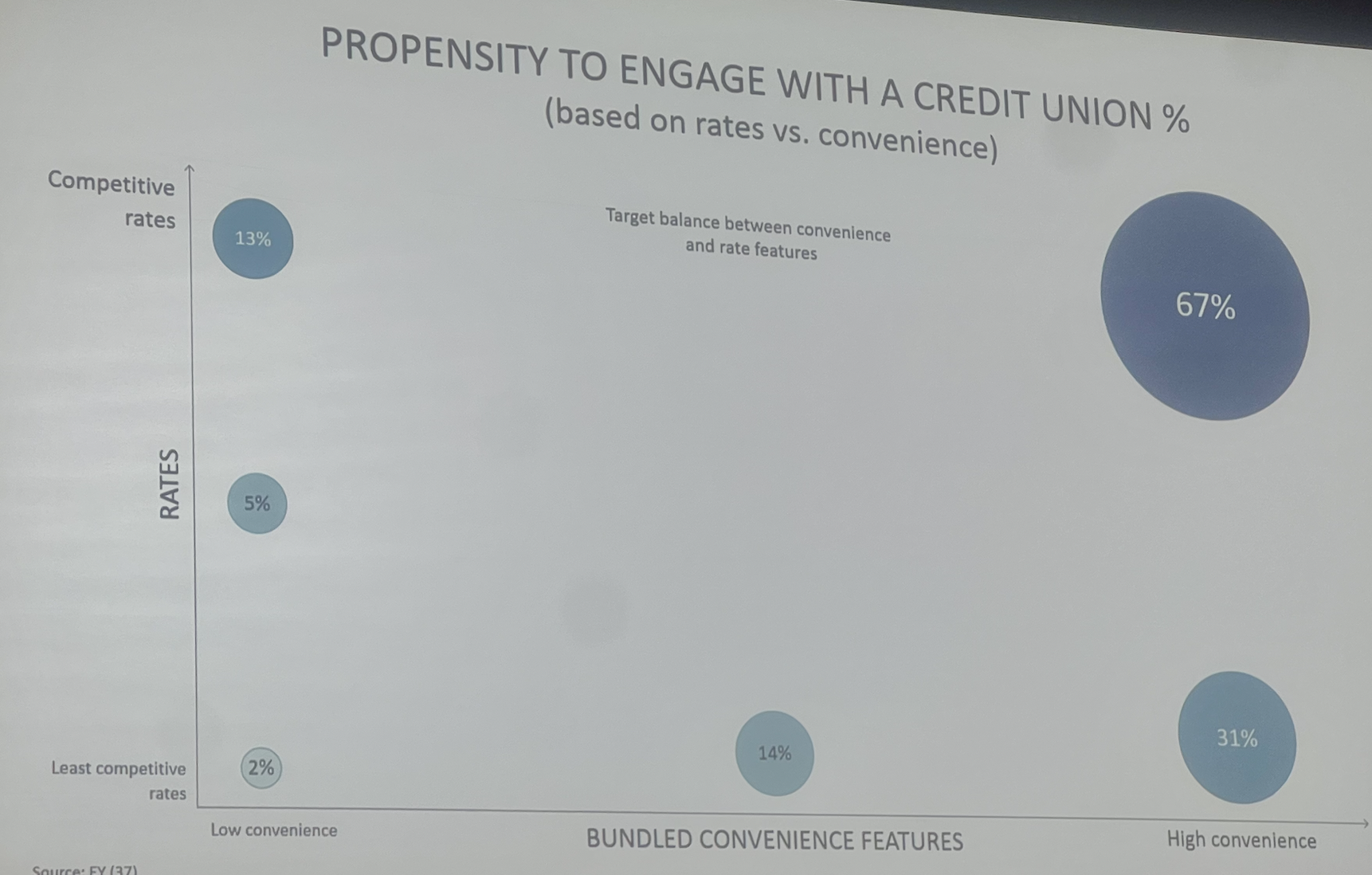

Paxson cited the extensive research that has been conducted by EY over the past five years on credit union member behaviors and thinking.

“We looked at the data around rate performance versus having convenient tools that are going to help me in my daily life,” she explained. “If you have the least competitive rates you can expect to grow by 2%. If your rates are more attractive and more competitive, you can expect utilization to go up and new member acquisition to go up by 5%. If you have the most competitive rates, you get to 13% growth.

“Now, if you go along the convenience scale and you build out convenience features within your credit union…you can expect to grow by 31%. If you do both–if you have the best rates in town and you are the most convenient—you can expect to grow 67%. You want to find that balance in the way that you put your credit union together and balance your investment. If you can find that equilibrium…you will a have really strong proposition around how you grow member deposits, how you grow new members and how you get them using your credit union again.”

The Key & the Culprit

What’s key, said Paxson, is understanding what human centricity means. CUs need look no further than Amazon for an example. It’s why the company has become the expectation consumers now have for every provider, she added.

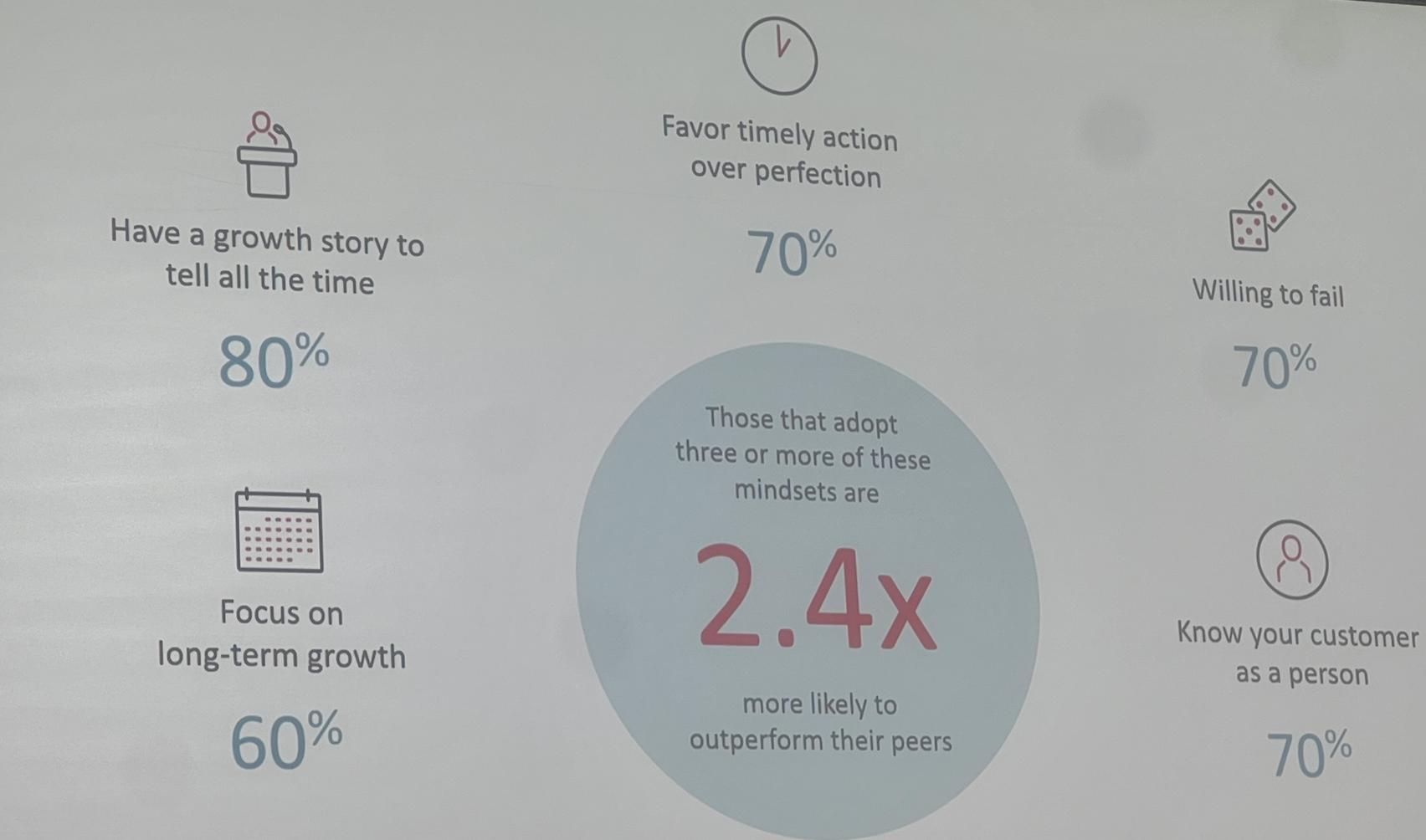

In a market in which most credit unions are not hitting their ROA targets, one big culprit is that even CUs that have a good strategy are struggling to implement it, according to Paxson.

“Three out of four leaders have identified a strategy, but they’re struggling to pull it through their organization. There is a gap between credit union strategy and actual execution,”

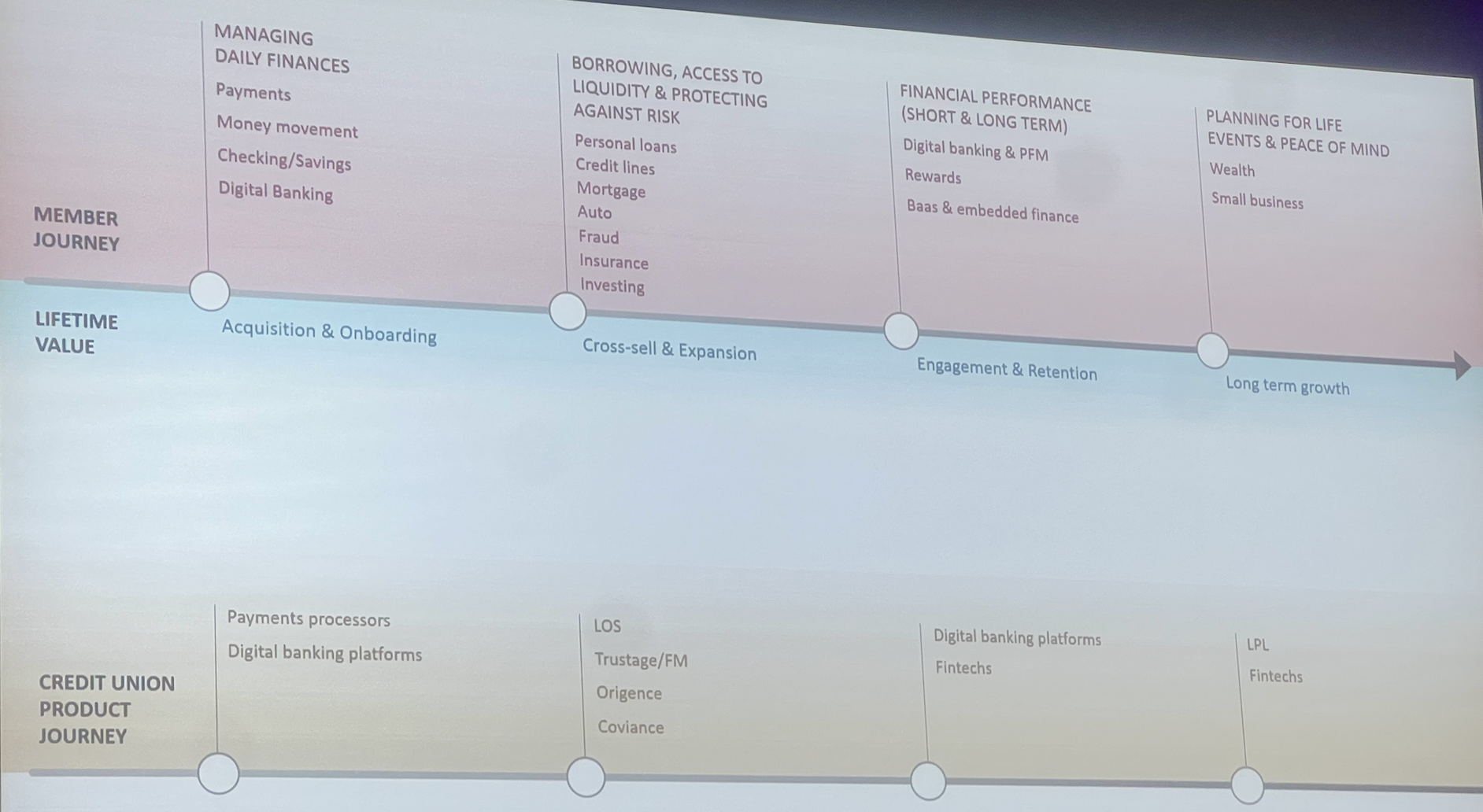

One way to adequately fill that gap, Paxson told the meeting, is to understand how a member moves through a credit union. That member journey is not product-centric,” she said.

Where to Begin

To be member-centric, Paxson, advised, begins with:

- Knowing the market

- Knowing strategic focus

- Having internal alignment

- Having product experience

- Knowing the technology stack

- Knowing the ecosystem.

And yet even knowing all that, Paxson reminded, “What got you here won’t get you there.”

Paxson cited additional research showing the average consumer has 40 different financial relationships. Moreover, 40% of global consumers are now potential nomads who are open to self-assembling their own suites of banking products.

‘Tremendous Opportunity’

“How do we get the empowered consumer to do all of this with you? That is the goal,” Paxson said. “There is tremendous growth opportunity in the market and we’re barely scratching the service.”

Paxson said that having cross-brand opportunities in the digital marketplace can help improve client retention and reengage existing members, as 82% have also said they would be receptive to product offers outside the traditional financial services ecosystem.

“If you can deliver personalized experiences in the way the consumer expects, you will double your market share,” Paxson said. “We need to have a growth mindset. We think we’re the guys and gals that can’t compete. We can. We need to think about long-term growth.

The Daily Interactions

“What Chime does really well is focus on more timely action,” Paxson continued. “They are focused on daily interaction. They really understand their consumer as a person. One thing all growing organizations have in common is human-centricity.”

Rather than loans, Paxson urged CUs to think more about payments as touch points, as the average person engages in some form of payment as much as 12 times per day.

“Get out of the life-stage business and get into the lifestyle business and focus on what’s next,” she advised. “Think about how and when members engage. You’re focused on loans and hoping they do micro-transactions with you. I am recommending you flip it and focus on micro-interactions. It’s land and expand. Get them in on something small and then start moving them across your credit union.”