ALEXANDRIA, Va.–The NCUA Board was given an update on the 2026/27 budget for the Central Liquidity Facility (CLF), which like the agency itself, is smaller than in years past.

At several points before and during the update, Chairman Kyle Hauptman encouraged more credit unions to join the CLF, which provides liquidity to credit unions when needed, noting it’s one of the rare examples of insurance that has no cost and which pays the policyholder.

“Most insurance costs you money out of pocket and, maybe, if you use it, you get some back,” said Hauptman, adding that CU deposits with the CLF are currently earning a yield of 3.5%-3.6%, the equivalent of what is paid on a Treasury. “So, moving money from a Treasury to the CLF is the same thing. You’re still going to get paid Treasury yield,” Hauptman said. “The CLF is insurance that pays you, the complete opposite of most insurance.”

The CLF has approximately 450 natural-person credit union members and 11corporate credit union members, and represents about 10% of all total CU assets, the NCUA board was told. It has approximately $1.2 billion in subscribed stock.

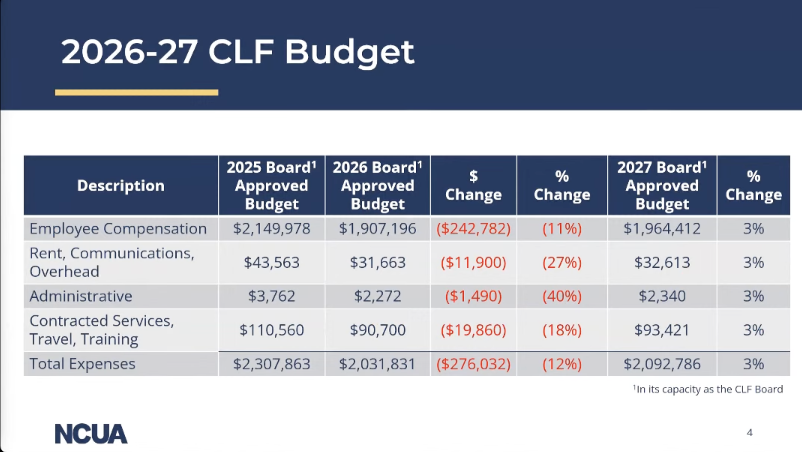

12% Reduction

The update to the board was provided by Matthew J. Biliouris, a long-time NCUA veteran who was recently named its acting director. Biliouris said the 2026 budget for the CLF reflects a 12% reduction from 2025, while the 2027 proposed budget calls for a 3% increase over 2026.

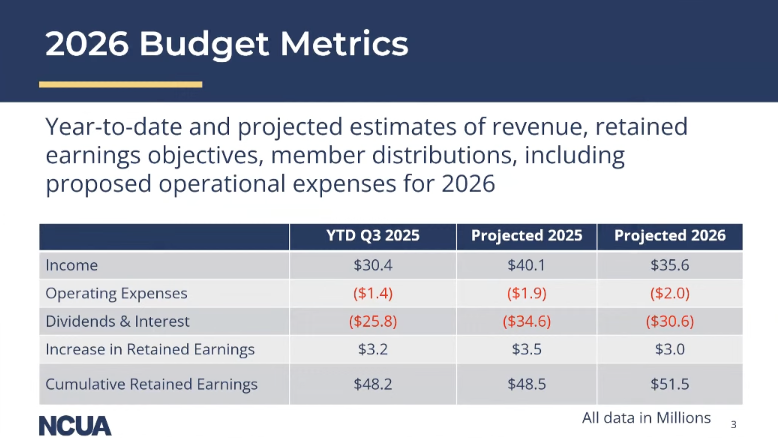

Biliouris said the fund’s $48.2-million in retained earnings have provided it with a base to cover operations. Remaining proceeds from investments are distributed as dividends to member CUs.

During 2026 the CLF plans to increase retained earnings by $3 million, Biliouris said.

CLF Performance

Additional financial performance can be seen above and below in the charts shared during the board meeting.

‘Admirably Lean’

Following Biliouris’ remarks, Hauptman called the 2026-27 proposed budgets “admirably lean,” which he said reflects a broader initiative at NCUA of lowering costs on credit unions.

“I’m supportive of the liquidity facility,” said Hauptman. “It’s vital, it’s growing, it’s well capitalized and it’s dependent on credit unions participating. Every member of the CLF strengthens it as it grows and provides more coverage.

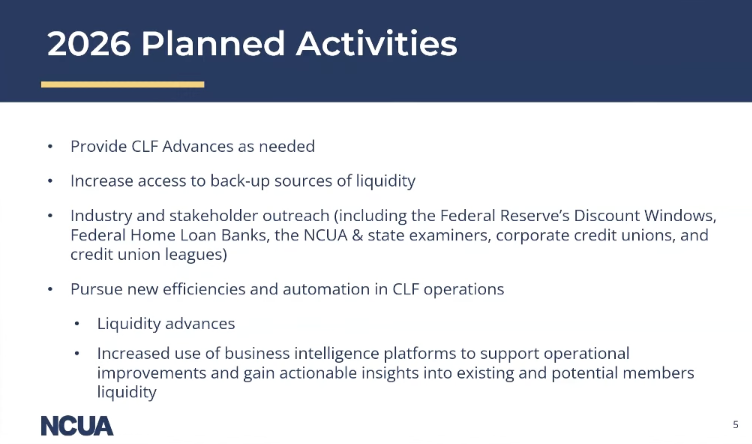

In response to a question from Hauptman, Biliouris said the CLF continues to pursue additional efficiencies, including making it easier to join and further automating the process.

Two Examples Shared

Asked by Hauptman for some examples of how the CLF has helped credit unions, Biliouris shared two:

- A credit union with between $10-$50 million in assets that had drawn down some of its credit line with its corporate credit union and which wanted to preserve the remaining line. That credit union received a 90-day advance that it repaid.

- A CU with between $100-$500 million in assets that needed a 30–day advance to deal with some mismatches related to maturing non-member deposits. Similarly, the CU also wanted to retain some of its corporate line access, so it turned to the CLF to resolve some short-term ALM challenges.

“We’re not telling credit unions you need to be part of the CLF, but you do need liquidity,” said Hauptman.