ALEXANDRIA, Va.–The NCUA board was given an update on the performance of the Central Liquidity Facility (CLF) through the second quarter.

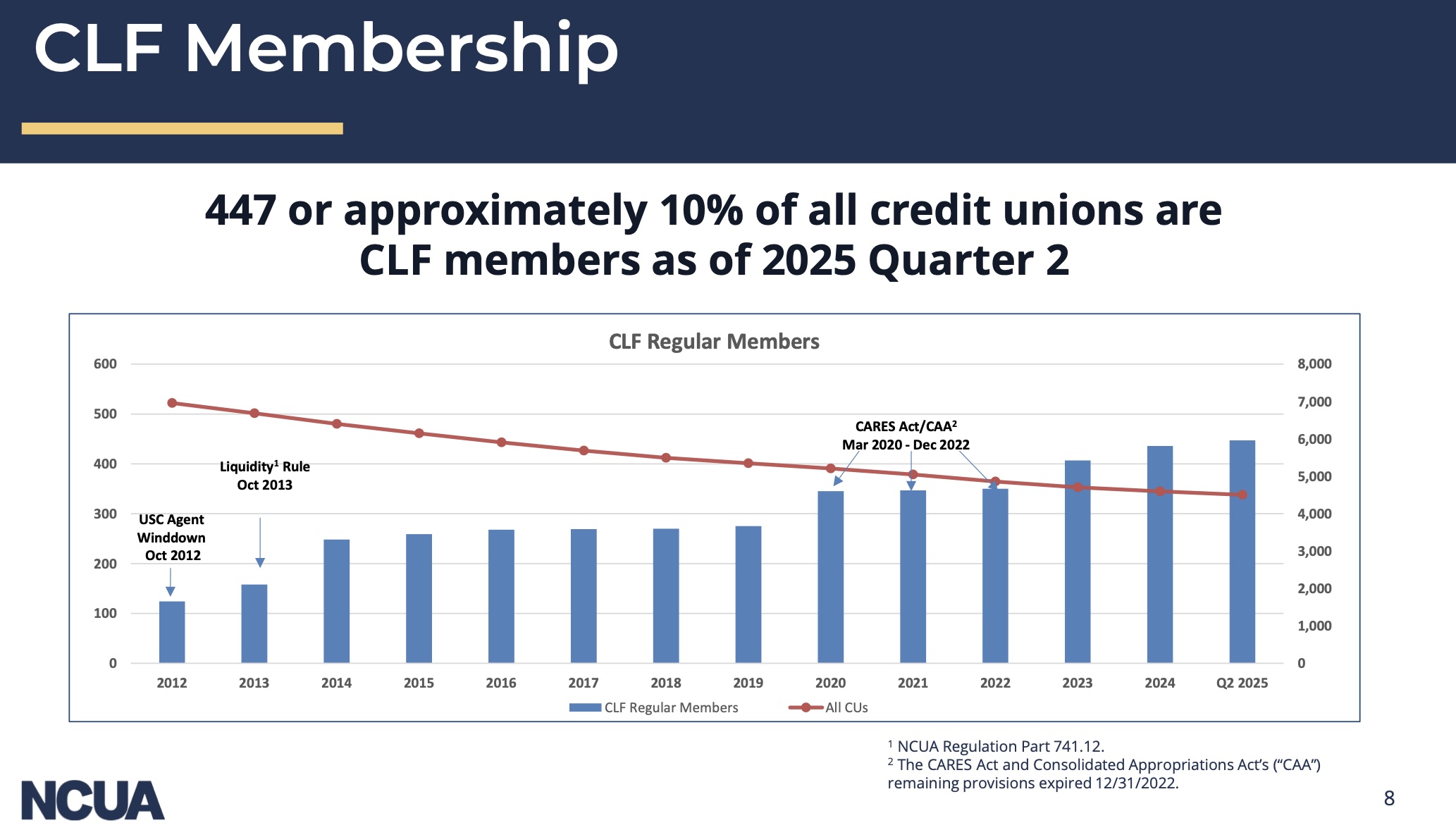

Anthony Cappetta, president of the Central Liquidity Facility, provided the update, and noted approximately 10% of credit unions are members of the CLF. As the name implies, the CLF is there to provide liquidity to credit unions and was originally created to be credit unions’ discount window for access to funds similar to what banks had, although credit unions now have access to funds from FHLBs and corporate CUs.

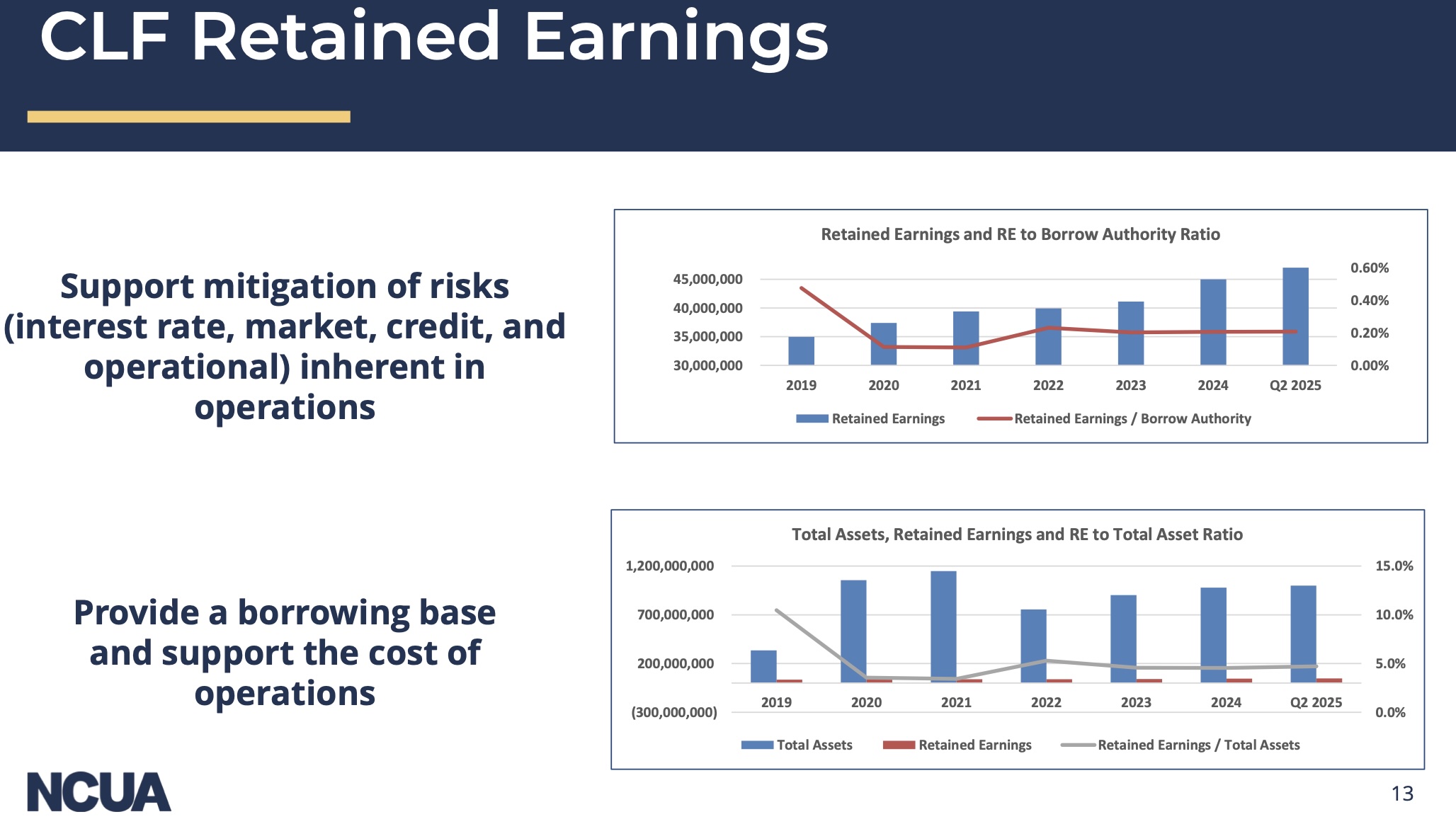

It has not been tapped to date in 2025, said Cappetta, noting it’s been a year in which there has not been much in interest rate fluctuations that might strain some CUs’ balance sheets. It did provide funds to several credit unions in 2024, he added.

In response to a question from Board Member Todd Harper, who was participating virtually, Cappetta said he expects the number of CLF members to grow to about 460 by year end.

When It’s Time to Go Looking

In addition, when asked by Harper why CLF membership is important, Cappetta responded by citing the old adage that “the time to go looking for liquidity is when you don’t need it.’ It’s just a wise planning in your liquidity management.

Here today you said we’ve not had a request in 2025 for a loan from the CLF and I will take that at face value but I also know that in recent years we have had requests for Cle loans is that not the case that is back in 2024 we did fund several loans for some members so the CLF is certainly that functionable and we has have deployed a loans to members as they’ve requested it and can you talk to me because

Chairman Kyle Hauptman agreed with some of the points made, and said while there has been some criticism posted online that the low usage of the CLF means it isn’t needed, that doesn’t mean it isn’t serving its purpose.

‘Apples to Oranges’

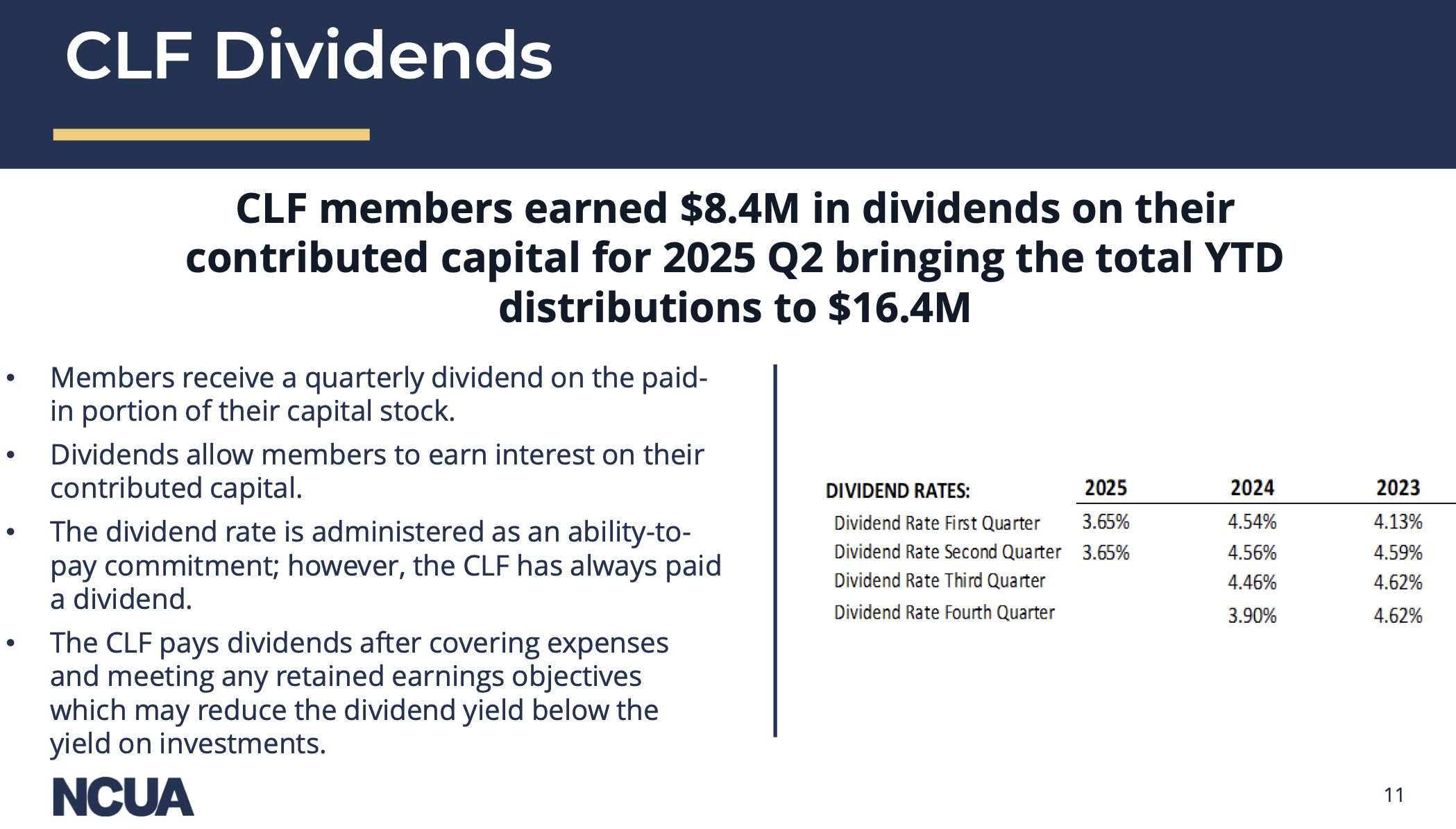

Cappetta said 70% of CFL members are also members of FHLB and 100% of CUs of more than $1 billion are members of the FHLB. Choose each for different reasons.

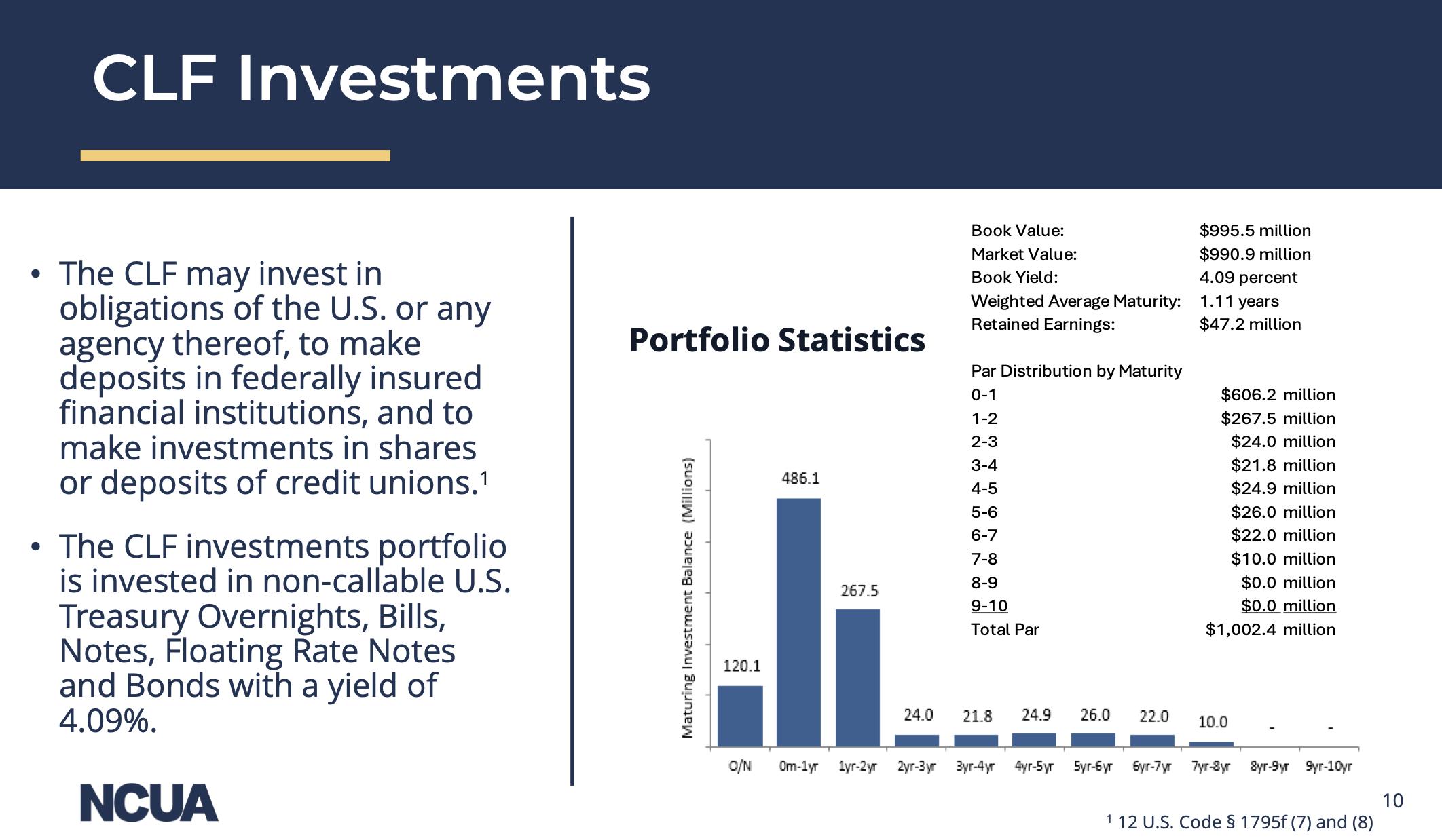

Cappetta noted, for example, that credit unions utilizing the Federal Home Loan Banks are required to have mortgage assets and can only borrow by pledging mortgage-related collateral. (It is the mortgage assets that explain why the FHLB dividend is higher than that paid by the CLF, it was noted.)

“Comparing the CLF and the FHLB is an apples to oranges comparison as the purpose and function of these two facilities is different,” said Cappetta, who called the CLF “liquidity insurance.”