BURBANK, Calif. — Fraud is increasingly becoming a direct driver of credit losses for lenders, with most financial institutions reporting rising losses tied to increasingly sophisticated schemes, according to a new report from Celent commissioned by Zest AI.

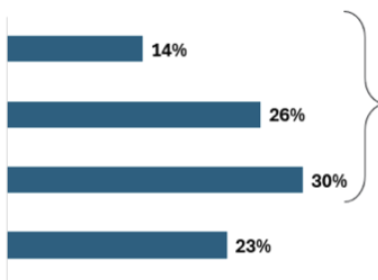

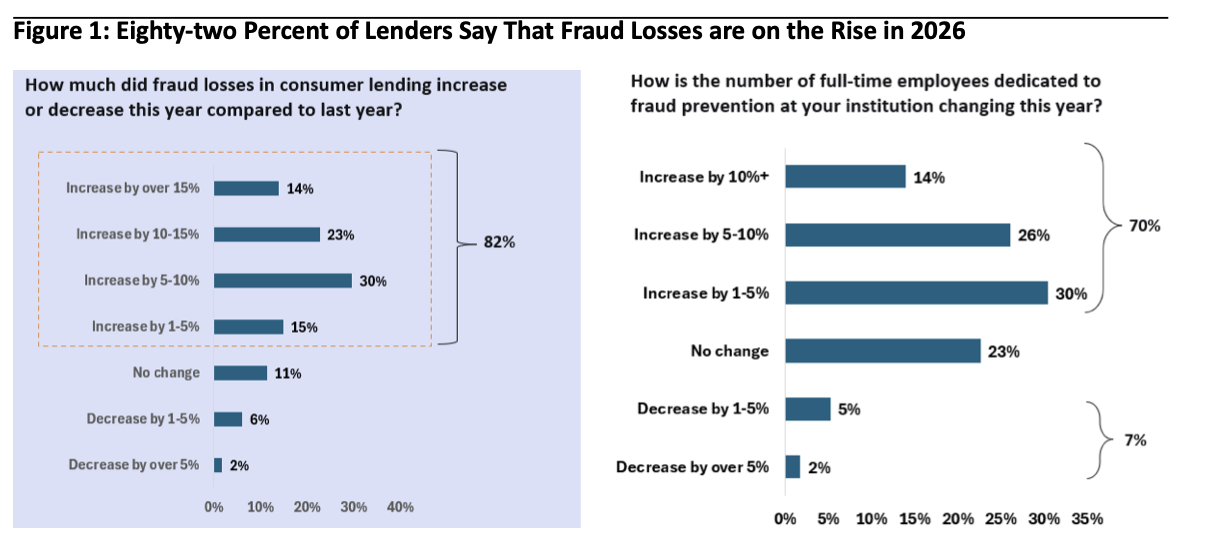

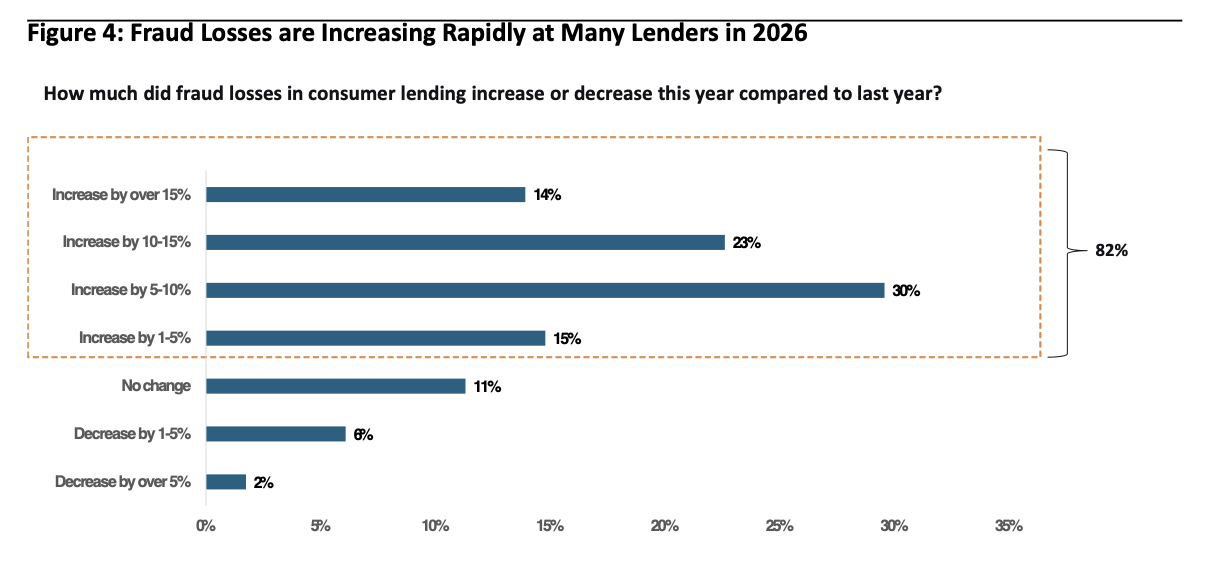

The report, based on a survey of 115 U.S. financial institutions, found that 93% of lenders said fraud contributes to their credit losses, while 82% reported fraud losses increased in 2026 compared with the prior year.

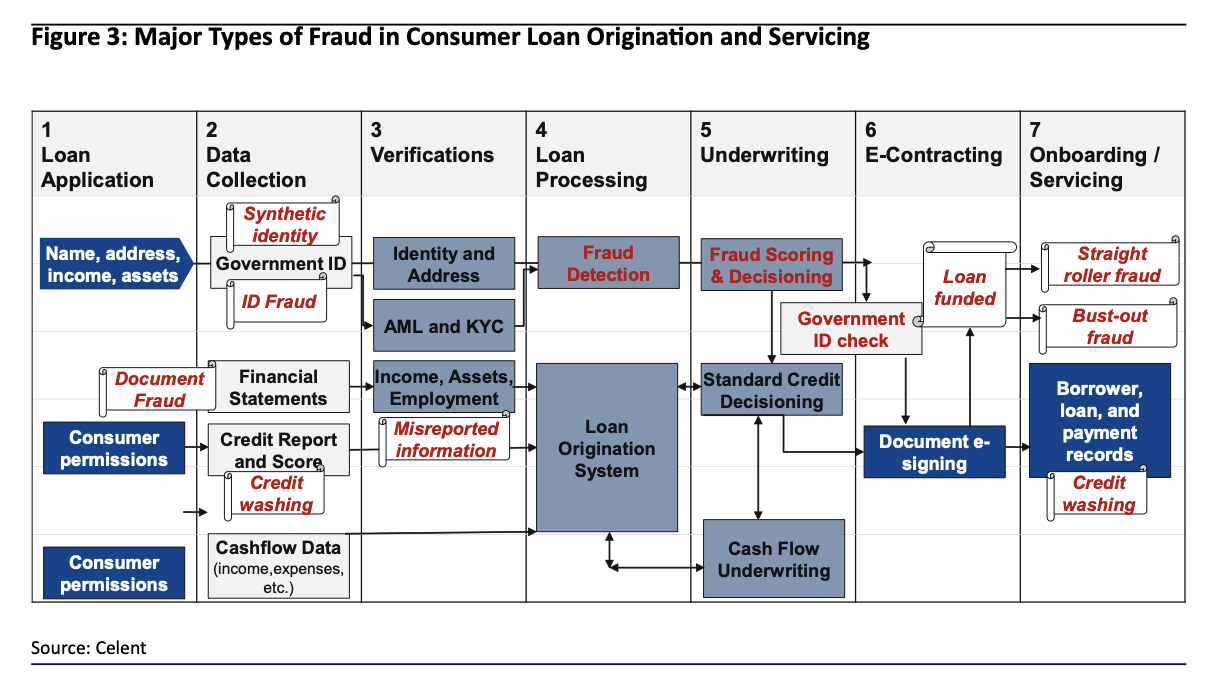

According to Celent, lenders are facing fraud schemes that often span multiple institutions, making them difficult for any single lender to detect on its own.

Sixty-one percent of lenders identified synthetic identity fraud as the fastest-growing type of fraud in 2026, followed by bust-out fraud at 56% and application stacking at 55%, the report said.

Synthetic identity fraud involves the creation of fake identities using a mix of real and fabricated information. Bust-out fraud occurs when borrowers establish good credit histories before maxing out credit lines and disappearing, while application stacking involves borrowers applying for loans simultaneously across multiple lenders.

Evolution in Fraud

“Fraud has evolved from a contained risk into a systemic threat that is cutting directly into lender profitability,” Craig Focardi said in the report.

“What makes this moment different is the nature of the fraud types that are driving losses,” Focardi added. “Synthetic identities, bust-out fraud, and application stacking are not opportunistic acts. They are organized, cross-institutional attacks, and no single lender has the full picture on their own.”

The report said many lenders are increasing investments to address the issue, though adoption of newer fraud detection technologies remains limited.

The Findings

Among the findings:

- 75% of lenders said they are increasing fraud technology spending this year.

- 70% said they are adding staff dedicated to combating fraud.

- Fewer than one-third currently use artificial intelligence or machine learning fraud models, alternative data signals or consortium-based intelligence-sharing tools.

The report also found broad support for fraud data-sharing consortiums, although participation remains relatively low.

According to the survey:

- 73% of lenders said fraud data-sharing consortiums benefit the industry overall.

- Only 34% currently participate in such consortiums.

- Another 46% said they would participate if the right consortium existed.

Additional Findings

Of that group, 25% said they would join a cross-lender fraud signal consortium immediately, while 21% said they are still evaluating the benefits of fraud data sharing.

In addition, 64% of lenders said their existing fraud technology systems are not keeping pace with evolving fraud methods, according to the report.

“These findings reflect a broader industry reality: the cost of fighting fraud is rising, and many institutions are struggling to keep pace with increasingly sophisticated attacks,” Mike de Vere said in a statement included in the report.

De Vere said fraudsters are operating across institutions while many lenders continue to fight fraud only within their own portfolios.

Broader Intelligence Sharing Recommended

The report said lenders may need broader intelligence-sharing capabilities and more advanced AI-based fraud detection tools to better identify cross-institutional fraud activity before losses occur.

According to Zest AI, its fraud detection platform is designed to identify first-party and behavioral fraud while maintaining automated loan decisioning processes for most applications.

Celent’s full report is titled “Combatting the Rise in Lending Fraud with AI and Data Sharing.”