RICHMOND, Va. — Community development financial institution (CDFI) credit unions are experiencing rising demand for services, but their challenges and ability to meet that demand vary significantly depending on their size, designation and service area, according to an analysis by the Federal Reserve Bank of Richmond.

The analysis, based on responses from 162 CDFI credit unions participating in the Federal Reserve’s 2025 CDFI Survey, found that while many institutions are seeing increased demand for financial products and services, some segments of the industry face greater capacity constraints than others.

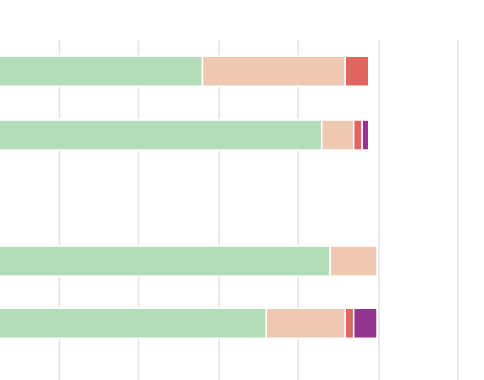

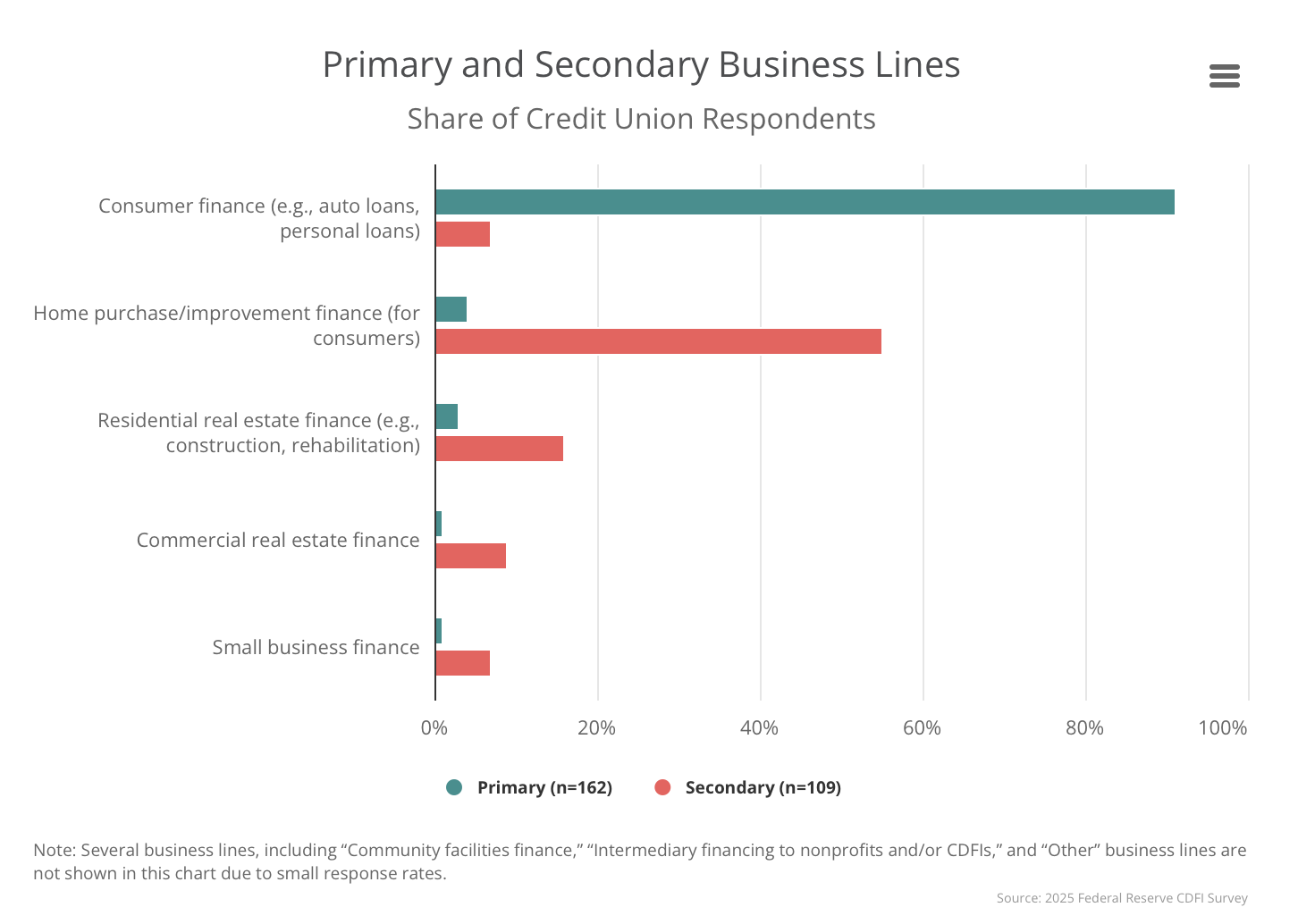

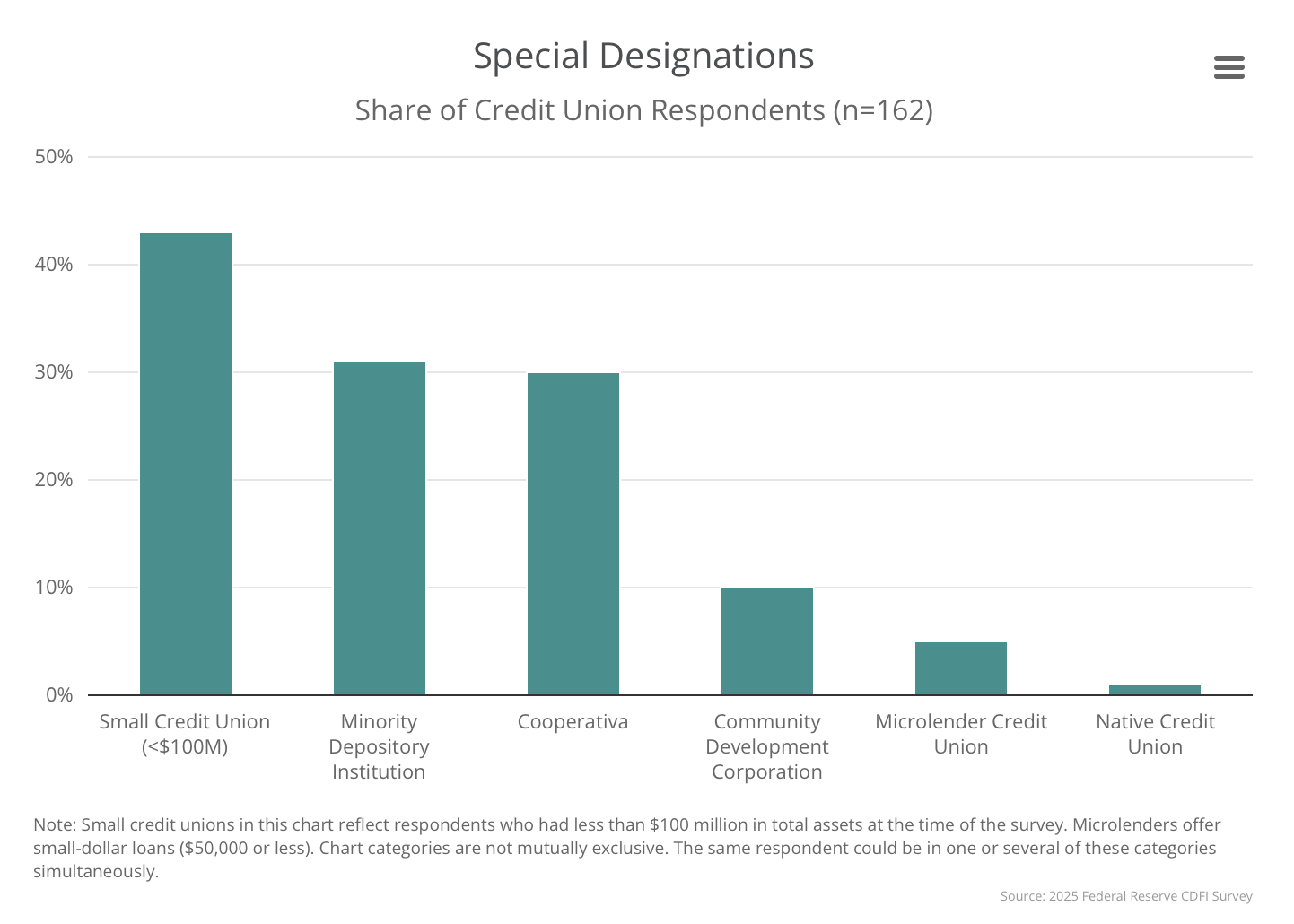

According to the Richmond Fed, 91% of responding credit unions said consumer financial products are their primary line of business, reflecting the traditional credit union model. Approximately one-third reported having no secondary business line. The survey also found that 31% of respondents were designated as minority depository institutions (MDIs), while roughly 30% were cooperativas, the cooperative credit unions based in Puerto Rico.

The Richmond Fed said responses from these institutions highlighted the differing opportunities and challenges facing credit unions serving distinct membership groups and communities.

Technology Emerges as Common Challenge

One finding that cut across institution types was the impact of technology-related challenges.

According to the Richmond Fed, 78% of credit union respondents said technology issues were limiting their ability to meet growing demand. Among those institutions, 80% cited the high cost of client-facing technology as a significant obstacle, while 71% said integrating new technology with existing systems created operational difficulties.

Security concerns also were frequently cited. Approximately 60% of respondents said cybersecurity and related security challenges were hindering their ability to serve additional members and customers. The Richmond Fed noted that fraud and scam activity has increased across the financial services sector, raising costs and operational risks for institutions.

Capacity Constraints Differ by Institution Type

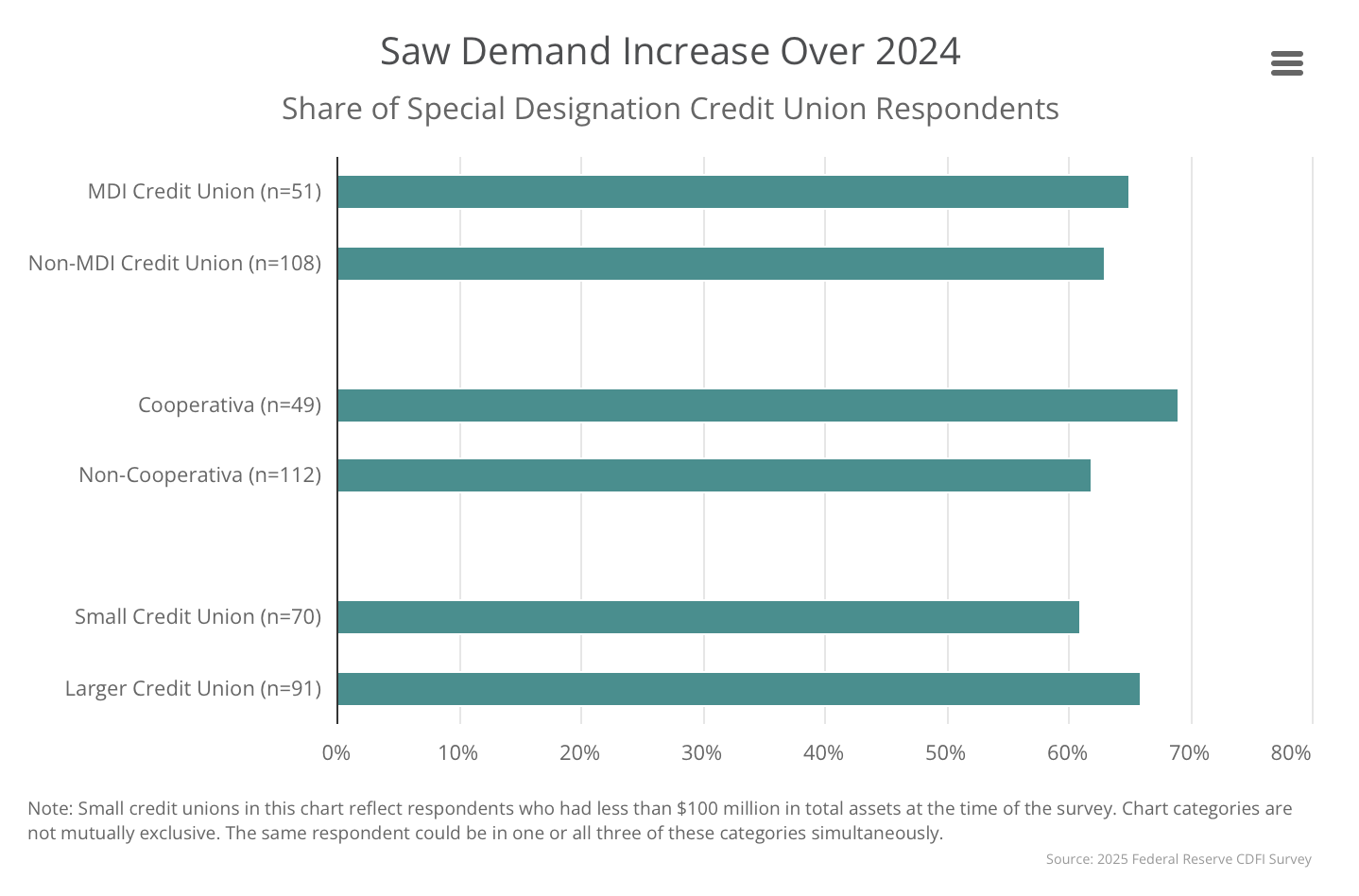

While technology challenges were nearly universal, the Richmond Fed found that capacity constraints varied across institution types.

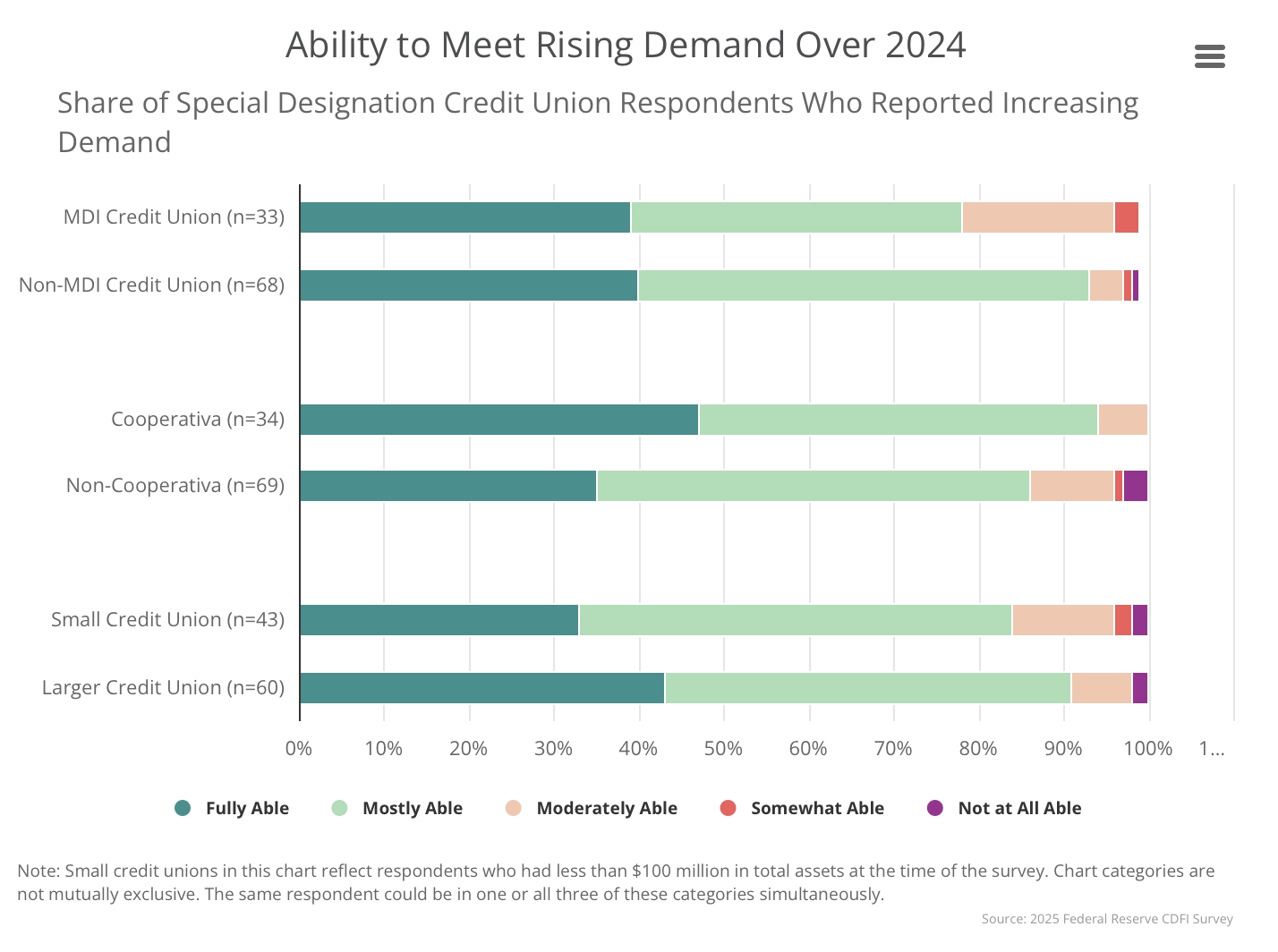

A Federal Reserve analysis of survey responses found that minority depository institution credit unions and smaller credit unions were more likely to report difficulties keeping pace with growing demand. According to the analysis, 18% of MDI respondents reported challenges meeting increased demand, compared with 4% of non-MDI credit unions.

The Richmond Fed said these differences reflect the varying resources, staffing levels and operational capacities available to different types of institutions.

Partnerships Help Address Challenges

The Richmond Fed’s analysis also highlighted the role of community partnerships in helping credit unions overcome operational barriers and expand access to financial services.

Survey respondents reported working with other financial institutions, municipalities, nonprofit organizations and philanthropic groups to strengthen their ability to serve members. Several smaller credit unions cited mission-aligned deposits from philanthropic organizations as an important source of funding that could be redeployed into affordable lending for underserved borrowers.

Other respondents described partnerships that support financial education programs and outreach efforts designed to serve low-income households, younger consumers and members using Individual Taxpayer Identification Numbers. These collaborations helped institutions identify gaps in financial knowledge and develop services tailored to community needs, according to the Richmond Fed.

Looking Ahead

The Richmond Fed concluded that although most CDFI credit unions have experienced increasing demand in recent years, the ability to respond to that demand differs substantially across the sector.

The analysis said community partnerships can help credit unions address technology, staffing and operational challenges while expanding access to financial services. The Richmond Fed also suggested that collaboration among credit unions—including sharing expertise, back-office services and operational resources—could help smaller institutions improve efficiency and better serve their communities.

About the Survey

The Federal Reserve’s CDFI Survey is conducted every two years and gathers information from mission-driven lenders across the country, including banks, credit unions, loan funds and venture capital funds that focus on expanding financial access in underserved communities.