WASHINGTON— U.S. households are leaning more heavily on credit cards for day-to-day liquidity, pushing revolving credit to grow faster than longer-term borrowing even as overall consumer credit growth slowed in October, according to new data released by the Federal Reserve.

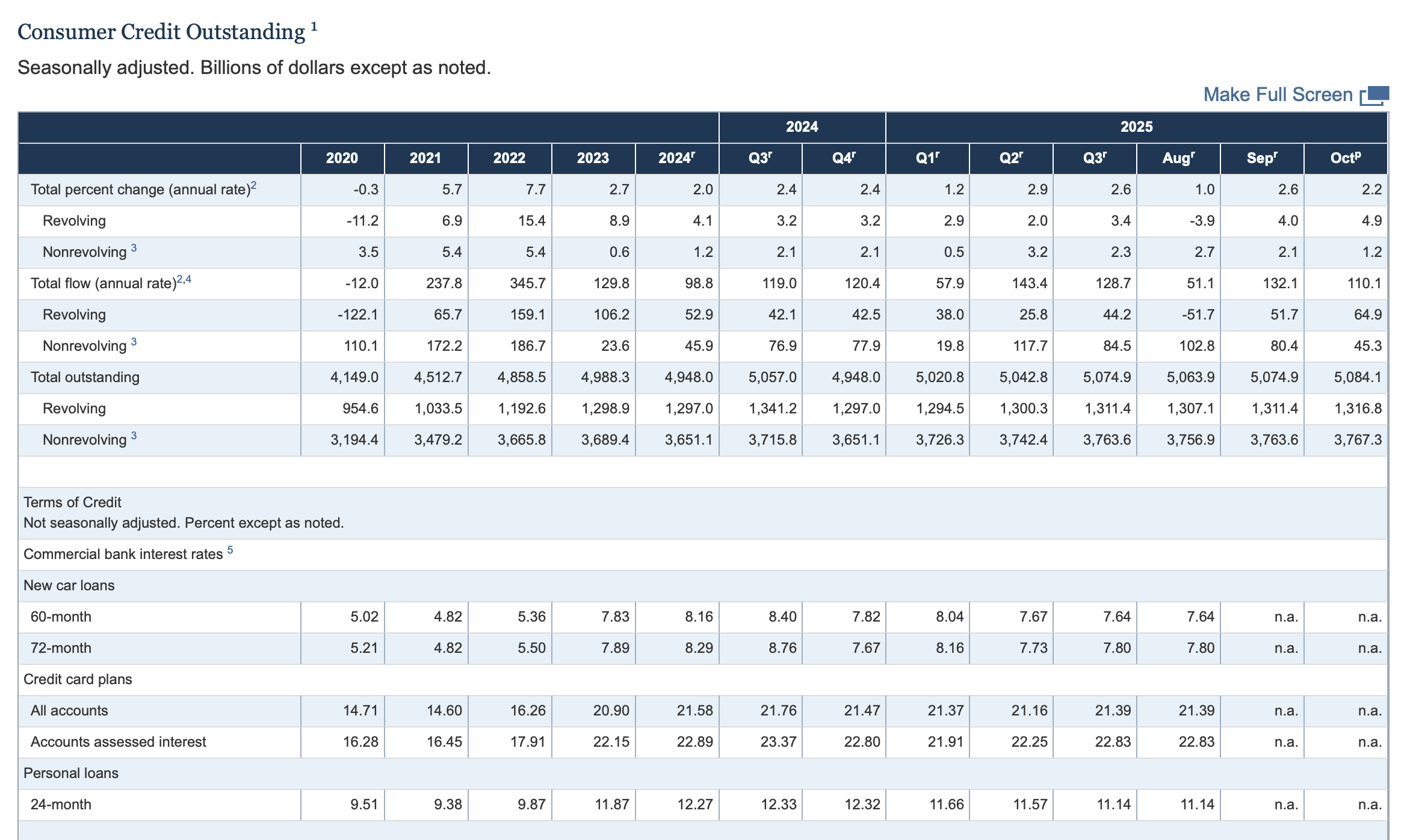

Total consumer credit rose at a seasonally adjusted annual rate of 2.2% in October, down from 2.6% in September. Beneath that headline figure, however, borrowing patterns shifted as revolving credit accelerated while nonrevolving debt cooled, the Fed data indicate.

Revolving credit balances climbed to $1.3 trillion in October and expanded at a 4.9% annual rate, up from 4% the prior month, the Fed reported. Revolving credit includes credit cards and other short-term borrowing tied to household cash flow, discretionary spending and liquidity needs.

By contrast, nonrevolving credit — which largely reflects auto loans and other installment products — slowed to a 1.2% annual rate, down from 2.1% in September, the Fed data show. The divergence suggests households are exercising caution on large, long-term financed purchases while relying more on readily available credit as the holiday season approaches, according to analysts.

Leap in Card Rates

The Fed said rates charged on credit cards stood at more than 21.3%, up sharply from about 14.7% roughly five years ago, underscoring the higher cost of carrying revolving balances.

Younger and lower-income households continue to rely on revolving credit not only for spending but also as a way to manage cash flow and build credit histories, the data show. Despite the elevated rates, depository institutions remain the primary drivers of credit expansion, while lending activity by finance companies has softened, particularly for installment products.

The Fed data point to a consumer credit environment defined less by broad-based growth and more by shifting preferences, as households navigate higher borrowing costs and increased reliance on short-term credit to manage everyday expenses.

For the full data, go here.