Has Charts

ST. PETERSBURG, Fla.–A new analysis of members spending and consumer card activity shows consumers began 2025 with strong levels of purchasing activity, despite a drop in confidence and higher-than-forecasted inflation, according to the February edition of the Velera Payments Index.

The Index reveals debit purchases posted the best monthly year-over-year growth since February 2022, while credit remained strong, according to Velera, which also conducted a Deep Dive into Buy Now, Pay Later (BNPL) consumer activity and the continued rise in popularity of the offering.

Key Takeaways

Velera reported its found:

- For the first month of 2025, year-over-year growth rates improved for debit and held steady for credit. Debit purchases were up 7.8% and credit purchases were up 2.5% in January. Debit transactions were up 4.8% and credit transactions were up 2.8%.

- For debit, Money Services returned as the top contributor to growth in purchases, accounting for one-third of the year-over-year increase. The Goods and Services sectors had the second largest impact for debit and the largest year-over-year increase in credit purchases.

- The 12-month CPI through January increased by 3.0%, up 0.5% from December. The Shelter index increased 0.4% and accounted for 30% of the overall increase. Core inflation, now at 3.3%, was up 0.4% for January, the largest increase in two years.

The next opportunity for an interest rate change by the Federal Reserve is on March 19.

Buy Now, Grow Now

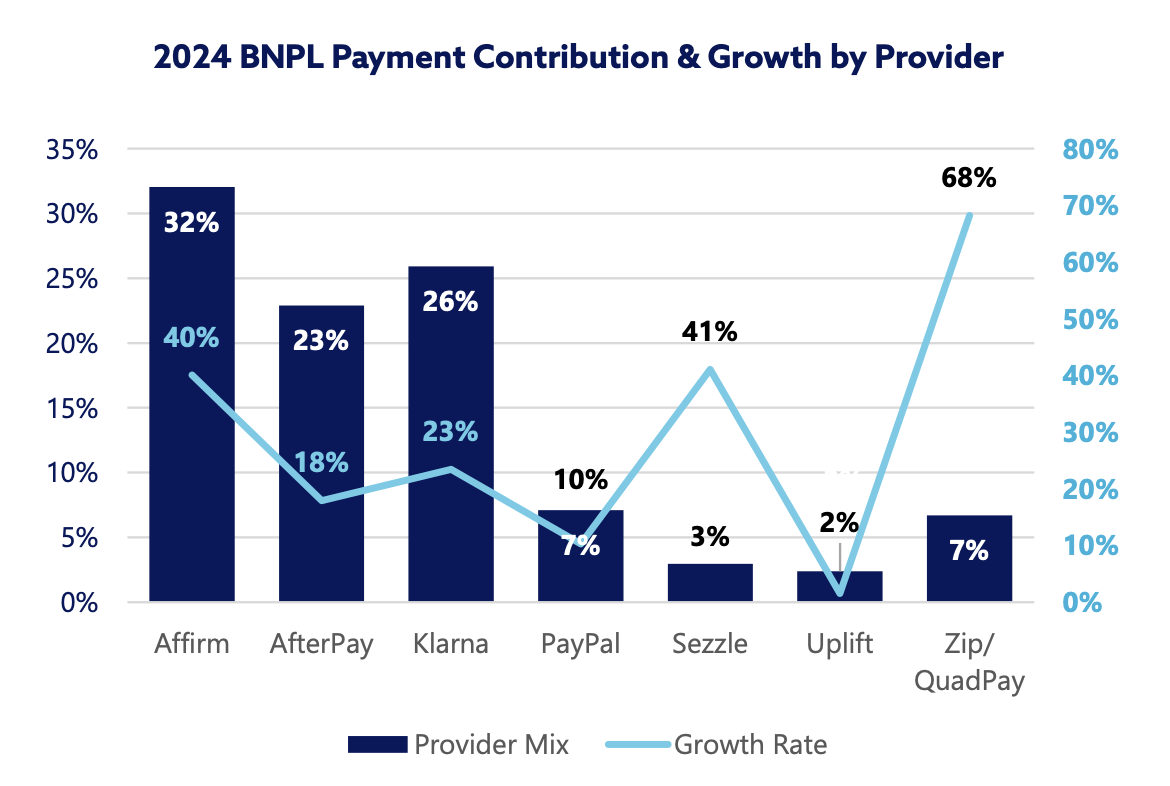

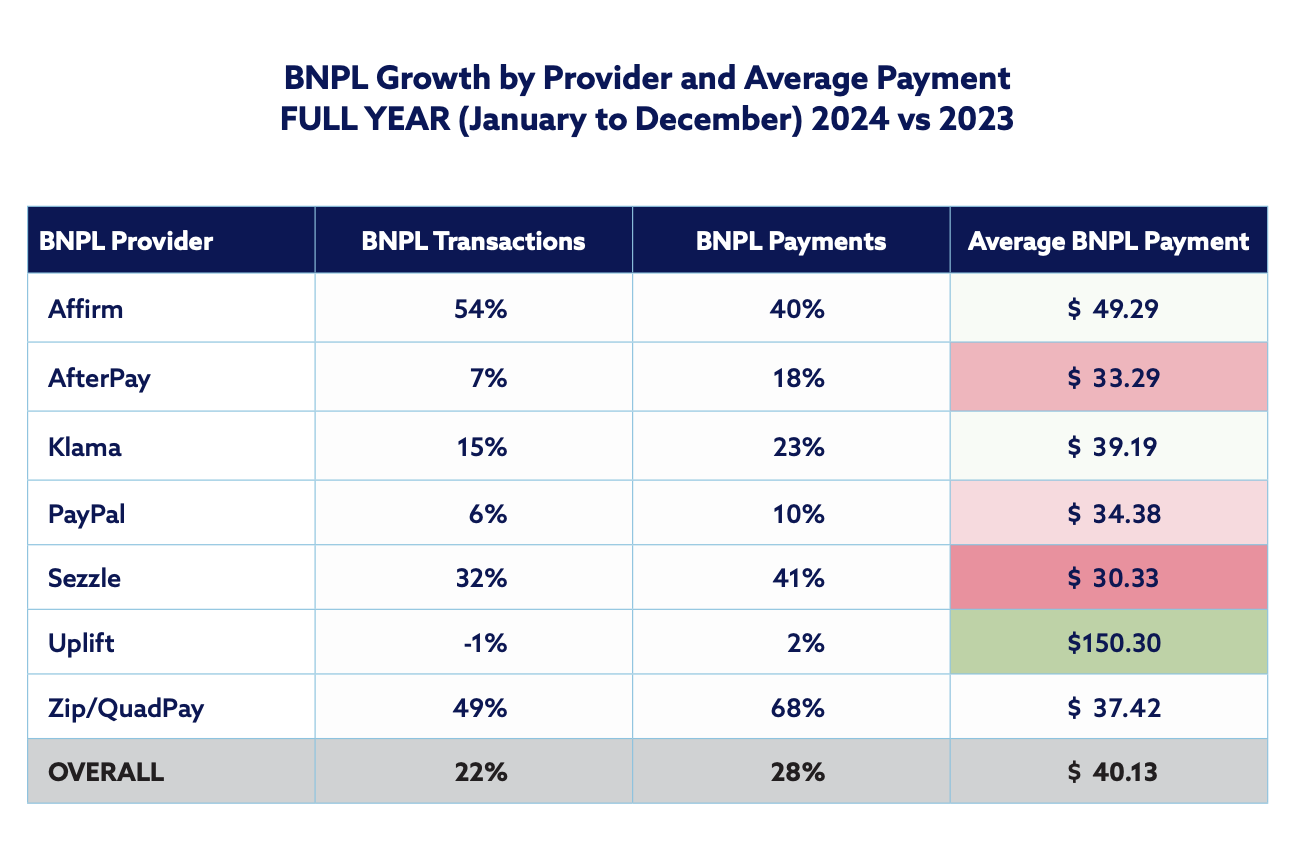

Meanwhile, Velera reported that growth in BNPL payments and transactions facilitated by cards increased 28% and 22%, respectively, for the top BNPL merchants for full-year 2024 compared to 2023.

The rise of Buy Now, Pay Later (BNPL) highlights the increasing demand for convenience and flexibility, especially among younger consumers,” said Cody Banks, senior vice president, product experience & enablement, in a statement. “While BNPL offers ease, it also brings considerable risks to consumers, such as potential overspending and debt accumulation. BNPL also poses a significant threat to traditional credit cards, challenging credit unions to reinforce benefits like rewards and credit score building that BNPL lacks. Credit unions should take the lead in educating members on the variety of payment methods available, empowering them to make informed choices and enhance their financial well-being.”

What to Do Now?

What should credit unions do now?

According to Velera’s analysis, credit unions should keep a pulse on member usage of alternative payments, including BNPL.

“To offset the impacts of BNPL, credit unions should constantly communicate the value of their card offerings, including zero liability, rewards and convenience,” the company said. “Additionally, credit unions should optimize card integration into digital banking, leverage the usage of mobile wallets and consider the addition of post-purchase installment options on their credit card products.”

According to Velera’s Advisors Plus Payments & Deposits Consulting, credit unions that don’t focus on this area in 2025 should expect volume growth to be nominally lower or even decline.

Credit unions should strengthen their portfolios by offering competitive rewards products that drive member engagement and enhance loyalty. Positioning rewards programs as valuable financial tools will allow credit unions to deepen member relationships, increase transaction volumes and boost fee income.

The full report is available for download here.