DALLAS — Rising homeowners insurance premiums are increasing financial strain on U.S. households and could contribute to higher mortgage delinquencies and broader financial system risks, according to new research from the Federal Reserve Bank of Dallas.

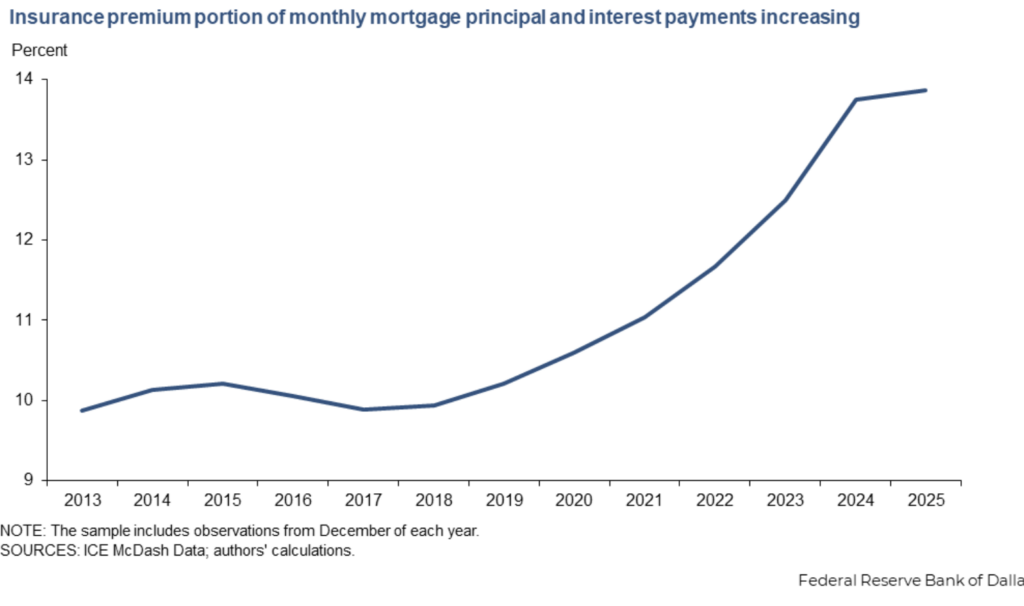

In a new report, researchers Shan Ge and Nitzan Tzur-Ilan said insurance costs have climbed sharply in recent years, rising about 70% nationally between 2019 and 2025. As a result, insurance now accounts for a growing share of monthly housing payments, reaching 14% of the typical mortgage payment in 2025, up from 10% in 2013, according to the Dallas Fed analysis,

The report found that homeowners facing rising premiums have limited options, particularly those with lower incomes. While some households respond by switching insurers or relocating to areas with lower costs, others increasingly rely on credit cards, delay mortgage payments or face the risk of losing their homes .

Using mortgage-level data, the researchers said higher premiums are linked to both increased mobility and financial distress. A $1,000 increase in annual insurance premiums was associated with a 0.54-percentage-point rise in the likelihood of relocating, as households seek lower-cost areas . At the same time, premium increases pushed an estimated 31,000 mortgages into delinquency in 2022, the report said .

The Look Forward

Looking ahead, continued increases in premiums could result in an additional 203,000 mortgages becoming delinquent annually between 2025 and 2055, based on projections cited in the report .

The effects are not evenly distributed. Financially constrained households are more likely to fall behind on mortgage payments, while higher-income households are more likely to relocate or find alternative insurance coverage, according to the researchers .

The report also found that rising insurance costs are driving greater credit card use, signaling that some households are turning to revolving debt to manage housing-related expenses .

‘Broader Economic Concern’

Ge and Tzur-Ilan said the findings point to a broader economic concern, as rising delinquencies could lead to increased losses for lenders and entities that back or insure mortgages. The trend may also contribute to long-term shifts in where people live, with higher-risk, higher-cost areas increasingly concentrated among lower-income households.

The researchers said the findings highlight insurance affordability as a growing policy issue, noting that rising premiums are emerging as a key driver of financial stress and potential instability in housing markets.