By Susan Mitchell

At our company we have been looking closely at organizational development across the credit union industry, not as an academic exercise but through the lens of what it will take to lead in an AI‑enabled future. If we are serious about using AI to elevate the member experience, then we must be equally serious about building the internal infrastructure that supports it.

Otherwise, we are simply bolting new tools onto old structures and allowing vendors to define our trajectory for us.

I recently completed an organizational chart analysis across 10 credit unions ranging from $1-$10 billion in assets. The results were almost unsettling in their uniformity. Different titles here and there, a few added roles based on field of membership or growth, but structurally they were nearly identical. My findings were “non‑findings,” which forced a different question: What happens when you apply legacy organizational knowledge to a 2026 operating environment?

The answer was sobering. When I reached out to trusted advisors, one message cut through everything else: we are not ready. One leader even told me, “I’m retiring because driving this tsunami of change requires fresh eyes, persistence of mission, and an extraordinary real‑time focus.”

Who but an extraordinary leader says that out loud?

Getting Deeper

That level of candor pushed us deeper into the work. We began examining job descriptions, organizational positioning, and the real ROI behind modernizing key roles. When we looked closely at the finance function, especially the VP of Finance or Controller depending on size, the gap between legacy expectations and 2026 realities became impossible to ignore. What credit unions need from this role today is fundamentally different from what most job descriptions still describe.

In fact, it is elevated to what most consider the CFO position, which causes a hmm…

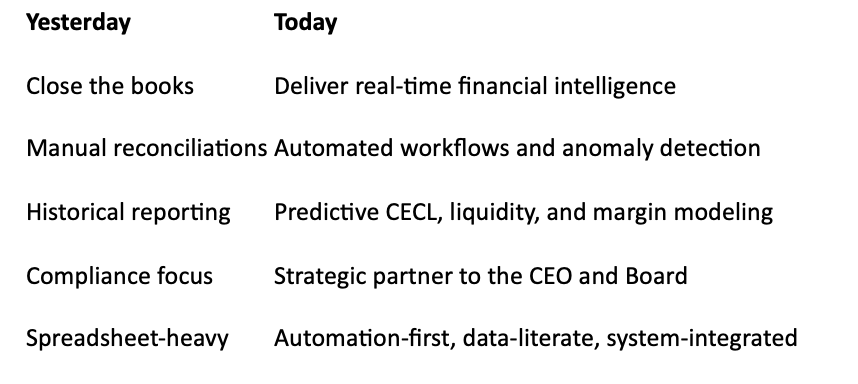

Across the industry, we are all dealing with the same realities: margin pressure, unpredictable liquidity, CECL swings that can reshape a quarter, and a pace of decision‑making that does not wait for the month‑end packet. The traditional Controller role has not kept pace with the complexity. The work has changed, and the expectations have changed with it. This is not about adding more tasks to an already full plate. It is about redefining the role, so the credit union has business intelligence, automation, and foresight it needs to operate with confidence.

What’s Changing and Why It Matters

The Controller used to be the quiet stabilizer in the background. Today, the role sits much closer to the center of strategic decision‑making. The organization needs more than historical reporting; it needs real‑time intelligence, predictive modeling, and a finance function that can keep up with the speed of the business. The Controller still owns accuracy and compliance, but now must also bring insight, automation, and strategic clarity.

What ROI Looks Like for a Billion+ Credit Union

Although most say that ROI is hard to state up front, the realities of current practices give us an idea of what to expect in the future because the value of automation comes from multiple operational improvements happening at once: time saved, errors reduced, volatility minimized, and decisions made earlier with better information. When these efficiencies compound across a year, the fiscal impact becomes both visible and defensible.

Closing time reduction is one of the most immediate gains. Many credit unions still close in eight to 12 days. When automation takes over reconciliations, journal entry workflows, and exception handling, the close reliably drops to four to six days. This shift frees up meaningful staff time, reduces audit pressure, and gives leadership a clearer, earlier, view of the month. The value is both operational and strategic. Decisions get made with fresher data and fewer surprises.

Automated reconciliations deliver another significant return. A billion+ credit union typically manages 150 to 300 reconciliations a month. Automation manages the bulk of them and flags exceptions. The ROI is straightforward: fewer manual hours, fewer errors, and a more stable control environment. It also reduces key‑person risk, which is becoming a real issue as finance teams stretch thin.

CECL: A Meaningful Lever

CECL stability is one of the most meaningful financial levers available. CECL volatility can swing hundreds of thousands of dollars in a single quarter. When the Controller leads a more sophisticated modeling and validation process, supported by better data and predictive tools, the allowance becomes more stable and more accurate. Even a five to ten basis point improvement in over‑provisioning translates into $300,000 to $600,000 in capital impact for a billion+ M institution.

Liquidity forecasting has become essential. Better modeling reduces reliance on overnight borrowing, improves investment timing, and helps ALCO make decisions with confidence. The ROI shows up in avoided interest expense, better laddering, and fewer reactive moves. This easily reaches six figures annually.

Improving Margin

Margin improvement is another consistent outcome. When the Controller brings stronger analytics into pricing, forecasting, and ALCO strategy, the credit union typically sees a three to five basis point improvement in margin. On the balance sheet this is $225,000 to $375,000 a year. It is not theoretical. It is simply better information, delivered faster, and used consistently.

Strategic acceleration is the quiet value driver. When the Controller provides real‑time dashboards, scenario modeling, and clear narratives, the entire organization moves faster. Leadership spends less time waiting for data and more time acting on it. The ROI is harder to quantify, but it is felt everywhere: fewer surprises, better alignment, and a leadership team that can see around corners instead of reacting to what already happened.

The ROI Framed for Leaders

The most credible way to frame the return is simple and grounded. For every one dollar invested in modernizing the Controller role, credit unions have the potential to generate $6-12 in measurable value. That range reflects operational improvements, risk reduction, margin lift, and faster decision‑making. It is based on real work happening inside credit unions today, not hypothetical models or inflated assumptions.

Summary

The Controller role is no longer a back‑office necessity. It is a strategic position that shapes how the credit union navigates risk, margin, liquidity, and growth. As the industry leans into AI and real‑time intelligence, the organizations that will thrive are the ones willing to rethink their structures, upskill their teams, and modernize the roles that sit at the center of financial decision‑making.

This is not about adding complexity. It is about creating clarity. And for credit unions ready to lead, the return is not only measurable, but also transformative.

Susan Mitchell is a strategist and industry consultant with 30 years of experience advising credit union boards and executives. As Founder and CEO of Mitchell Stankovic & Associates, she drives bold thinking on governance, culture, and the future of cooperative leadership. Her work challenges complacency and pushes the industry toward relevance, resilience, and meaningful community impact. Connect at mitchellstankovic.com.