WASHINGTON–Credit unions seeking to grow and perform better often share some common mistakes when attempting to accomplish both, while their boards just as often never ask a common but necessary question, especially when they are considering mergers, according to one company.

Those issues and a host of others around CU growth, performance, charters, SEGs, FOM expansion, why some branches significantly outperform others and more are examined in this CU Daily Q&A with Sam Brownell, CEO and founder of CU Collaborate. The comments are part of the CU Daily’s 2026 series, “The Profitability Imperative.”

Here are some of the insights, advice, and strategies he had to share.

The CU Daily: First, provide some background on CUCollaborate and what it does and how it came to be?

Brownell: I founded CUCollaborate in 2014, but the idea had been percolating for a while. I spent close to a decade at Callahan & Associates before that, and I kept seeing the same pattern. Credit unions offer better pricing and services than banks, especially for lower-income Americans, yet most consumers either didn’t know credit unions existed or didn’t know they were eligible to join one. That’s a marketing problem, a regulatory problem, and a data problem all at once.

We started as a consulting shop focused on field of membership work, because field of membership was the most obvious growth bottleneck for federally chartered credit unions. From there we built software to make the regulatory work faster and more less burdensome. Then we added a marketing arm, because expanded eligibility doesn’t mean much if no one in your new addressable market has heard of you.

Today we describe ourselves as a data and analytics CUSO, but the through-line hasn’t changed. We exist to help credit unions grow, perform better, and improve their impact. I still believe every American should be a member of a credit union, and most of the work we do is in service of closing the gap between that belief and the reality.

The CU Daily: When a credit union approaches you, are they seeking guidance on something in particular, and has that changed or evolved?

Brownell: When I started the firm, almost every conversation began with field of membership. A credit union would call us because it had hit a ceiling on its addressable market and needed to expand its charter. That’s still a big part of our practice. We have a 100% approval record on the FOM work we file with NCUA, and the expansions we close are roughly 321% larger than the industry average.

What’s changed is the breadth of the conversation. Credit unions now come to us for FOM, charter conversion, CDFI certification, low-income designation, branch strategy, member acquisition, mergers, and whole host of other things. Often, it’s several of those at once, because they’re all interconnected. A credit union that wants to grow deposits in a new community usually needs to think about FOM, branches, marketing, and possibly LID or CDFI in the same plan.

The other shift is toward analytics. Five years ago, we were mostly answering “can we?” Today we’re more often answering “should we, and what should we expect?”

The CU Daily: If a credit union broadly states that it “wants to grow,” what is your response? Do you differentiate between growth and performance?

Brownell: When a credit union tells me it wants to grow, my first question is what it means by growth and why. Asset growth, membership growth, loan growth, and deposit growth are all different things, and they don’t always move together. A credit union can grow assets quickly by raising deposit rates and still deliver less value to its members than a peer with flatter asset growth.

I do differentiate growth from performance, and I think the industry should, too. I wrote a piece a couple of years ago arguing that the metrics most credit unions track aren’t actually measures of success. Ten percent asset growth, 1% ROA, and over 8% net worth tell you the credit union is growing in their assets in a financially responsible way. They don’t tell you whether members are better off because of it.

Performance, in my view, is how much more money your members have in their pockets because of their relationship with you, multiplied by how many members you’re reaching. That’s what we mean by Member Benefit Impact. Growth without performance is just movement.

The CU Daily: CUCollaborate states that it uses data and analytics to drive insights: which data do you look to and what kinds of mistakes/misunderstandings, if any, do credit unions make in looking to the member information they already have?

Brownell: We pull from several buckets: regulatory data the NCUA publishes, deposit data from FDIC, demographic data from the Census and ACS, branch and ATM data, our own field of membership database, and where we have the relationship, the credit union’s core data. The point isn’t any one source. It’s the combination.

The most common mistake I see is credit unions treating their own member file as the whole picture. Your member data tells you who’s already with you. It doesn’t tell you who isn’t, and it definitely doesn’t tell you why. Without an external benchmark, it’s hard to know whether your member demographics reflect your community or just the corner of it you’ve historically reached. It’s also hard to know whether your products are pricing competitively against the banks down the street.

The second mistake is treating data as a reporting exercise rather than a decision-making one. Knowing your average member age went up two years isn’t useful unless it changes what you do next.

The CU Daily. Data is quantitative. Things like mission, values, and philosophy are qualitative. Both have value—how can a credit union bridge the two?

Brownell: Mission is the why. Data is the proof. Credit unions tend to be very good at the first and inconsistent at the second, and the result is that policymakers, regulators, and consumers can’t always see the difference between credit unions and banks.

The bridge is impact reporting. We worked with American United Federal Credit Union to quantify member benefit, and the answer came out to about $450 per member, per year in savings versus what those members would have paid at a comparable bank. That’s a mission statement with a dollar sign attached. It resonates with members, with employer partners considering a SEG relationship, and with legislators evaluating the credit union tax exemption.

You don’t lose the qualitative by quantifying it. You actually protect it. When the mission can be measured, it’s much harder to argue the mission isn’t real.

The CU Daily: CUCollaborate offers consulting across a number of areas/disciplines. Where are you seeing the most interest and why?

Brownell: Field of membership and charter work is still the largest single line of our consulting business. We just closed an expansion for JetStream Federal Credit Union into Broward County, which brings their eligible market to roughly 4.7 million across South Florida.

Beyond FOM, we’re seeing real momentum in three areas. First, data driven branch strategy. Credit unions often need to consider their service network strategy as part of field of membership expansion projects. After several years of consolidation, credit unions are asking sharper questions about where they should be physically present, and they want analytics behind the answer instead of intuition. Our Branch Market Analysis work sits in that lane, and it’s been some of our fastest-growing consulting.

Second, helping credit unions maximize the value they get from what we call beneficial regulatory programs (CDFI, LID, ECIP, etc.). CDFI certification and grant work has accelerated meaningfully. We’ve helped credit unions secure more than $27 million in CDFI grants with roughly a 65%-win rate, and as the funding environment shifts, more credit unions are taking certification seriously. Low-income designation is in a similar place, with 30 designations since 2020 and a 100% success rate.

Third, mergers. Merger activity has picked up across the industry, and the conversations we’re having are different than they were a few years ago. Boards are asking harder questions about whether a proposed combination actually serves members or just gets the deal done, and regulators are scrutinizing member benefit more closely as part of approval.

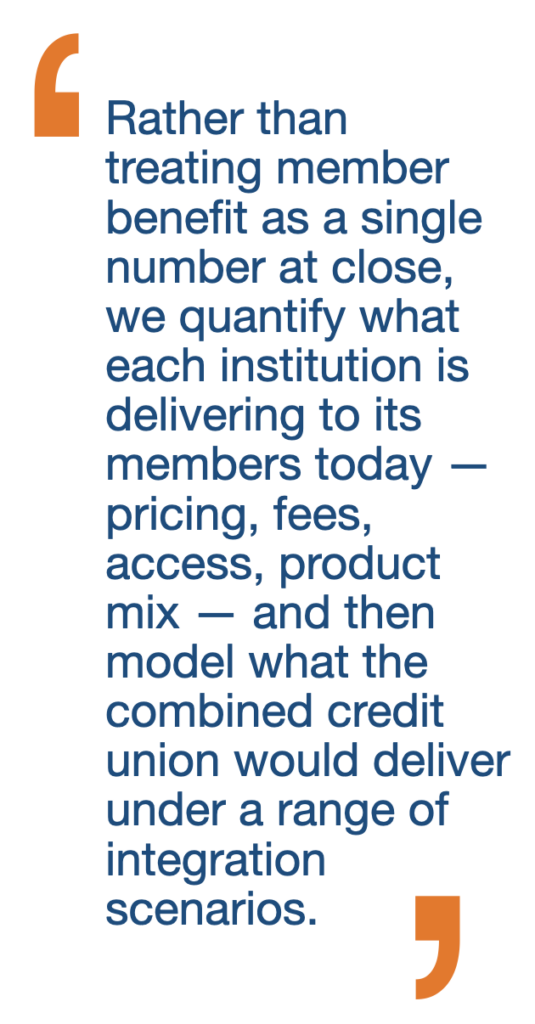

That’s where our risk-based Member Benefit approach comes in. Rather than treating member benefit as a single number at close, we quantify what each institution is delivering to its members today — pricing, fees, access, product mix — and then model what the combined credit union would deliver under a range of integration scenarios. The output is a defensible view of which members are better off, by how much, and where the risks sit.

For the continuing credit union, that becomes the foundation of the member notice, the board’s fiduciary analysis, and the post-close integration plan. For the merging credit union, it’s the answer to the question every board should be asking before it votes: are our members actually going to be better off, and how do we know? We’ve found that grounding the merger conversation in measurable member benefit changes the deal — sometimes it accelerates a combination that clearly serves members, and sometimes it surfaces issues that send the parties back to the table. Either outcome is better than finding out after close.

The CU Daily: Most credit unions began their lives being SEG-based, before momentum shifted to community charters for many. What are the benefits of serving SEGs and what is the best strategy for a CU to use in signing them up?

Brownell: SEGs are one of the most underrated growth levers in the industry. They give a credit union a defined audience to market into, a partner organization that effectively endorses the relationship, and a much lower cost per acquisition than broad consumer marketing. For multiple common bond credit unions, they’re the primary path to FOM growth.

The economics matter here, and they’re worth saying plainly. Because credit unions price better than banks and don’t have shareholders to pay, they can’t — and shouldn’t — be willing to spend as much to acquire a new member or account as a for-profit bank spends to acquire a customer. That math rules out a lot of broad-market paid acquisition.

The corollary is that the most sustainable growth comes from partners where the credit union’s superior pricing solves a real problem for the partner — enough that the partner is willing to introduce the credit union to its people. SEGs are the cleanest version of that: the employer has a financial-wellness problem, the credit union’s pricing is the answer, and the introduction comes from a trusted party at effectively zero marginal cost.

That also means the pitch to the SEG can’t just be “we’d like access to your employees.” It has to quantify what the partnership is worth to the business. We help credit unions put numbers behind that conversation: projected dollar savings per employee, aggregate savings across the workforce, and the downstream benefit to the employer in the form of higher retention, reduced financial stress, and recovered productivity. Framed that way, a SEG relationship stops looking like a favor the employer is doing the credit union and starts looking like a benefit the employer is adding to its package.

The best strategy starts with an honest audit. What groups do you already have, and how penetrated are they? Where are the gaps, geographically and by industry? From there, prospecting splits into two lanes. Geographic prospecting targets employers near your branches. Demographic prospecting targets industries or workforces that match the kind of member you serve well. The right answer is usually a mix of both.

The mechanical side of SEG work, meaning the 4015 form, the overlap letters, the board approvals, is where most credit unions lose time. We built our SEG application software to take that piece off the business development team’s plate so they can spend their time signing groups instead of pushing paperwork.

The CU Daily: On a related note, do most companies—most likely, smaller firms—understand what a credit union is and why it would benefit their employees?

Brownell: Not really, and that’s especially true for the small and mid-sized employers who would benefit most from a SEG relationship. HR leaders at large enterprises often have credit union experience from a prior employer. At a 50-person company, the HR function is usually one person wearing four hats, and credit unions aren’t on the list of things they’ve had time to learn.

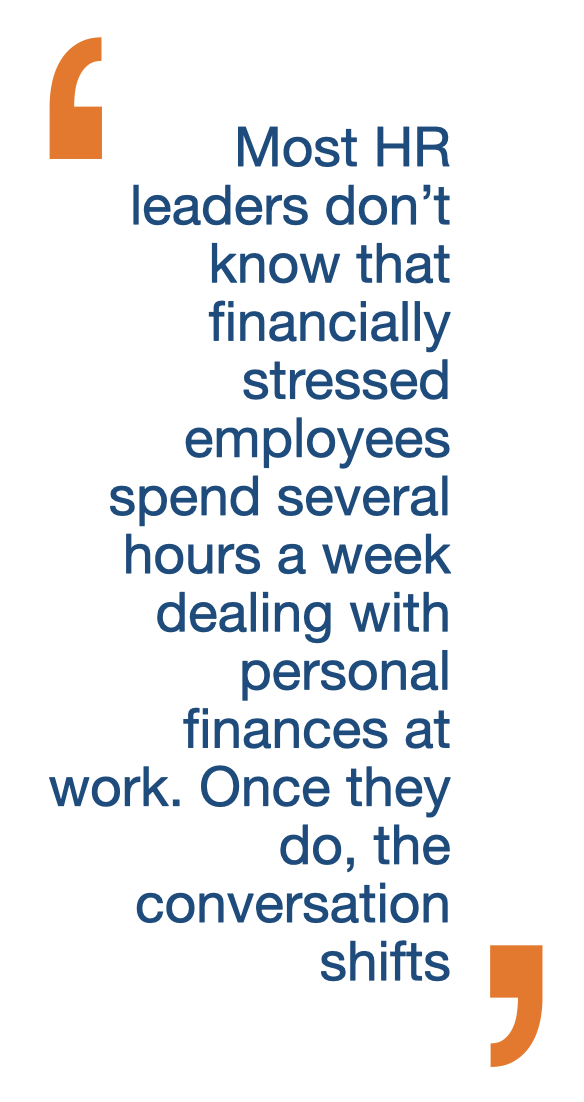

That puts the education burden on the credit union’s business development team. The pitch that lands is rarely, “We’re a credit union and here’s what that means.” It’s “this is a free benefit you can offer your employees, your employees will save real money, and financially stressed employees cost you productivity.” Most HR leaders don’t know that financially stressed employees spend several hours a week dealing with personal finances at work. Once they do, the conversation shifts.

The same logic applies, maybe more so, to the SEGs a credit union already has. Most business development teams are wired to chase new groups and assume the existing ones will take care of themselves. They won’t. HR contacts turn over, benefits packages get re-evaluated, and a SEG that was active five years ago can quietly go dormant. The relationships that stay productive are the ones where the credit union shows up periodically with a refreshed view of what the partnership is actually delivering — how many employees are members, how much they’ve saved in aggregate, what that means for retention and financial-wellness metrics the employer cares about, and where there’s room to do more.

That kind of check-in keeps the credit union in front of the HR team, gives the employer something concrete to point to internally, and surfaces the next round of opportunities — an onsite event, a new-hire enrollment touchpoint, a benefits-fair slot — before a competitor does.

Existing SEGs are also, dollar for dollar, the cheapest place to grow: the introduction has already happened, the trust is already there, and the only question is whether the credit union is doing enough to deserve the next employee.

The CU Daily: As you noted, you recently assisted JetStream FCU in an FOM expansion. What do credit unions with dreams of expanding their own FOMs need to know first?

Brownell: The first thing to understand is that field of membership is a strategy question before it’s an application question. Most credit unions skip ahead to “what counts as a well-defined community” and miss the harder question of where they actually want to grow and why. We start every engagement with strategy, not paperwork.

The second is that the rules are more flexible than most credit unions assume. The NCUA Chartering and Field of Membership Manual leaves real room for creative, well-supported expansions. JetStream is a good example. They had a clear mission to serve underserved families in South Florida, the data supported the addition of Broward County, and we structured the application to reflect both. The result was approval and roughly 4.7 million eligible members.

The third is patience. NCUA review takes time, and the process often involves back-and-forth. Going in with a clean, well-supported application shortens that loop considerably.

The CU Daily: This is a much-discussed issue: What is your view of the future of the branch, and how have branches evolved? Are branches underutilized as tools for growth?

Brownell: Branches aren’t dead. They’re often just in the wrong place, the wrong building, or set up to do the wrong job.

Our research on bank branches in the same size range as most credit unions shows new branches typically grow deposits rapidly for about five years before plateauing. The variance inside that average is enormous. A branch in the 25th percentile pulls in about $8.8 million in deposits in its first year, while a branch in the 75th percentile pulls in $69 million. Same investment, very different outcomes. The difference is almost always site selection and what the branch is designed to do.

It’s also worth saying that the value of a branch isn’t measured only by the people who walk through the door. A nearby branch is one of the strongest signals a consumer uses to decide which financial institutions to even consider. Most people won’t seriously evaluate an institution they’ve never seen a physical presence for, even if they intend to do all of their banking on a phone. The branch functions as a billboard, a trust signal, and a tiebreaker at the moment someone is choosing where to open an account, and that effect shows up in application volume and digital sign-ups well outside the branch’s immediate foot-traffic radius.

Credit unions that only count teller transactions and in-branch account openings systematically understate what the branch is actually doing for them.

So, yes, I think branches are underutilized as growth tools. Most credit unions treat the branch network as a fixed cost rather than a growth asset, and most branch decisions still get made on real estate intuition rather than data. When credit unions plan branches the way they plan a marketing campaign, with a clear target audience, a competitive analysis, and projected ROI, branches earn their cost back and then some. When they don’t, the credit union pays for the mistake for the next 20 years.

For more info, go here.