MADISON, Wis.—Through September 2024, credit unions reported rising equity levels, and projections are calling for the industry’s loan-to-savings ratio to remain north of 85% for 2025. But that good news is tempered by expectations that auto lending, and especially loans for used cars, will slow down in 2025, according to TruStage’s newest Trends Report.

Other loan categories have also seen declines, the report added.

Here is what the data show, according to the Trends Report, which is authored by TruStage’s chief economist, Steve Rick.

Total CU Lending

The data through September reveal CU loan balances were up 0.4%, the same increase reported one year earlier in September 2023., according to the Trends Report.

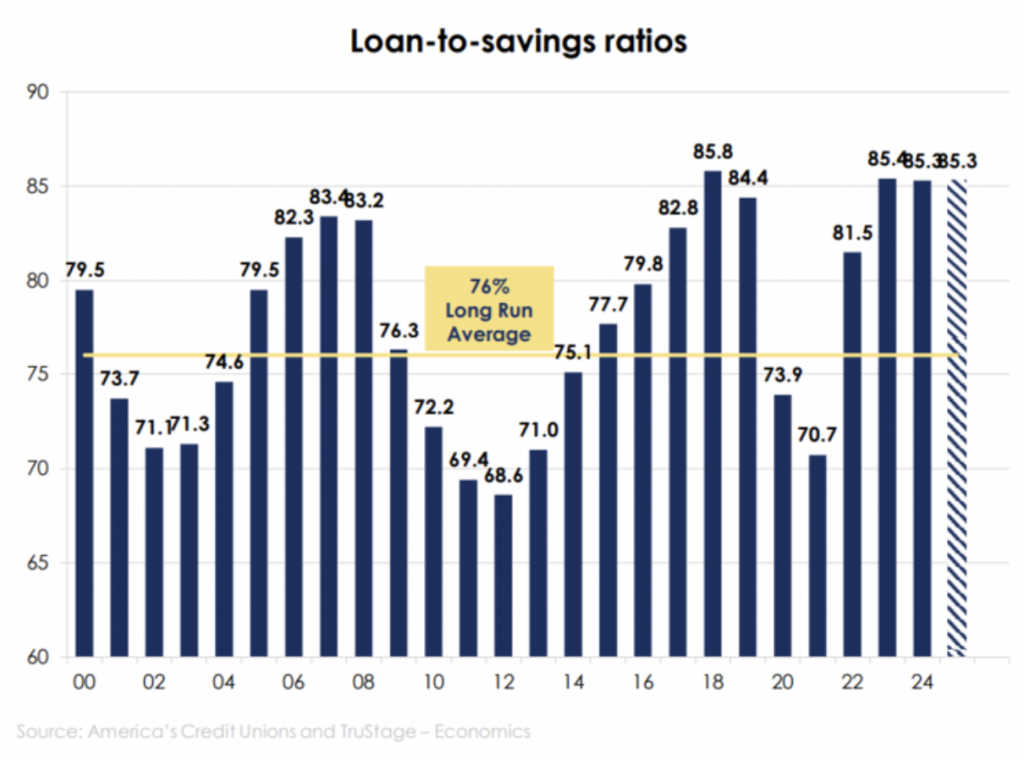

“Driving overall loan growth was strong growth in adjustable-rate mortgages (2.6%) home equity loans (1.4%), and unsecured personal loans (1.4%),” the Trends Report states. “The credit union average loan-to-savings ratio rose to 84.3% in September, down from 84.8% in September 2023, due to savings growth (3.6%) exceeding loan growth (2.9%) during the last 12 months.”

Rick is projecting that based on those trends, loans at credit unions will increase 6% 2025, while savings balances will increase by a similar rise 6%, with those trends combining to maintain the average loan-to-savings ratio above 85% through the end of the year.

That figure is significantly above the 20-year LTS average of 76%, the report states, adding, “This will be the third year in a row the ratio will be above 85%, which hasn’t happened since the late 1970s.”

Rick noted in his analysis, “This high loan-to-savings ratio can boost credit union earnings, heighten liquidity concerns, attract regulator scrutiny, lead to the need to borrow additional wholesale funds, require higher interest rates on deposits, reduce the investment portfolios to maintain lending volumes, and increase the need for additional capital reserves.”

Consumer Installment Credit

Pointing to Federal Reserve data showing, outstanding consumer credit for all lenders rose just $3.2 billion in September, which is significantly below the $15 billion monthly average, the Trends Report stated credit unions now hold 14.8% of all consumer credit, down from the 15.0% reported in September 2023.

“Going forward, expect nonrevolving credit growth to be below its 7% long run trend in 2025 due to satiated consumers’ demand for autos and interest rates remaining elevated through most of next year,” the Trends Report projects. “Revolving credit growth will also slow due to tighter lending standards and households trying to pay down high-cost debt.”

Vehicle Loans

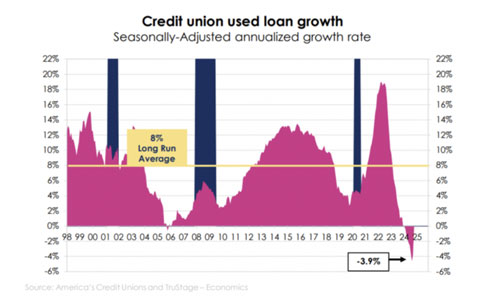

A bread-and-butter product for credit unions, used auto loans, experienced -3.9% seasonally-adjusted annualized growth rate in September 2024, the slowest pace on record due to high auto loan interest rates, high used car prices, little pent-up demand for used cars, more new-car inventory and the accelerating amortization of the significant number of loans originated in 2022, according to Rick.

While used car prices rose markedly over the last couple of years, a ramp up in new car production has pushed down used car prices, which have fallen 18% from a record high in February 2022, the Trends Report notes. Those prices are still approximately 28% above pre-COVID 19 prices set in 2019, the report adds.

“Credit union new-auto loan balances fell at an 8.3% seasonally-adjusted annualized growth rate in September, the slowest pace since the spring of 2011 due to competitive financing offers from competitors,” according to the Trends Report analysis. “On a monthly basis, credit union new-auto loan balances fell 0.4% in September, worse than the 0.1% decline reported in September 2023. New-auto loan balances fell 5.6% during the last 12 months while used auto loan balances fell 1.2%.”

Rick is projecting that automobile sales will increase over the next few months as rates decline and concerns over future tariffs lead car buyers to purchase sooner rather than later.

Real Estate

When it comes to real estate, the Trends Report found CU fixed-rate first mortgage loan balances declined 0.3% in September, below the 0.2% gain set in September 2023.

According to the report:

- Credit unions sold 33.7% of mortgage originations into the secondary market during the first half of the year, up from 22.3% in the similar period of 2022 and 22.1% in 2023.

- ARM loan balances rose 2.6% in September, above the 2.1% gain recorded in September 2023.

- The contract interest rate on a 30-year, fixed-rate conventional home mortgage fell to 6.18% in September from 6.50% in August but down from the 7.20% reported in September 2023.

“House price appreciation is moderating due to the lowest housing affordability in four decades and a modest increase in the inventory of homes for sale,” the analysis states.

Savings And Assets

Meanwhile, through September, CU members’ demand for “money deposits” (checking, savings and MMAs) declined at a 0.2% seasonally-adjusted annualized rate in September and has been in negative territory since July of 2022, according to the new Trends Report.

“This is a dramatic reversal from the greater than 30% growth rate recorded in the summer of 2020 when COVID-19 stimulus checks were being sent out to millions of Americans,” the analysis observes. “Meanwhile, demand for investment type accounts like certificate of deposits are growing at an 18% annualized rate. The high federal funds interest rate is the major factor causing this decline in money deposits as members withdraw funds from low-yielding savings deposits and place them in higher yielding certificate of deposits or money market mutual funds.”

Negative Corelation

Rick’s analysis pointed to the strong negative correlation between short-term interest rates and holdings of checking, savings, and money market deposit accounts.

“This shift in credit union deposits helped increase credit union cost of funds from 0.36% in the first half of 2022 to1.88% in the first half of this year. This is known as the ‘mix effect’,” the Trends Report states. “But there is also a ‘rate effect,’ whereby credit unions are raising their deposit interest rates to prevent deposit runoff or what is known as disintermediation.”

The Trends Report found savings balances per member rose $224 during the 12 months leading up to September, to $13,704 from $13,480 in September 2023.

“This 1.7% increase in savings per member is significantly below the 25-year average of 4.4%,” the report states. “Some members are spending some of their savings due to falling real wages, while other interest-rate-sensitive members are moving funds out of their credit union to higher-yielding alternative investments.”

Rick is projecting that as the Fed lowers the fed funds interest rate in 2025 money deposits will again experience growth.

Equity And Other Key Measures

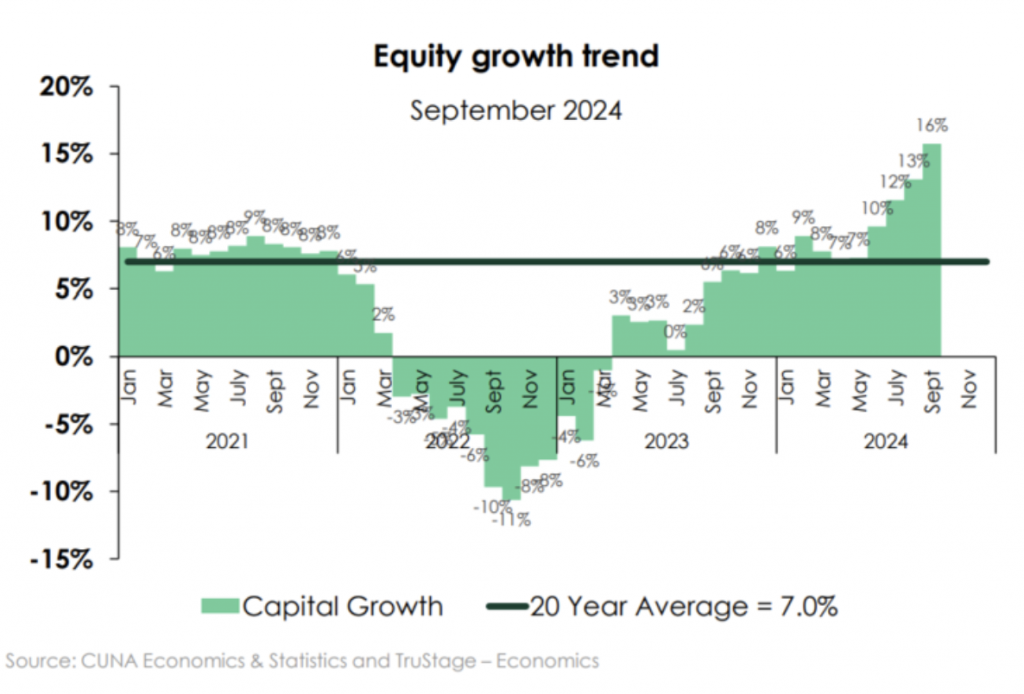

Overall, credit unions’ equity-to-asset ratio rose to 9.7% in September, up from 9.6% in August and 8.7% in September 2023 due in part to falling interest rates increasing the market value of investments classified as available for sale, according to the Trends Report, which noted that through June 2024 credit unions had classified 75% of their investments as available for sale and therefore were reported at fair value.

“Many believe the Federal Resave will decrease short-term interest rates by one percentage point during the next 12 months, which will then boost investment valuations,” Rick stated in the Trends Report. “Changes in securities value between accounting periods are included in the equity section of the balance sheet. For example, a one-year 5% Treasury note would rise in value by 1.0% if interest rates fell 1 percentage point, a two-year 5% Treasury note would rise by 1.9%, a four-year 5% Treasury note would rise by 3.6% and a nine-year 5% Treasury note would rise in value by 7.4%.”

The report further found that through June credit unions held 15% of their surplus funds in the 5–10-year maturity bucket, down from 18.6% one year earlier. If the Federal Reserve lowers interest rates another 100 basis points over the next 12 months as inflation falls to their 2% target, expect investment values to continue to rise as well as equity levels, the report states.

“The above-mentioned equity tailwind along with the net income earned during the last year increased credit union equity levels 16% during the last 12 months the fastest pace since February 1994,” the report states. “This equity growth rate is also known as the return-on-equity ratio and is one of the most important credit union financial ratios. For the last eight months, the return-on equity ratio has been running above the 7% average recorded over the last 20 years.”

Credit Union Numbers

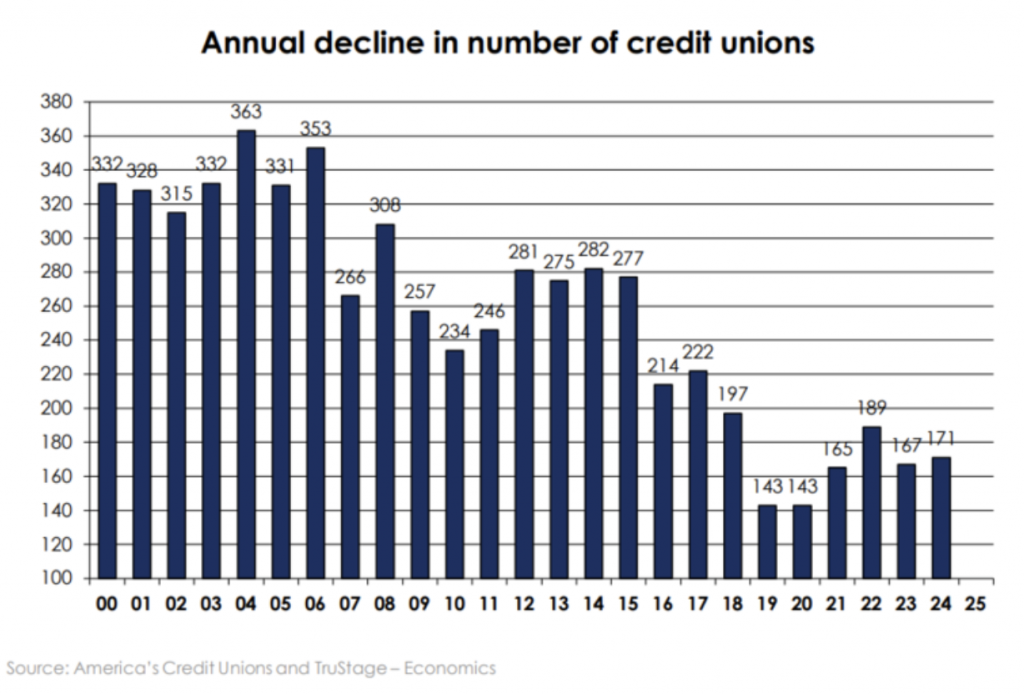

As of September 2024, the Trends Report, which is based on data gathered by America’s credit unions, found 4,668 credit unions were in operation, a decline of 171 charters from September 2023.

“Year-to-date, the number of credit unions fell by 128, slightly faster than the 124-decrease reported in the first nine months of 2023. NCUA’s Insurance Report of Activity showed 50 mergers were approved in the third quarter (up from 39 in the third quarter of 2023), with an average asset size of $100 million,” the report states. “The average asset size of the continuing credit union was $849 million.”

The report further notes that, based on filings with NCUA, 40 of the mergers were due to credit unions wanting expanded services, six were due to poor financial condition, two because of poor management, and one was due to an inability to find officials.

“Expect mergers to accelerate to 175 during 2025 due to the ongoing liquidity crisis and smaller credit unions wishing to expand the services offered to their members,” the report forecasts.

CU Membership

Meanwhile, the report notes that credit unions added more than 2.2 million members in the first nine months of 2024,which is below the 3.6 million added in the similar time period of 2023.

“Weak demand for consumer loans was the major factor leading to the slowdown in membership growth,” the report states. “Also contributing to the membership growth slowdown was the decline in job growth as only 1.7 million new jobs were added in the U.S. economy during the last nine months, which was significantly below the 2.4 million added during the same period in 2023.”