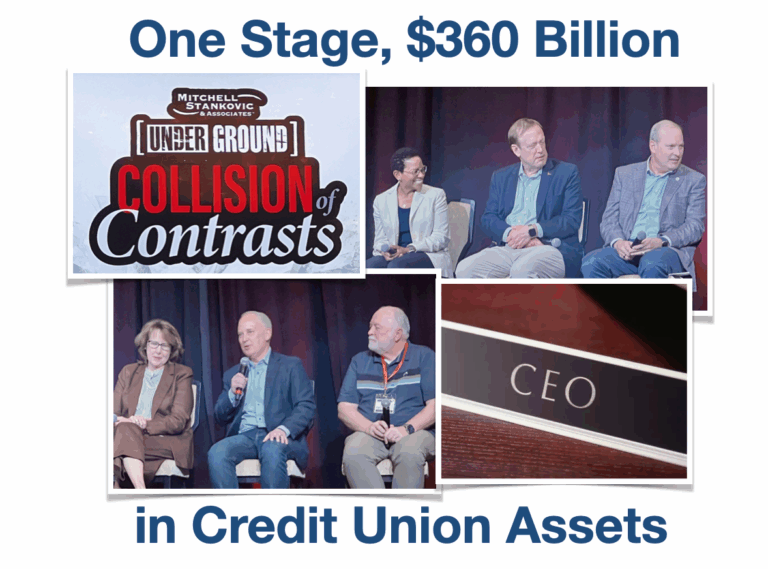

LAS VEGAS–In a highly unusual occurrence, the CEOs of six of the seven largest credit unions in the United States came together here and discussed everything from the values that drive them to what they do in financial education to how all CUs “share the same last name” and must stick together.

The CEOs were on hand for Mitchell Stankovic’s Underground meeting and will also be appearing this week on the main stage as part of the giant Money 20/20 conference in Las Vegas, the first time CU CEOs have been so featured.

All of the CEOs at various points in their remarks suggested that their large respective asset sizes—the credit unions combined represented approximately $361 billion in assets—do not mean they do not fulfill the mission of credit unions, and frequently cited examples of how they give back to members and communities.

The Panelists

Appearing during a session that was moderated by Sue Mitchell, president of Mitchell Stankovic & Associates, were:

• Beverly Anderson, president and CEO of BECU

• Bill Cheney, president and CEO of SchoolsFirst FCU

• Dietrich Kuhlmann, president and CEO of Navy FCU

• Leigh Brady, president and CEO of State Employees CU

• Sterling Nielsen, president and CEO of Mountain America CU

• Thayne Shaffer, president and CEO of America First CU

The Q&A

Here is a look at some of what was shared and discussed:

Mitchell: Credit unions are all about value-driven leadership. What are key points for Navy FCU?

Kuhlmann: We look for ways to help our fellow credit unions and smaller credit unions. We don’t want to make this journey alone. A large credit union is still a credit union, and it’s a credit union because of how it’s run. Our motto is “The members are the mission.” We do many of the same things you do, arguably at a different scale. We are about $194 billion in assets, and we just added our 15 millionth member a few weeks ago.

Cheney: SchoolsFirst FCU serves school employees and families throughout the state. We were founded in 1934 by 123 teachers. We have a TIP charter and have 1.5 million members (and $34.5 billion in assets).

Our mission is to provide world-class personal service and financial service to our members. I 100% agree that our credit union is operated as a credit union. We have a voluntary board of directors elected by our members to act in their best interests.

Brady: We are just in North Carolina and have about $58 billion in assets and about 3 million members. Our mission is simple: We work very hard to help our members keep money in their pockets, where it belongs, similar to what every credit union does.

We have a payday lending alternative loan, and we require people to save a little of that, and they now have $57 million in savings. We help teachers during the two months they don’t get paid. When we started, we had 17 members and $437. It’s grown a lot, but we have the same purpose.

Anderson: It’s amazing: whether it’s large or small, credit unions are all experiencing some of the same things and trying to do great things for our members.

This is my third year in the movement, and it’s been such an incredible learning journey. We are just about $30 billion with 1.5 million members in Seattle. We have a purpose that says we bring people together to improve the financial well-being of our members and their communities. Our 3,200 employees get up every single day trying to figure out how to fulfill that purpose. They donate 32,000 hours per year of their time. We show up every day working to help people move along on their financial journey.

I love the work we all do together. I love the support we provide small credit unions. We have one, Express Credit Union, that has a microbranch in one of our offices. We have loaned them someone for a year to help with a core conversion.

Nielsen: Utah is a unique environment for credit unions. We have a very high concentration of CU membership in the state. We have a unique environment in that it is highly competitive, but it is an honor to work and partner with so many unique people in the industry. We are about $22 billion in assets and have 1.4 million members, with branches in Utah, Idaho, Arizona, Nevada and Montana.

One of the things that has made us successful is working in those small communities. What we offer has really resonated in those communities. We have about 105 branches and continue to offer them. Branches are where you change lives.

I believe credit unions still are that best-kept difference. We love to share stories of how we have been able to impact members.

Shaffer: We are in Riverdale, Utah, north of Mountain America. Our credit unions have grown up together. We know each other well. We have $23 billion in assets with 1.5 million members in six Western states.

It is a big challenge to serve the different needs of members in all of those different communities. Our aspiration is to be able to offer the opportunities to members to achieve their financial goals. We do that in the ways you have heard others talk about.

I live in the congressional district in the U.S. with the highest concentration of credit union members, and Utah has four of the top 10. We are very involved in advocating for credit unions. We make multiple trips per year to Washington and have strong relationships with our elected officials at the state and federal level.

Mitchell: What about financial education?

Brady: Financial education is a big piece for us. It is done in a variety of ways, such as the salary advance loan and programs for those who are not as disciplined as they could be. It could be going out into the schools and communities. I think last year we reached 87,000 kids. It can be done through a foundation. With financial education, we believe you start early and often. That makes for a successful member and citizen moving forward.

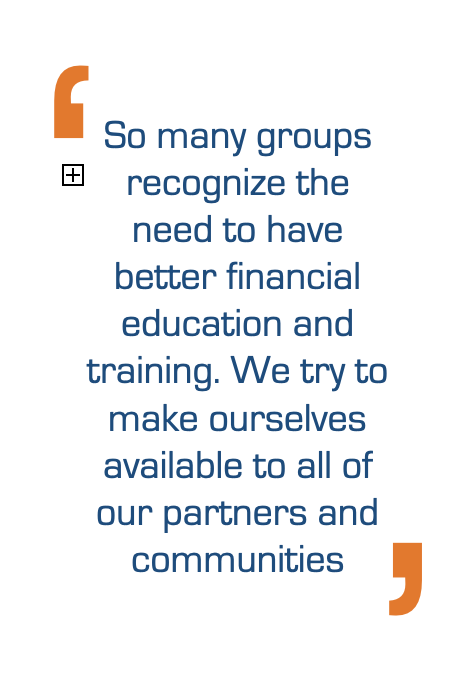

Shaffer: There has been a big change in how we talk about financial literacy from the beginning of my career. When I started, it was all about teaching in high school and how to keep a checkbook. Today, we get calls from universities, community groups, everybody out there. So many groups recognize the need to have better financial education and training.

We try to make ourselves available to all of our partners and communities. We have a curriculum we provide for free and send people out to do that. I would encourage anyone involved to get involved.

Anderson: You think about big disciplines in our life, such as driving, and we have to learn how to do that. There is a whole education system. But if you think about one of the most important disciplines we carry throughout our lives, we don’t teach that.

I think credit unions do such an incredible job. One of the things we do is we have launched a financial health hub, and we invite our members in to learn. There is so much content. The place where it comes to fruition is when they come through our doors and need to be taught and educated. I think this is an important thing missing in the lives of members.

We have had a loan repricing program in which we teach people to manage their credit. Every year we take that rate down. We’ve repriced 650,000 loans with $29 million in savings right into their pockets.

We do digital envelopes for the compartmentalization of savings. People love the discipline of compartmentalized savings. And what’s cool is we can see what they are saving for. The big areas are car payments and mortgages, but they also have aspirations, such as travel. That allows us to help them even more.

Mitchell: You all have a lot of employees—do you educate them?

Kuhlmann: We do. We are way above the national average in using the 401(k); about 94% of employees use it, with a 7% match.

Education is one of the fundamental things we do. We are on 92 (military) bases. You don’t make money on a credit union on the base. It’s a loss. You do have an operating agreement that you are available to do training for everyone on that base. We never turn down that opportunity.

I think this is where we are different in credit unions, and we should be proud.

Cheney: It’s an honor to be here as CEOs, but it’s the team that meets with members. And yes, we do work with them on their financial well-being. Our number one priority is member engagement, and we understand to achieve that we have to have an exceptional team. If our team is disengaged or if they are not financially thriving themselves, they are not going to focus on our members’ financial well-being.

Shaffer: A success story for us is we have an organization that is separate from America First called the Care-A-Lot Fund that is fully funded by our employees, and it is there for employees only who may be going through catastrophic problems. It is well funded. It has its own board. Our employees really work to watch out for the financial well-being of their peers. To me it is a crown jewel of what America First purports to be.

Mitchell: How does trust affect our partnerships?

Nielsen: It’s not just our partners, but we as financial institutions need to have that trusting relationship. Our partners have really helped us succeed. We would not be where we are if it were not for good, strong partnerships.

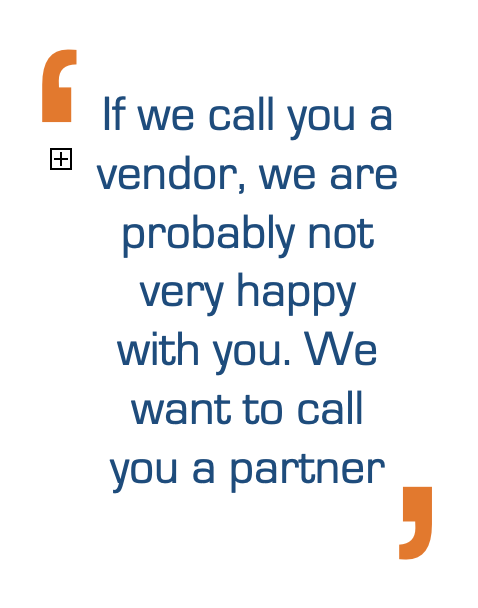

Kuhlmann: If we call you a vendor, we are probably not very happy with you. We want to call you a partner. You are in this with us. We are both striving for the best outcomes for both sides.

Cheney: Trust to me is the foundation the entire movement is built upon—whether with our team, with our members, with our partners, with our regulators.

Brady: We are going to be going through a core conversion and converting from 1983 technology. When we were looking at partners, I cursed a little bit because I said I want someone who will allow us to help other credit unions and smaller credit unions, whatever it might be. I wanted a partner to live with us in that space and not just be out to make money in the end.

Nielsen: One thing about our partners is they are always there for us, and we want to be there for them. We have helped them do development and funded some employees, so it is kind of like co-development so we have the best product for the industry.

Mitchell: What would you like to leave the audience with?

Anderson: I am excited to be a part of this movement. It has changed my life, and we have changed the lives of members. My challenge is to keep doing the work and to keep finding those populations of underrepresented people who really need us to lean into them and improve their financial well-being.

Cheney: I agree. We are in this together. We’re all credit unions. We share the same last name. Let’s use our collective energy to help each other. The tax battle this year turned out OK, but it’s not going to be the last time. We are large credit unions, but collectively we are still smaller than the largest banks. Let’s work together.

Kuhlmann: Find different ways to give back. Every one of you knows where your members’ pain points are. With the government shutdown, we have put up $2.5 billion in paychecks, so if you have direct deposit with us, we will pay you. That was started years ago, and other credit unions do it, too. I don’t know too many banks that do it. With our Overseas Banking Program, the government gives us a big fee. We donate that to charities.

Brady: We have social impact. And social impact is very, very important to today’s youth. One thing my mom always said was to leave something better than you found it. My charge to you is however you are going to do that, leave it better than you find it.

Nielsen: I am very proud to be part of a community that makes a difference every day. For those that are credit union partners and future partners, we need you, you make us better, and we really strive to leverage our trust with our members to help you become better as well. Working together, we can make a huge difference in the world.

Shaffer: There are a lot of people out there who want people to believe credit unions are getting very bank-like as they get bigger. A lot of our conversation with our bank partner we acquired had to do with the differences between credit unions and banks, and the charge that we have to watch out for our members’ well-being results in different types of decision-making.