TROY, Mich.— Online-only banks have become one of the fastest growing segments in financial services, and a new study reveals which are succeeding the most—and why—as well as why some are struggling.

According to the JD Power 2026 U.S. Direct Banking Satisfaction Study, released today, online-only banking providers—which the company said consists of both federally chartered online banks and neobanks, which do not have federal bank charters but partner with traditional banks to provide deposit insurance and other critical infrastructure–are continuing to win customers from traditional banking institutions and drive high levels of customer satisfaction by establishing strong emotional connections rooted in personalized digital experiences.

While the online-only banking marketplace is largely succeeding on personalization, some neobanks are struggling when it comes to high incidence of customer problems and weaker telephone and online chat support when problems occur, J.D. Power said.

‘Emotional Connections’

“Online-only banking providers are really succeeding at establishing emotional connections with their customers by delivering highly personalized digital interactions, along with products and services that help them feel understood and that they are moving toward their financial goals,” Paul McAdam, senior director of financial services intelligence at JD Power, said in a statement. “Within the online-only banking marketplace, however, JD Power finds that many neobanks are not performing as well as online banks when it comes to basic blocking and tackling in areas like the convenience of reaching customer service and single-contact problem resolution. While these challenger brands excel at fast funds availability and practical financial health support, their day-to-day customer service is not as strong as it needs to be.”

Key Findings

J.D. Power said key findings in the new study include:

- Online-only banking providers deliver personalized user experience: Both online banks and neobanks perform equally well on customer perceptions of being friendly, personalized and customer-centric. Both perform well on helping customers grow their money and avoid fees, which is foundational to establishing an emotional connection with customers.

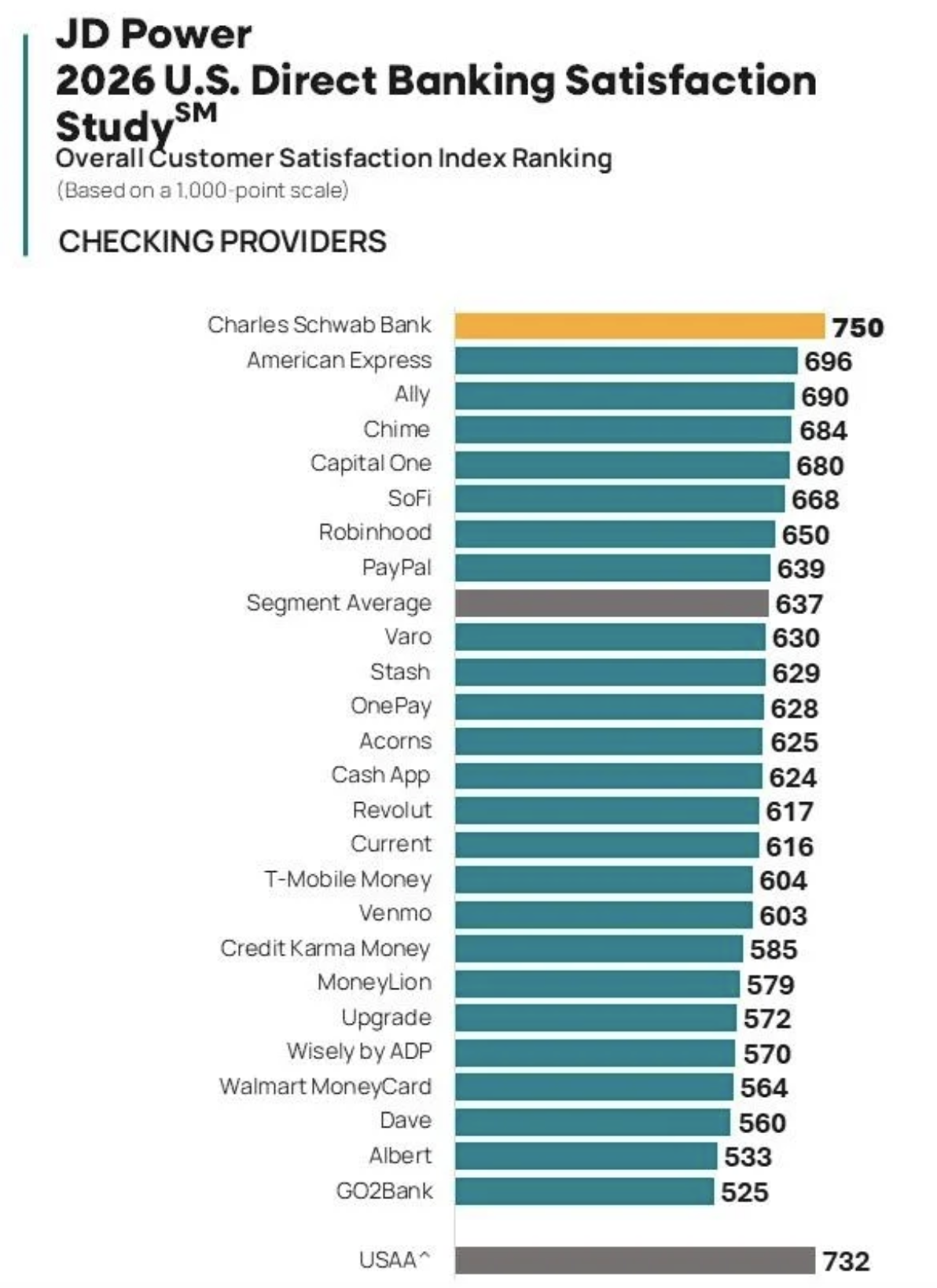

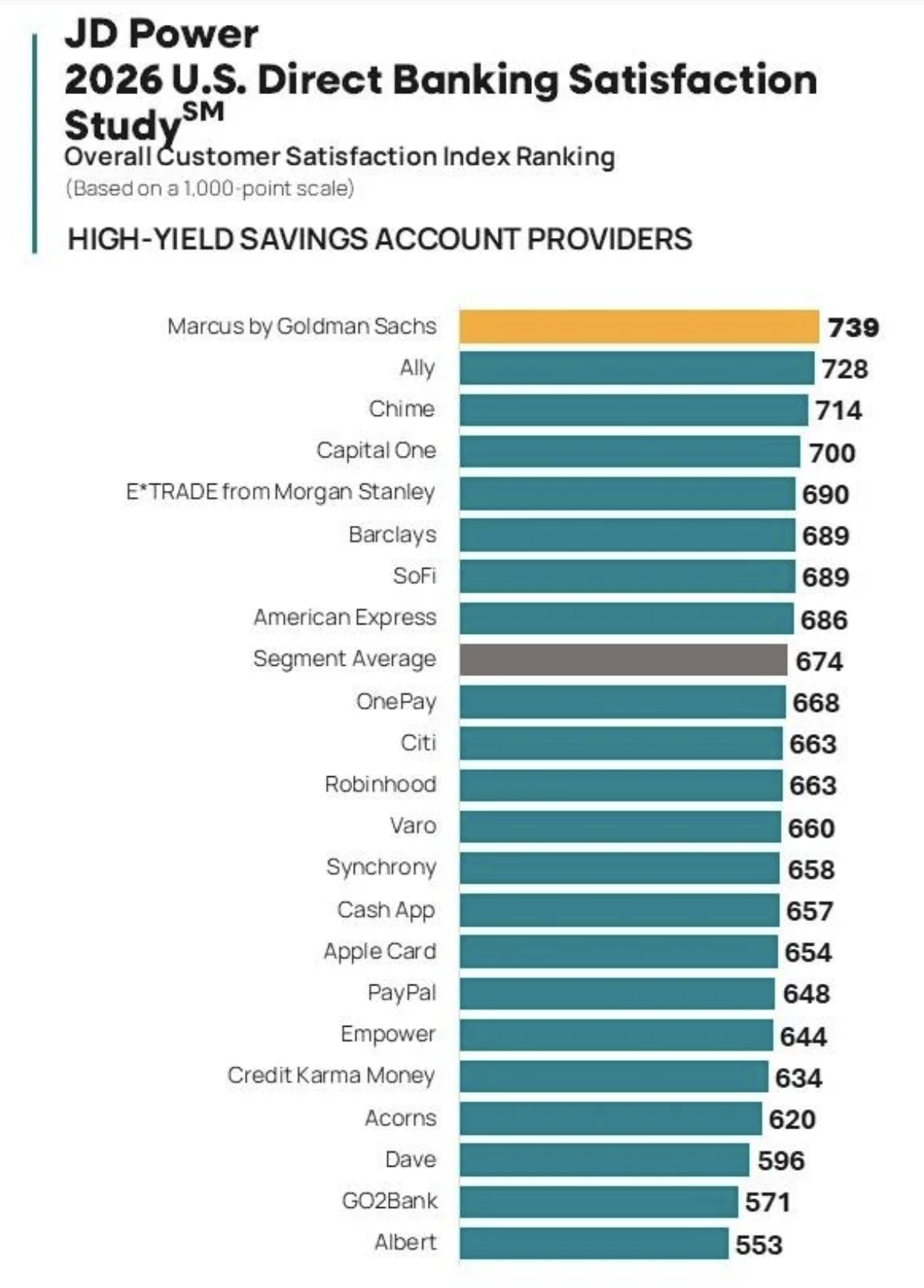

- Online banks outperform neobanks in overall satisfaction: The overall customer satisfaction score for online bank checking accounts is 674 (on a 1,000-point scale), which is 52 points higher than neobanks (622). Customer satisfaction for online bank high-yield savings accounts is 689, which is 32 points higher than neobanks (657). The gaps in performance are driven by a higher incidence of problems associated with the debit card and fraud/unauthorized activity, and with weaker satisfaction with telephone, online chat and email support.

- Significant gap between highest- and lowest-ranked online-only banking providers: The gap in overall satisfaction scores between the top-performing online banks in the study and the lowest-performing neobanks in the study is 225 points in the checking segment and 186 points in the high-yield savings segment, highlighting the widespread variation between the customer service and account management capabilities of different providers in this rapidly growing space.

Study Rankings

According to J.D. Power’s study, Charles Schwab Bank ranks highest in overall satisfaction among checking providers for an eighth consecutive year, with a score of 750. American Express (696) ranks second and Ally (690) ranks third.

Marcus by Goldman Sachs ranks highest in overall satisfaction among high-yield savings providers with a score of 739. Ally (728) ranks second and Chime (714) ranks third.

Study is Redesigned

J.D. Power said the U.S. Direct Banking Satisfaction Study was redesigned for 2026, thus overall satisfaction scores are not comparable with previous-year studies. The study, now in its 10th year, measures overall satisfaction with online-only bank and neobank checking and/or high-yield savings/money market products based on six dimensions (in alphabetical order): customer service; ease of moving money; helps grow money; level of trust; managing account via mobile app; and managing account via website.

The study defines online-only banks in two categories: 1) online/branchless institutions with federal banking charters with either the Federal Reserve Board, the Office of the Comptroller of the Currency (OCC) or the Federal Deposit Insurance Corporation (FDIC) as their primary regulator, and 2) neobanks, which do not have federal bank charters, but partner with federally chartered banks to provide FDIC deposit insurance and other critical infrastructure.

The 2025 study is based on responses from 16,309 online-only bank customers and was fielded from December 2025 through February 2026.

Additional information can be found here.