WASHINGTON — U.S. consumer borrowing rose modestly at the start of 2026, with credit card balances continuing to expand faster than other forms of household debt, according to the Federal Reserve’s latest G.19 consumer credit report.

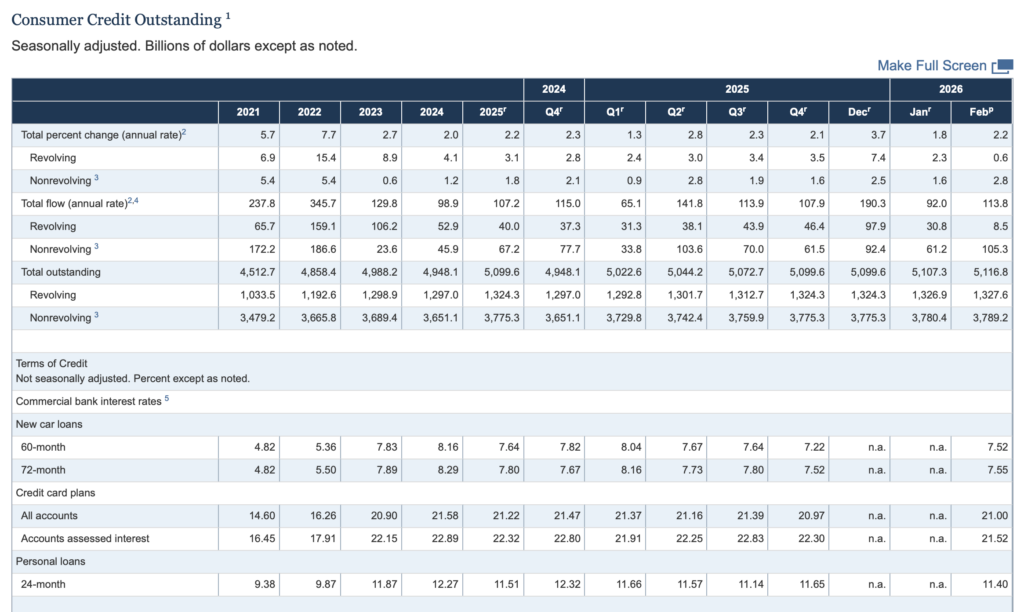

Total consumer credit increased at a seasonally adjusted annual rate of 1.9% in January, the Federal Reserve said.

The gain reflected divergent trends between revolving and nonrevolving credit:

- Revolving credit, which includes credit cards, increased at a 4.3% annual rate.

- Nonrevolving credit, such as auto and student loans, rose at a slower 1.1% pace.

The Fed’s data show total outstanding consumer credit reached roughly $5.1 trillion in January.

Revolving credit balances — a key indicator of credit card usage — continued to edge higher in dollar terms, climbing to about $1.33 trillion on a seasonally adjusted basis.

Continued Reliance on Cards

The G.19 report tracks borrowing by individuals for household, family and other personal expenditures, excluding mortgages. It divides credit into two main categories: revolving credit, which allows repeated borrowing up to a limit, and nonrevolving credit, which is typically repaid on a fixed schedule.

January’s data point to continued reliance on credit cards even as overall borrowing growth remains subdued. Revolving credit has shown stronger momentum than other categories in recent months, reflecting its role in helping households manage short-term expenses, while nonrevolving credit growth has been comparatively restrained.

The Federal Reserve releases the G.19 report monthly, providing one of the most closely watched snapshots of consumer borrowing trends and household balance sheets.