ST. PETERSBURG, Fla.– While growth in purchasing activity on their cards remained positive, February year-over-year results softened for both credit and debit activity, according to the March 2025 edition of the Velera Payments Index, which also includes a deeper look at delinquencies and differences by generations and credit scores.

In releasing its new data, Velera noted the Consumer Confidence Index posted a sharp decline in February of 7.0 points to 98.3 (1985=100), and remains at the bottom range of monthly scores since 2022. In addition, the University of Michigan Index of Consumer Sentiment fell in February by 10% to 64.7.

The Political Landscape

“While the drop was across all age and income levels, sentiment was unchanged for Republicans and fell for both Democrats and Independents, illustrating the differences related to current economic policies and the political landscape,” Velera stated.

In addition, in the Labor Department’s March 12 update, the Consumer Price Index (CPI) increased 0.2% in February, bringing the cumulative 12-month rate of inflation down to 2.8%, with the Shelter index accounted for nearly half of the February increase. The U.S. Bureau of Labor Statistics (BLS) reported the overall unemployment rate increased slightly for February to 4.1%, or 7.1 million people, but that was before government job cuts were announced.

The Federal Reserve is set to conclude its meetings on Wednesday, and analysts are not anticipating a reduction in rates.

‘Proactive’ Support Needed

“As credit card delinquencies continue to rise, albeit at a slower pace than in previous years, credit unions must proactively support members facing financial hardship,” David Knowles, SVP, Collections & Disputes and President, TriVerity at Velera, said in a statement. “With serious delinquency rates projected to reach 2.76% by the end of 2025 – driven by inflation, interest rates and ongoing economic uncertainty – credit unions should also consider the growing impact of Buy Now, Pay Later (BNPL) services, particularly among the youngest generations. By offering financial education, flexible repayment options and early intervention strategies, credit unions can help members manage debt responsibly and avoid deeper financial distress.”

The Key Takeaways

According to Velera, the key takeaways for February include:

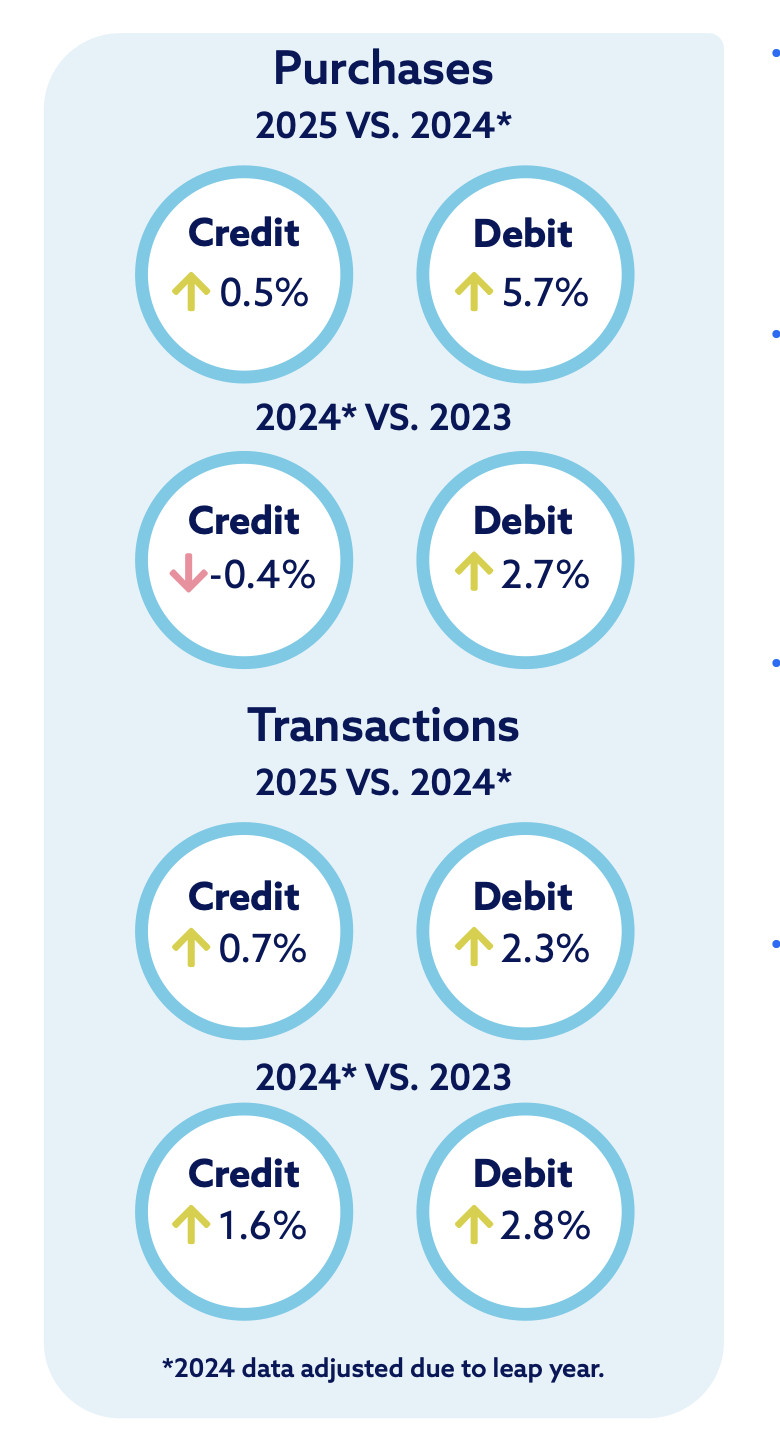

- Growth rates softened for credit and debit in February. On an adjusted basis (to account for the leap year in 2024), credit purchases were up 0.5% and debit purchases were up 5.7%. Credit transactions were up 0.7% and debit transactions were up 2.3%. Unadjusted (with one extra day in February 2024), credit purchases were down 3.4% and debit purchases were up 1.4%.

- Money Services maintained its position as the top contributor to growth in debit purchases, accounting for one-third of the year-over-year increase. The Goods and Services sectors represented the second- and third-largest impact for debit, respectively. For credit purchases, the Services sector was the largest contributor to growth for February. Within Services, insurance sales/premiums were the top merchant category, Velera said.

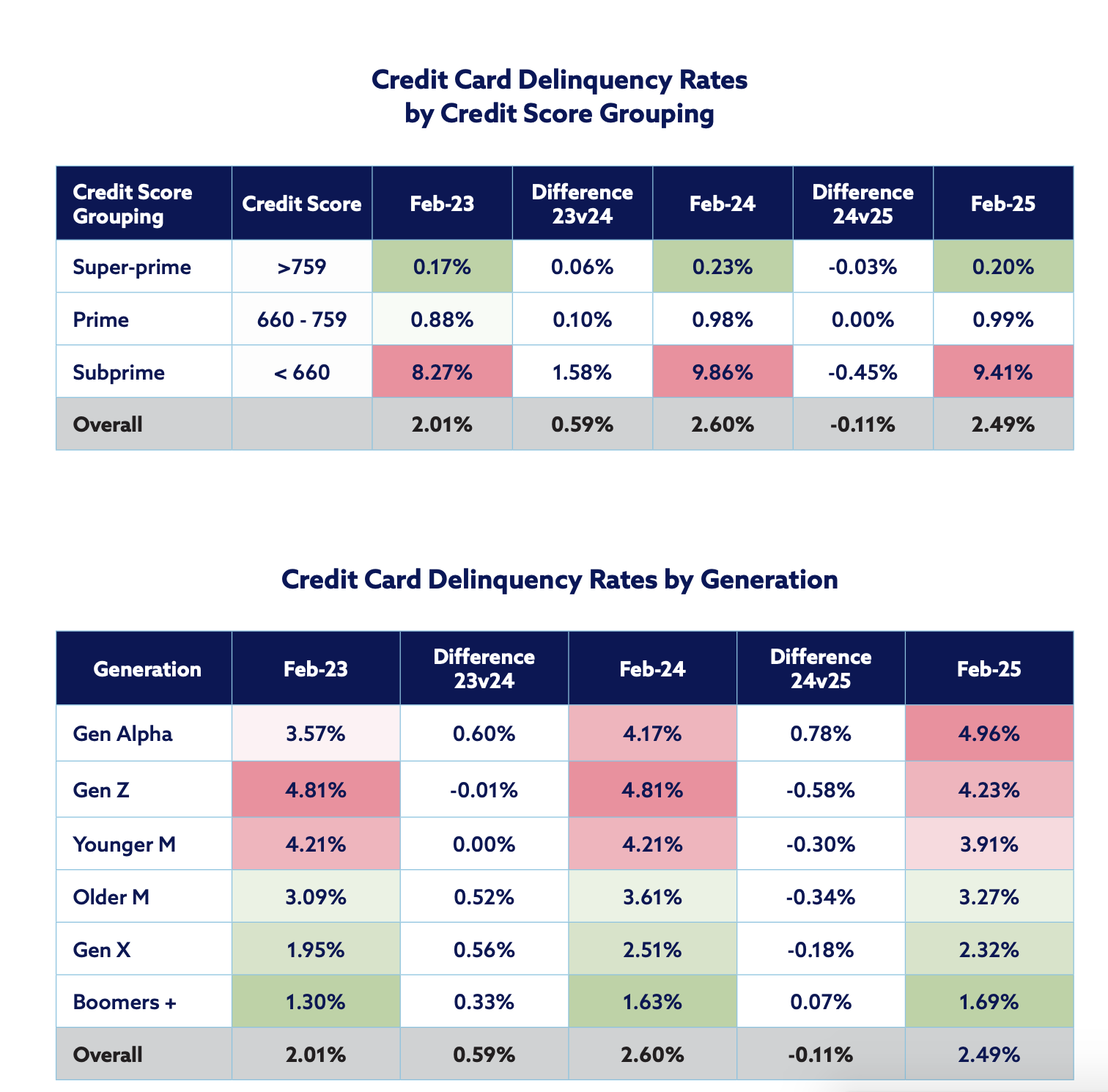

- Delinquencies rose after bottoming out in May 2021 at 1.03%, but have remained stable since our last delinquency Deep Dive (February 2024). Overall credit card delinquencies for February 2025 were 2.49%, down 0.11% year over year.

“However, we also saw higher delinquency rates within the younger age demographics, as seen in the notable increase for the youngest generational segment (Gen Alpha), up 17% year over year to 4.96% for February 2025,” Velera reported.

The full report is available for download here