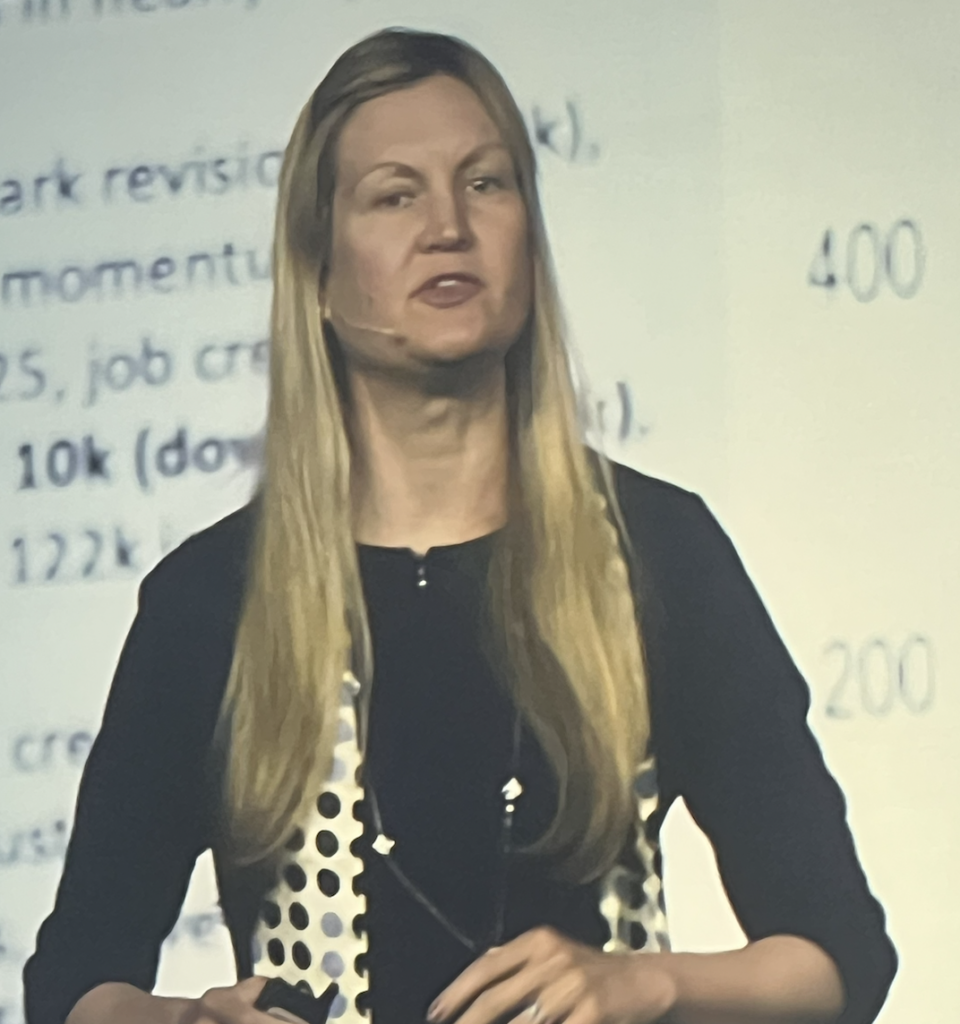

PALM DESERT, Calif.–Questions related to the economy that seem to be on everyone’s mind were discussed by one economist here.

Speaking to Origence’s Lending Tech Live event, Dr. Lindsey Piegza, chief economist with Stifel Financial, told attendees the U.S. consumer continues to be “resilient” thanks to gains in the labor market, but there are any number of issues that could tip the cart.

Among the economic issues touched on by Piegza:

Job Growth

While the U.S. has seen continued job growth, Piegza said the pace has “slowed precipitously” to about 50,000 jobs per month. That figure is above what is known as the “breakeven rate,” Piegza explained, or the minimum level needed t maintain full employment.

“We see the labor market slowing in terms of topline job creation. We also see the unemployment rate remain impressively low around 4.3%,” Piegza said. “We’ve been below 4.5% now for several years,” a trend line she said is “impressive.”

“We’re still notably below the lower bound that the Fed tells us is the full employment range now,” she added.

Artificial Intelligence

The fears and the hopes around AI are real, according to Piezga.

“AI has significantly contributed to productivity and efficiency, allowing businesses to offset challenges in this market,” said Piegza. But at the same time we could see AI displace millions of workers in this year alone, and could be doing 80% of tasks done by humans by the year 2050. There will be a sizeable displacement factor in the way we work now and in the future.

“In near term, as long as labor remains somewhat scarce, I do expect (employment) to remain positive. Forty percent of businesses say retaining skilled labor is a challenge.”

Consumer Balance Sheets & Household Debt

Piegza said many households are “turning to intergenerational wealth transfers. which is just a nice way of saying mom and dad and grandma and grandpa are rolling down some of those funds,” Piezga “Consumers have been turning to 401(k)’s, with hardship withdrawals up double digits since the start of the year. And, of course, now consumers are turning increasingly to buy now, pay later options. Credit cards are at the top of that consumer support list, with outstanding balances topping out $1.3 trillion. Auto loan debt is rising at $1.7 trillion.

“Now, this is an alarming amount of debt for the average American, but we do have to put it in the context of the health of the household balance sheet,” Piezga continued. “And to do that we look at the ratio of debt payments relative to disposable income. This gives us a picture of how the household is able to service that debt now…This ratio is still an amazing; it’s at a multi-decade low…What this tells us is there is still a lot of room to grow the liability side of the typical household balance sheet before it becomes the traditional red flag.”

Still, Piezga stressed that the consumer is not on “unshakable footing by any means. They continue to feel the pain. There is a loss of momentum as fewer dollars are spent in the market place.”

Piezga added that she is not overly concerned with delinquency rates at this point, as the growth has mostly been at the lower end of the credit spectrum.

Inflation

Price inflation has complicated data around consumer consumption data, offering as an example that the data doesn’t “make a distinction in whether you are buying 10 apples for $2 or two apples for $10.”

“What we are seeing is consumers are dramatically shifting the goods and services in their basket, something we do as consumers when we are aware of somewhat fragile footing,” she explained.

When it comes to fuel prices, she said, she said that the estimate is that for every $1 rise in gas prices there is $1.2 billion not spent on other goods and services.

The Projection

Overall, Piezga is projecting economic growth of 2%-2.5% this year, with the caveat being that the ongoing war with Iran could significantly reduce that number.