SAUSALITO, Calif.–Credit unions may want to tweak their card strategies for 2026 following the release of a deep dive into new data from the CFPB that reveals an evolving landscape in the consumer credit card industry, including how cardholder spending has increased and where, what’s happening with account balances, the role of interest rates, and consumer adoption of AI and other emerging technologies.

The study further shows credit union credit card balances grew to $85.7 billion, representing 7% of the market.

As the CU Daily reported here, the CFPB published its seventh biennial Credit CARD Act report. As required by the CARD Act, the report discusses the state of the credit card market through 2024, with a particular focus on credit card usage and availability, the cost of credit accessed through credit cards, delinquency and collection, market dynamics, issuer practices such as rewards, installment plans, and deferred interest, and innovations in the credit card market.

According to an analysis of the data performed by JD Supra, probing deeper into the new CFPB report uncovers a number of insights that may help credit unions in their decision-making. Those insights include:

Credit Card Usage and Market Dynamics

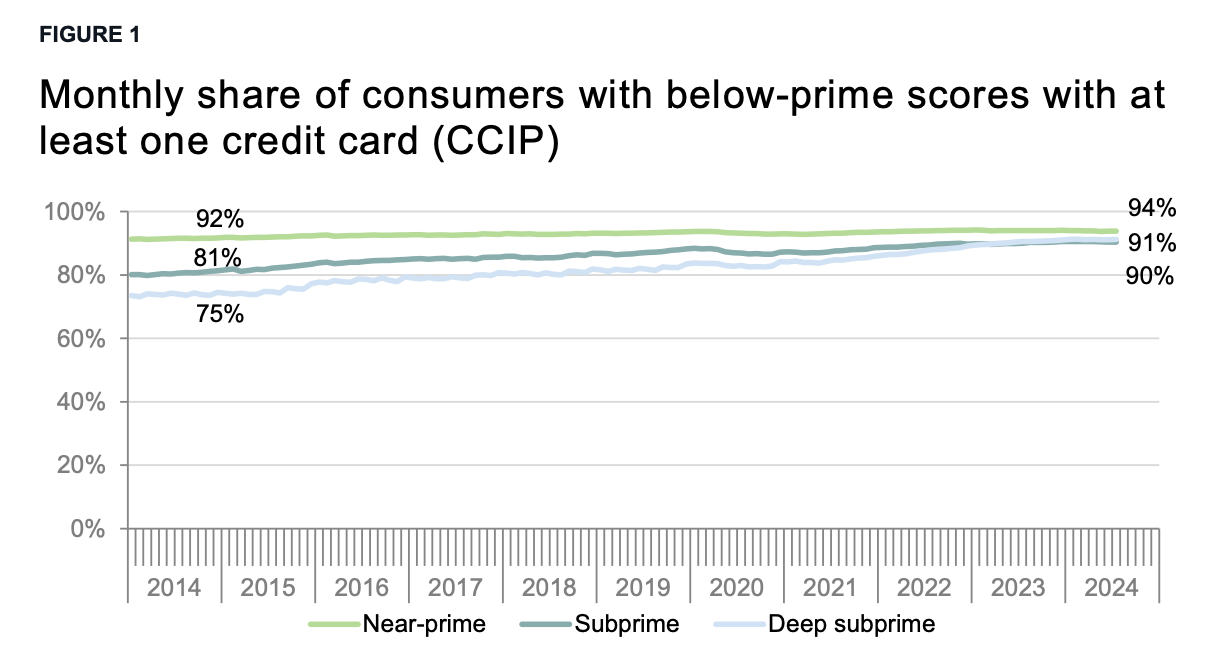

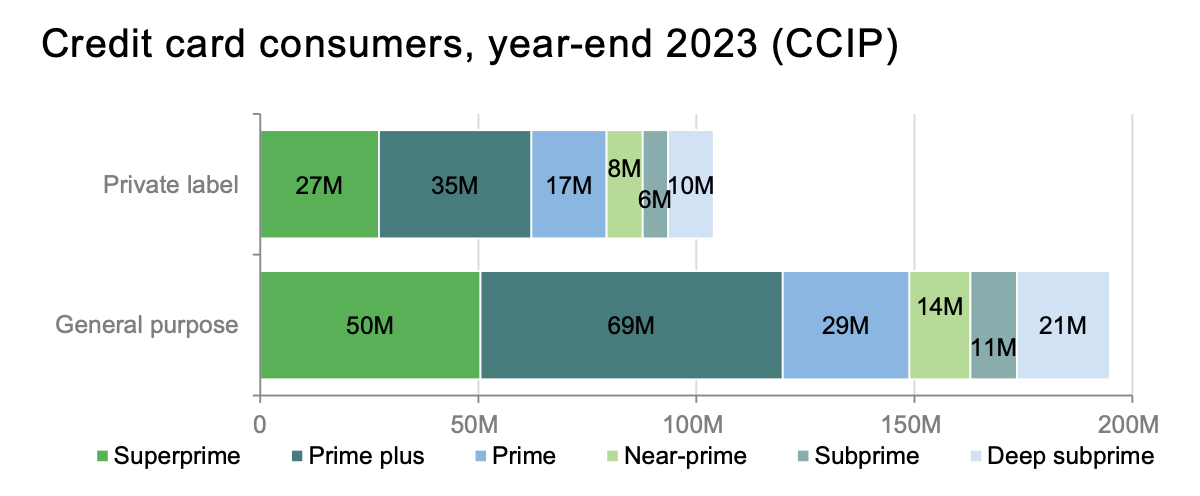

- 78% of U.S. adults have at least one credit card. Most of these cardholders have prime or higher credit scores (i.e., 660 FICO and over). There are almost 800 million credit card accounts in the U.S., over three-fourths of which are general-purpose cards. The number of general-purpose credit accounts has consistently increased while the number of private-label accounts has declined by over 33% since 2018.

- Credit card purchase volume has increased to $3.6 trillion (for the largest 14 issuers) in 2024 — a 13% increase from 2022, primarily driven by cardholders with prime plus credit scores or higher (i.e., 720 FICO and over). JDSupra noted these amounts are nominal and are not adjusted for inflation. By some measures, prices increased 10% over the same period.

- Credit card balances surpassed $1.2 trillion in 2024, with average total balances per cardholder of $5,312, exceeding pre-pandemic levels (though not in inflation-adjusted dollars). Cardholders with prime and near-prime credit scores (i.e., 620-719 FICO), who had average combined balances of $8,675 and $7,493, respectively, drove average balance growth.

- The average APR for general-purpose cards reached 25.2%, the highest since 2015, mostly due to changes in the underlying prime rate.

- One of the two largest merchant categories in 2024 are “professional and financial services” at $646 billion total purchase volume. These services include wire transfers, utilities, cash disbursement (e.g., cash advances), and childcare as well as merchant aggregators which assist local businesses like coffee shops, hair salons, etc.

Consumer Payment Behavior:

JDSupra noted the CFPB report reveals cardholders in the aggregate continue to pay a higher share of their balance than they did prior to the pandemic.

“However, cardholder payment behavior is highly correlated with credit score — “super prime” cardholders (i.e., 800 FICO or greater) pay approximately their entire balance every month, while cardholders with prime or lower credit scores pay 15% or less of their monthly balance,” the analysis states.

Among the other findings:

- The share of cardholders making only minimum payments has increased, with 15% of general-purpose cardholders and 20% of private-label cardholders doing so in 2024, up from 13% and 17%, respectively, in 2022. Although the average minimum payment increased across all credit score tiers, this was driven by higher balances as issuer formulas for setting minimum payments have remained consistent.

- Rates of “persistent debt,” which the report defines as debt where at least 50% of the actual payment amount in a year is for interest and fees (consistent with the 2023 CARD Act report), have increased to 13% from 9.9% in 2022.

- Interest charges rose to $160 billion in 2024 from $105 billion in 2022, driven by more cardholders, higher APRs, and increased cardholder balances. About half of cardholders are “revolvers,” consistent with pre-pandemic levels, though cardholders in prime or below credit tiers are almost four times more likely to revolve (ranging from 72-88%) than super prime cardholders (20%).

- The report indicates that between 2022 and 2024, the percentage of consumers who paid an annual fee declined. “However, the average annual fee rose, driven by high-rewards cards marketed to super prime cardholders,” the analysis states. “Total late fees increased through 2023, while declining slightly at the end of 2024. Not surprisingly, late fee incidence is correlated with credit score with deep subprime consumers (i.e., 579 FICO or less) incurring 4.7 late fees per year on average, more than three times the incidence for prime cardholders and almost double the incidence for subprime cardholders.”

Rewards and Promotional Offers

- Rewards cards were the most common type of card, accounting for 92% of general-purpose card purchase volume. Among rewards cards, cash back became the most common, accounting for 36% of the total number of general-purpose card accounts. The report notes that large banks have invested significant resources in developing differentiated rewards cards targeted to high score cardholders who tend to spend more.

- Credit card rewards that are earned or redeemed in the form of cryptocurrency stored in an affiliated investment account continue to grow. Cards with 0% introductory-APR promotions accounted for one-third of purchase volume, $899 billion in 2024. Accounts with introductory rates exhibit showed higher longer-term balances than cards without, and by 36 months after account opening, the average balance on cards that had introductory promotions are still 69%% higher.

Delinquency and Debt Collection

Credit card delinquencies and charge-offs peaked in early 2024 but returned to pre-pandemic levels of 3% and 3.8%, respectively, by year-end. Dispute and chargeback volumes have remained fairly constant.

“Debt collection practices have shown a decline in pre-charge-off collection performance, marked by lower cure and liquidation rates,” the analysis observes. “All surveyed issuers reported policies that capped daily calls per account. These caps ranged from one to four calls per account, down from one to 11 calls per day as reported in the 2023 report. Actual average attempts remained within the historic range of one to 2.8 per day.

The analysis further notes that several issuers sent change in terms notices implementing paper statement fees, ranging from $2 to $5.99. Generally, cardholders with higher credit scores are more likely to receive paperless statements than other cardholders. The exception is for accounts with deferred interest promotions, in which the pattern is reversed.

Market Segmentation:

As of 2024, approximately 3,700 financial institutions reported holding credit card balances, down from 4,700 10 years ago, according to the CFPB data. Larger issuers hold approximately 84% of all balances and 95% of super prime balances, while smaller issuers (those outside of the top 30) cater to below-prime consumers and account for only 5% of balances. This distribution has remained largely consistent over the past 10 years, JDSupra states.

The report also shows:

- Many of the smaller issuers provide credit card-as-a-service to other financial institutions (including fintechs).

- Credit union credit card balances grew to $85.7 billion, representing 7% of the market.

Innovation and Technology

According to the JDSupra review of the CFPB data, during the last two years the number of installment-plan originations has doubled, although the average amount of credit extended in installment plans has fallen from just under $1,000 to approximately $600. During each year, the largest number of originations occurred during the fourth quarter.

“AI and alternative data are improving underwriting and expanding credit access, particularly for consumers with limited credit history,” the report states.

It further report suggests that AI is also contributing to increases in both the incidence and seriousness of fraud, as well as issuers’ efforts to combat it.

Increasing Reliance on AI

“Consumers are increasingly relying on AI-powered tools for financial advice, specifically to help consumers manage their spending, optimize spending over numerous cards, or manage debt,” JDSupra stated. “The report notes the potential benefits of this innovation for consumers, while noting that AI-powered advice introduces novel privacy challenges and other risks.”

It further report suggests that AI is also contributing to increases in both the incidence and seriousness of fraud, as well as issuers’ efforts to combat it.